Is This the Beginning of the USD Retreat After Services Fall in Contraction?

US services PMI fell deeper in contraction in July, meaning no 75 bps hike from the FED, which is helping improve the risk sentiment

The US economy fell into recession during Q1 and Q2 of this year, although the manufacturing and service sectors were holding well until the services PMI indicator fell in contraction in June. Last month this indicator was expected to climb to breakeven, but it showed a further decline, which dampens the odds of another strong rate hike worth 75 bps from the FED.

This is a good thing for the risk sentiment, even though it’s bad data, so stock markets and commodity dollars have jumped higher, while the USD has turned lower. So, it seems like this might be the beginning of a bearish retreat period for the USD after the uptrend of the last two weeks. But, the situation is still unclear, so let’s see where everything ends up after the dust settles.

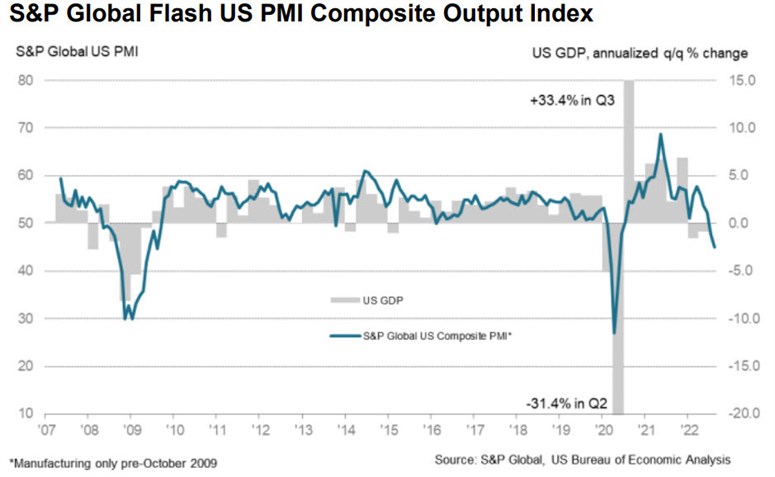

US Prelim Services PMI Survey

- Services July flash PMI 44.1 points vs 49.2 expected

- June services were 47.0 points

- July manufacturing 51.3 points vs 52.0 expected

- Prior manufacturing was 52.3 points

- Composite 45.0 points vs 47.7 prior

The fall below 50 in services last month was the first decline below that level since June 2020. Excluding the pandemic, this is the worst since 2009.

Details:

- Services new orders contracted at the steepest pace for over two years

- Services level of outstanding business decreased at the quickest rate since May 2020

- Services input costs continued to rise markedly

- Services hopes of an uptick in new business drove the degree of optimism regarding the outlook for output over the coming year to the highest for three months

- In manufacturing, going supply chain issues, paired with weak client demand, led to the drop in output

- Manufacturing new export orders fell solidly as inflationary pressures in key export markets weighed on demand

- Manufacturers registered the slowest rise in cost burdens since January 2021

- Signs of improvements in supply chain disruption emerged, as manufacturing delivery times lengthened to the least marked extent since October 2020

The fall in manufacturing export orders could be a sign the strong US dollar is beginning to bite. Commenting on the flash PMI data, Siân Jones, Senior Economist at S&P Global Market Intelligence said:

“August flash PMI data signalled further disconcerting signs for the health of the US private sector. Demand conditions were dampened again, sparked by the impact of interest rate hikes and strong inflationary pressures on customer spending, which weighed on activity. Gathering clouds spread across the private sector as services new orders returned to contractionary territory, mirroring the subdued demand conditions seen at their manufacturing counterparts. Excluding the period between March and May 2020, the fall in total output was the steepest seen since the series began nearly 13 years ago.

“Lower new order inflows and continued efforts to rein in spending led to the slowest uptick in employment for almost a year. Reports of challenges finding suitable candidates started to be countered by those companies noting that voluntary leavers would not be replaced with any immediacy due to uncertainty regarding demand over the coming months.

“One area of reprieve for firms came in the form of a further softening in inflationary pressures. Input prices and output charges rose at the slowest rates for a year-and-a-half amid reports that some key component costs had fallen. Although pointing to an ongoing movement away from price peaks, increases in costs and charges remained historically robust. At the same time, delivery times lengthened at the slowest pace since October 2020, albeit still sharply, allowing more firms to work through backlogs.”

At least there’s some good commentary on inflation. But overall, the US dollar is getting smacked on this report which is casting new doubts on the service sector, which is supposedly the strong pillar of the US economy. There’s some optimism in orders so it doesn’t necessarily point to an autumn slowdown but it’s certainly problematic. EUR/USD is up to parity again from 99.40 on this report with similar-sized USD moves elsewhere.

EUR/USD Live Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts