Prices Forecast: Technical Analysis

For the EUR/USD, the daily closing price is predicted to be around 1.1705, with a range between 1.1685 and 1.1743. The weekly closing price is expected to be approximately 1.1720, with a range from 1.1685 to 1.1750. The RSI is currently at 69.045, indicating a bullish trend as it approaches the overbought territory. The ATR at 0.0091 suggests moderate volatility, while the ADX at 22.5036 shows a strengthening trend. The MACD line is above the signal line, reinforcing the bullish sentiment. These indicators, combined with the recent economic data showing stable inflation and retail sales in the Eurozone, support a positive outlook for the EUR/USD in the short term.

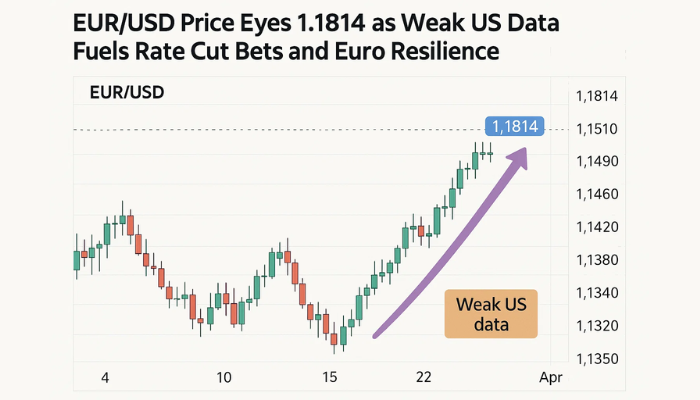

Fundamental Overview and Analysis

Recently, the EUR/USD has shown a steady upward trend, driven by positive economic indicators from the Eurozone, such as stable inflation and retail sales figures. The asset’s value is influenced by the balance of economic data between the Eurozone and the US, with the latter showing moderate personal spending and income growth. Investor sentiment remains cautiously optimistic, with the Euro benefiting from a stable economic outlook. Opportunities for growth include potential improvements in Eurozone economic conditions and a weaker US dollar. However, risks such as geopolitical tensions and potential shifts in monetary policy could pose challenges. Currently, the EUR/USD appears fairly priced, reflecting the balance of economic conditions and market sentiment.

Outlook for EUR/USD

The future outlook for EUR/USD remains positive, with expectations of continued upward momentum. Historical price movements show a consistent upward trend, supported by moderate volatility and positive economic indicators. Key factors influencing the price include Eurozone economic data, US monetary policy, and global market conditions. In the short term (1 to 6 months), the EUR/USD is expected to maintain its upward trajectory, potentially reaching 1.1750. Long-term forecasts (1 to 5 years) suggest further growth, contingent on stable economic conditions and favorable market dynamics. External factors such as geopolitical events or significant policy changes could impact this outlook, but current trends support a bullish perspective.

Technical Analysis

Current Price Overview: The current price of EUR/USD is 1.1705, slightly above the previous close of 1.1684. Over the last 24 hours, the price has shown an upward trend with moderate volatility, characterized by bullish candles.

Support and Resistance Levels: Key support levels are at 1.1685, 1.1669, and 1.1663, while resistance levels are at 1.1743, 1.1750, and 1.1755. The pivot point is at 1.17, with the asset trading slightly above it, indicating bullish sentiment.

Technical Indicators Analysis: The RSI at 69.045 suggests a bullish trend. The ATR of 0.0091 indicates moderate volatility. The ADX at 22.5036 shows a strengthening trend. The 50-day SMA and 200-day EMA do not show a crossover, maintaining a bullish outlook.

Market Sentiment & Outlook: Sentiment is currently bullish, supported by price action above the pivot, a rising RSI, and a strengthening ADX. The absence of a moving average crossover further supports the bullish sentiment, with moderate volatility as indicated by the ATR.

Forecasting Returns: $1,000 Across Market Conditions

Investing $1,000 in EUR/USD under different market scenarios can yield varying returns. In a Bullish Breakout scenario, a 5% price increase could raise the investment to approximately $1,050. In a Sideways Range scenario, with a 0% change, the investment remains at $1,000. In a Bearish Dip scenario, a 3% decrease could reduce the investment to about $970. These scenarios highlight the importance of market conditions on investment outcomes. Investors should consider current bullish sentiment and moderate volatility when making decisions. Practical steps include monitoring economic indicators and technical signals to adjust positions accordingly.

| Scenario | Price Change | Value After 1 Month |

|---|---|---|

| Bullish Breakout | +5% to ~$1,229 | ~$1,050 |

| Sideways Range | 0% to ~$1,170 | ~$1,000 |

| Bearish Dip | -3% to ~$1,135 | ~$970 |

FAQs

What are the predicted price forecasts for the asset?

The daily closing price for EUR/USD is predicted to be around 1.1705, with a range between 1.1685 and 1.1743. The weekly closing price is expected to be approximately 1.1720, with a range from 1.1685 to 1.1750.

What are the key support and resistance levels for the asset?

Key support levels for EUR/USD are at 1.1685, 1.1669, and 1.1663, while resistance levels are at 1.1743, 1.1750, and 1.1755. The pivot point is at 1.17, with the asset trading slightly above it, indicating bullish sentiment.

Disclaimer

In conclusion, while the analysis provides a structured outlook on the asset’s potential price movements, it is essential to remember that financial markets are inherently unpredictable. Conducting thorough research and staying informed about market trends and economic indicators is crucial for making informed investment decisions.