USD Ends Lower After After Softer US Inflation CPI

The US Inflation CPI showed signs of slowing down in April, after a strong Q1, which is weighing on the USD as FED rate cut odds go up.

The US Inflation CPI showed signs of slowing down in April, after a strong Q1, which is weighing on the USD. The odds of a FOMC interest rate cut have moved higher, which is benefiting risk assets such as commodity dollars, and weighing down on safe havens, with the US Treasury yields moving lower.

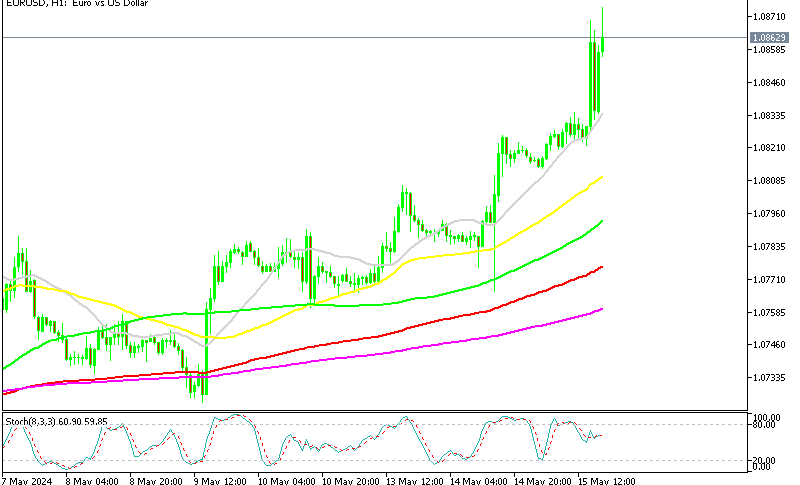

EUR/USD Chart H1 – The 20 SMA Has Turned into Support

The CPI report leaned on the soft side, and the market’s reaction to it indicates an increasing expectation for FED interest rate cuts this year, with the market now pricing in 50 basis points of cuts compared to 47 basis points prior to the release of the CPI figures. While the report may not prompt immediate confidence for the FED to lower rates, it does lessen the likelihood of future rate hikes and addresses concerns about sticky inflation.

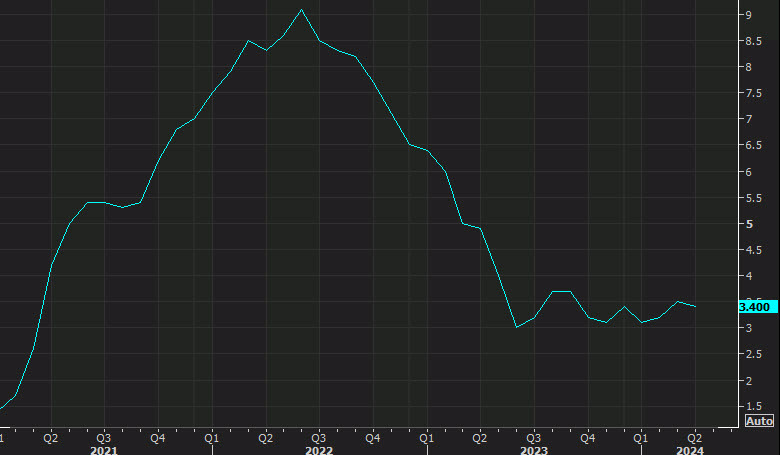

US April 2024 Consumer Price Index (CPI) Report

Headline US CPI Measures:

- Year-over-year (y/y) CPI stood at 3.4%, in line with expectations and slightly lower than the previous month’s 3.5%.

- Month-over-month (m/m) CPI increased by 0.3%, slightly below the expected 0.4% and slightly lower than the previous month’s 0.4%.

Core CPI Measures:

- Core CPI, which excludes volatile food and energy prices, had a month-over-month increase of 0.3%, matching expectations but lower than the previous month’s 0.4%.

- Year-over-year core CPI was at 3.6%, in line with expectations but down from the previous month’s 3.8%.

Other Key Inflation Highlights:

- Shelter prices increased by 0.4% month-over-month, consistent with the prior month.

- Services less rent of shelter increased by 0.2% month-over-month, lower than the previous month’s 0.65%.

- Real weekly earnings declined by 0.4%, contrasting with the previous month’s increase of 0.3%.

- Food prices remained unchanged month-over-month, while energy prices increased by 1.1%.

- Rents and owner’s equivalent rent both increased by 0.4% month-over-month, consistent with the prior month.

The data on rents and owners’ equivalent rent, which remained relatively high, may provide some reassurance to the FED, as it suggests that any disinflation may be more of a timing issue rather than a long-term trend. Additionally, the energy price increases seen in April were reversed in May, contributing to the overall narrative of potential disinflationary pressures.

Overall, the report highlights the importance of factors such as petrol and shelter prices, which accounted for a significant portion of the CPI increase. However, it suggests that these increases may not be sustainable in the long term, providing some relief for policymakers concerned about inflationary pressures.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts