Forex News and Market Analysis

Monday, June 15, 2026

The JSE FTSE All Share Index has succeeded in continuing its positive performance and has shown gain ...

33 seconds

Gold Price Forecast: Bullion hits $4,330 as markets brace for Kevin Warsh's historic first FOMC poli ...

8 minutes

Paramount Skydance Gains Regulatory Momentum as $111 Billion Warner Bros Deal Nears Finish Line

4 min read

...

2 hours

Zcash crashed 50% after revealing ...

3 hours

Dow futures are pointing h ...

3 hours

Silver rose briefly, breaking above $70 an ounce amid a historic rally driven by speculative trading ...

4 hours

XRP is currently navigating a highly visible consolidation ...

4 hours

CoreWeave shares rose 5.02% to $100.55, helped by renewed optimis ...

4 hours

...

5 hours

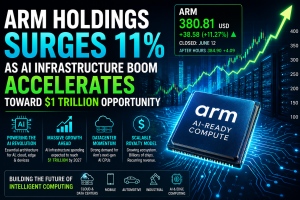

Arm Holdings Surges 11% as AI Infrastructure Boom Accelerates Toward $1 Trillion Opportunity

4 min read

...

7 hours

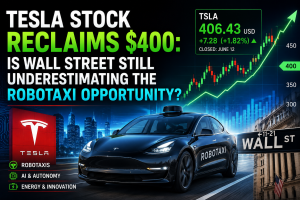

Tesla Stock Reclaims $400: Is Wall Street Still Underestimating the Robotaxi Opportunity?

3 min read

...

9 hours

USD/ZAR has turned lower toward the R16 level as improving geopolitical sentiment and a softer US do ...

11 hours

Ahead of the Federal Reserve's policy meeting, optimism about a possible Middle East peace framework ...

12 hours

Crude oil prices fell precipitously as investors turned their focus to the Federal Reserve's impendi ...

12 hours

...

13 hours

After temporarily dropping below $60,000 in early June, BTC has risen above $65,000 due to strong te ...

13 hours

Silver sank after briefly breaking below $68 an ounce amid a historic rally driven by speculative tr ...

1 day

BlackRock was covertly connecting Ripple's XRP infrastructure after the Wormhole development team an ...

1 day

When it comes to the markets, staying abreast of important economic events and breaking news

items is a full time job. Whether one is an active day trader or a long-term investor, the need to be current is one that must be satisfied every

single day. The FX Leaders news feed is a great way to stay on top of the evolving global

marketplace.

Everything You Need In An FX News Service

All Things Forex News, 24 Hours A Day, 5 Days A Week

Sidebar rates