US Session Forex Brief, May 3 – Sentiment Remains Negative Despite the Jump in Eurozone Inflation

The inflation report form the Eurozone didn't move markets today but the US employment report might get them started

The sentiment in financial markets has been slightly positive in recent weeks as some sectors of the global economy return to growth again, although the miss in Chinese manufacturing and services as well as the confirmation of the contraction for manufacturing activity in Europe and in Germany hurt the sentiment. FED’s Powell also gave the sentiment a kick on Wednesday evening after he dismissed the soft inflation figures recently as transitional. As a result, risk currencies have turned bearish in the last few days, with commodity Dollars down, and most of major stock indices also down on the week.

This morning we had the inflation report form the Eurozone which was quite surprising as headline CPI (consumer price index) CPI jumped three points higher while core CPI jumped four points higher. That should be a relief for the European Central Bank (ECB) but there are some seasonal factors which might have helped inflation climb higher in April, so the Euro didn’t really mind the numbers. We have to wait and see how May’s inflation figures come out in order to see the bigger picture.

We have heard US officials say that the deal with China is pretty close, but the Chinese played those comments down as mere pressure from the US to get the deal done as soon as possible. That should weigh some more on risk assets. We also had the services report from the UK today and this sector came back into expansion in April after having fallen into contraction in March.

European Session

- Swiss CPI – Inflation turned negative at the end of last year in Switzerland and it declined for three months from November to January this year. But it returned back to positive territory in February, growing by 0.4% that month and by 0.5% in March. Although a slowdown to 0.2% was expected in April and it indeed slowed to 0.2% as expected.

- UK Services PMI – The activity in the service sector has been slowing down in Britain during the end of last year and for several months it was close to stagnation. Although, we saw that this sector fell into contraction in March as the PMI indicator declined to 48.9 points. Although, it was expected to turn positive again in April and the actual number came as expected at 50.4 points. That’s still pretty close to stagnation though. New orders continued to shrink, recording a print of 49.0, and is now on its longest run of contraction readings since 2009. Surveying firm Markit notes that the April PMIs recorded overall are consistent with the UK economy stagnating. Not much action in the GBP.

- Eurozone CPI Inflation – Inflation has been weakening for several months in the Eurozone and in March inflation lost two points falling from 1.6% to 1.4%, while core CPI fell from 1.0% to 0.8%. Although expectations for April were for a return to the previous levels, the actual numbers today beat those estimates. Headline CPI jumps to 1.7% from 1.4% previously, while core inflation moves to 1.2% again from 0.8% in March. Core inflation jumps to a six-month high, rebounding strongly in April. But as I mentioned above, there is some upside bias due to Easter holiday period seasonality in April, so we better wait for May’s number. The Euro continued to slide lower.

- German Bundesbank’s Weidmann’s Speaking – Bundesbank chief, Jens Weidmann, was speaking earlier this morning saying that German growth dip proving to be more persistent than initially thought. Germany likely posted solid Q1 growth but this is helped by one-off factors like mild weather. Low borrowing costs and rising wages suggest that growth will pick up later this year.

- China Calls US Bluff – US officials have been commenting that they are close to striking a deal with China, but the Chinese consider that as a bluff to get China to sign the deal soon. Chinese officials came up with a statement today: “It’s the same tactic as the US threatening to raise tariffs, it is merely smoke and mirrors to exert extreme pressure [on China],” the post said. “You don’t have to take it seriously.”It warned that there is still a possibility that the two sides will end up in “an unhappy departure” if one side wants the other to make compromises and neglects “fairness in negotiation”.

US Session

- UK PM May ‘Profoundly Disagree’ with Calls for a Second Referendum – Theresa May made this comment a while ago and she added that the best way to deliver Brexit is to leave with a deal. The Parliament has made clear that it will prevent a no-deal Brexit. There was a simple message from local elections: “Get on and deliver Brexit”, but this is a difficult time for the Tory Party.

- US Unemployment Rate – The unemployment rate declined to 3.8% in February from 4.0%. It remained unchanged in March and it is expected to remain where it is for April as well when the employment report from the US comes out shortly.

- US Average Hourly Earnings – Earnings have been sort of volatile so far this year, jumping by 0.4% for two months, but then falling to 0.1% growth again. But, that’s better than the really soft figure we saw last year. Today’s report which is for March is expected to show another jump, this time to 0.3%, but let’s see if earnings really jump higher.

- US Final Services PMI – The services sector has held up to the normal range at around 55 points for many months, but the first reading for April showed a considerable slowdown and the PMI indicator came at 52.9 points. The final reading for last month is now expected to remain unchanged as the prelim reading, so let’s see how it comes out.

- US ISM Non-Manufacturing PMI – The non-manufacturing PMI has held up pretty well in the US at around 56-57 points and this is the best performing sector now after the slowdown in manufacturing we saw yesterday. Last month’s report showed a decline to 56.1 points, but today’s report which is for April is expected to show another reversal higher to 57.2 points.

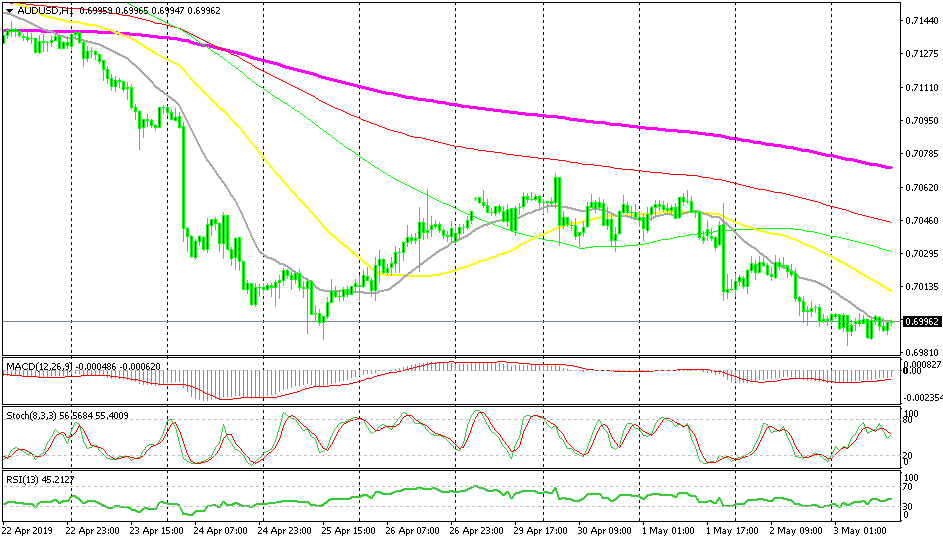

Bullish AUD/USD

- The main trend is bearish

- The pullback higher is over

- The 20 SMA is now pushing the price lower

The trend is strong if the 20 SMA is pushing the price down

Yesterday I posted the NZD/USD chart and the bearish trend there. Today I am going with AUD/USD since the picture is similar and the pressure is on the downside here as well. This pair has been bearish since the middle of April but it put up a reversal at the end of last week. That retrace is over now and the bearish trend has resumed. The sellers are threatening last week’s lows and the 20 SMA is pushing the price down, which is telling the strength of the trend.

In Conclusion

The inflation report from Europe this morning was impressive as both headline and core CPI jumped higher, but the Euro totally ignored those numbers and EUR/USD continues to slide lower. But, the US earnings and employment report is coming out soon and that might reverse things in the markets, so let’s get this update posted and concentrate on that report now.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts