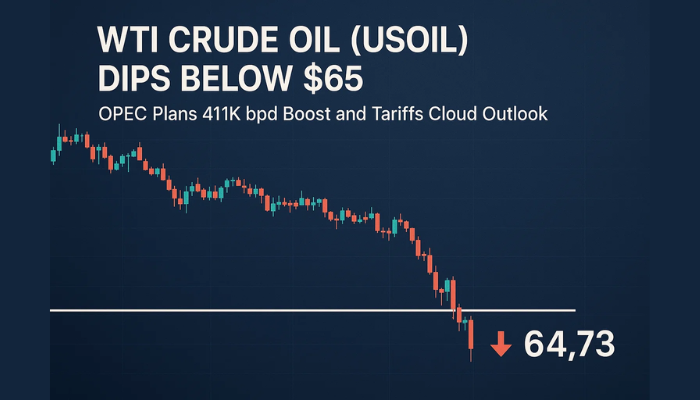

WTI Crude Oil Remains Under Pressure at Around $40 – Oversupply Fears in Play!

WTI crude oil prices failed to stop the previous day’s losing streak, remaining depressed at around the $40.31 level. Most of the selling...

During Wednesday’s Asian trading session, the WTI crude oil prices failed to stop the previous day’s losing streak, remaining depressed at around the $40.31 level. Most of the selling bias came due to the risk-aversion market sentiment. The risk appetite was backed by the relentless spread of the coronavirus, which resulted in continuous fading of optimism regarding the economic reopening, thereby contributing to the oil losses.

On the other hand, the reason behind the oil price declines could also be associated with the report that showed a build in US crude stockpiles, which were fueled by fears of the continuous increase in the number of COVID-19 cases. A bearish bias was triggered, as traders fear that this will stop the economic recovery and the demand for energy.

Moreover, the geopolitical tension between the US and the rest of the global economies, like the European Union (EU), the UK and China also exerted some downside pressure on the risk tone, providing support for crude oil, which is trading at $40.37 and consolidating in the range between 40.31 and 40.73.

On the data front, the American Petroleum Institute (API) announced a two million-barrel build in crude oil supplies for the week ended July 3, which was much higher than the draw of 3.7m barrels in forecasts. The fears of oversupply rose with increasing numbers of COVID-19 cases, dampening the global oil demand. As per the latest report, US coronavirus cases increased to over 3 million in total so far, the largest outbreak in the world as per the report. The cases in Texas rose by more than 10,000 in just one day. It is worth mentioning that this was a new record increase for the state, which recorded 60 deaths in one day.

Elsewhere, the coronavirus situation in Los Angeles County also flashed red signals. The death toll has risen above 2,700, with the hospitalized cases hitting a new record high of 9,286 (9th day in a row of record hospitalizations), which rose by 588 compared to the previous day. As a result, the broad-based US dollar reported gains on the day, as investors preferred to invest in safe-haven assets, mainly due to concerns about the mounting number of coronavirus cases. The US dollar gains also kept the oil prices under pressure, due to an inverse relationship between crude oil and the US dollar. At the same time, the US Dollar Index, which tracks the greenback against a basket of other currencies, gained 0.06%, rising to 96.895 by 12:09 AM ET (5:09 AM GMT).

Apart from the virus woes, the US-China dispute was on the cards, as US Secretary of State Mike Pompeo recently imposed visa restrictions for some Chinese officials over the Tibet issue. Moreover, the dragon nation kept its strong stand against Americans and the UK, concerning the ban on Huawei, and fought against the Hong Kong security laws.

The risk-off market sentiment was further bolstered by the announcement by Australia, that lockdown restrictions would be re-imposed for Melbourne. In the meantime, Australian Prime Minister (PM) Scott Morrison hinted at further restrictions in terms of travel. While talking about his concerns over the Hong Kong issue, Morrison said that the situation in Hong Kong was very concerning and that the Australian government was very actively considering proposals to welcome residents of the former British territory, and this also favored the risk-off mood. Looking forward, traders will be focusing on the trade/virus updates, due to the lack of any major economic data to be published today. Good luck!

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account