London Wrap – FTSE recovers to 7150 as pound softens.

A mixed start for European equities after a slightly soft start amid worries about China, which has lowered its target for growth in 2019 at 6-6.5%, down from a pinpoint target of 6.5% before. Clearly China’s economy is slowing – expect further policy measures to stimulate activity, although the lowering of the growth target is an admission of economic reality. After a stuttering start though European markets are now mainly going green.

Meanwhile, China’s services sector activity declined again in February. The Caixin-Markit PMI slipped to 51.1 for last month, with new export orders at the weakest in 5 months. The latest manufacturing report was a little more upbeat, although it remains below the magic 50 line between contraction and expansion.

We also had a weaker handover from the US yesterday – SPX has failed on the 2800 tussle for now and is coming off at last following the ramp up in the first couple of months of the year. Weaker construction figures were maybe a factor, but I’d put this down to a technical breakdown at key resistance levels as the bulls tried to break the Oct and Nov twin peaks a little above the 2800 round number. It’s also as we look at the global picture a case of markets pausing for breath, taking some profit and – as I said in yesterday’s note – a buy the rumour, sell the news type trade. Look for pull backs ahead of the ink drying on any deal between the US and China.

The FTSE 100 has held the line at 7100, with a softer pound doing the main work for the blue chips as it pushed on up to 7150. The weakening sterling will offer support and if it does soften further towards 1.30 again we may well see the FTSE break 7200.

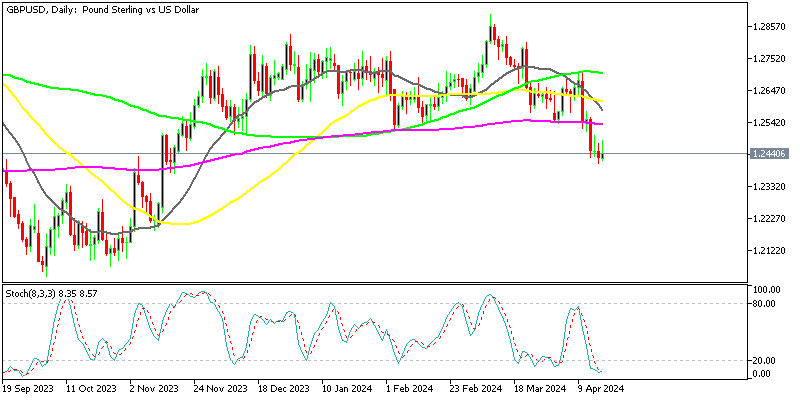

Looking at FX, GBPUSD has slumped to a week low ahead of the services PMI figures due at 09:30, whilst the US ISM services PMI is also due later. Also watch for Mark Carney’s testimony in parliament later today as a potential risk event for sterling. Brexit uncertainty continues, we could see a softening in pound crosses ahead of the votes next week. Broadly the dollar remains well bid with EURUSD also softer as we run into the ECB meeting on Thursday. The market seems reasonably well positioned for the bank to strike a dovish note. The dollar remains the least ugly sister right now.