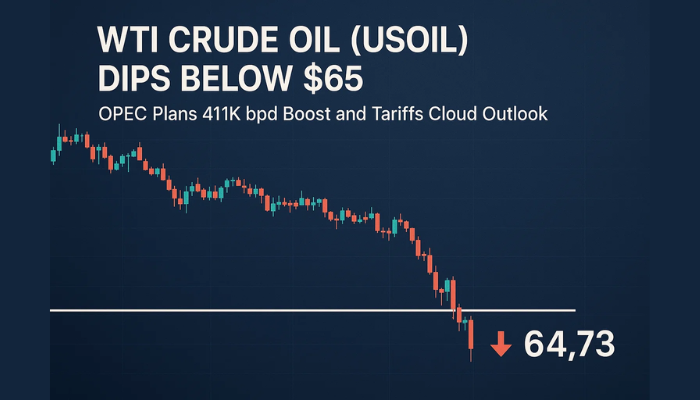

Crude Oil Prices Slips to Sessions Low – OPEC+ Meeting In Focus!

WTI crude oil prices failed to stop their early day losing streak, dropping further toward the $39.09 level, while representing 2% declines

During Tuesday’s Asian trading session, the WTI crude oil prices failed to stop their early day losing streak, dropping further toward the $39.09 level, while representing 2% declines on the day, mainly due to OPEC’s expectations that, in an upcoming meeting, + might ease output cuts as of August. However, oil buyers failed to cheer fresh, upbeat China’s Crude Oil Import reports, due to a mixed market mood and coronavirus concerns.

Elsewhere, the oil price declines could also be attributed to the virus woes, which heightened the fears of falling demand. This sentiment was further supported by geopolitical tensions between the US and the rest of the global economies, like the European Union (EU), the UK and China, which also exerted some downside pressure on crude oil prices. Currently, WTI crude oil is trading at $39.27 and consolidating in the range between 39.09 – 39.69.

On the data front, China’s crude oil imports surged by 33% in June for the year, accounting for the second straight record month, as per the General Administration of Customs data on the day. Meanwhile, the world’s top crude oil importer, China, imported 53.18 million tons of oil, which is equivalent to 12.9 million barrels per day (BPD). That easily beat the previous record of 11.3 million BPD in May, and was up 34% from the 9.63 million BPD in June 2019. Data showed that in the first half of 2020, China imported 268.75 million tons of crude oil, which is equivalent to 10.78 million BPD – a whopping 9.9% higher, compared to the same period last year.

As we have already mentioned, the OPEC+ group of producers is likely to begin retreating from the large production cuts that have been in place for a couple of months, which also added bearish pressure to oil prices and will keep traders cautious until the announcement of the final decision. However, the OPEC+ decision could be associated with the reports of the latest IEA demand forecast for 2020. The institute’s monthly report for July stated: “The IEA estimates that global oil demand this year will average 92.1 million barrels per day, which is down by 7.9 million barrels per day compared to 2019, which is a slightly smaller decline than forecast in the last report.”

However, the long-lasting pandemic continued to fuel the fears of reducing oil demand from some of the biggest oil consumers. As per the virus report, the US has recorded 59,747 new infections in the last 24 hours, as per the Johns Hopkins University. At the same time, the total number of cases in the US rose to the alarming figure of 3,479,483. Global figures now exceed 13 million, with more than 565,000 people having died of the virus in the last 7 months, according to reports by global institutes.

On the other hand, Brazil and India are also following in the footsteps of the US, and are now the nations with the 2nd highest number of new cases after the US. The latest figures from Florida suggested over 15,000 new cases on Sunday, after further pressure to reopen schools and anti-mask protests.

Considering the worsening of the virus situation, California’s governor ordered that bars and restaurants, movie theatres, zoos and museums be closed, in order to put a stop to indoor operations. At the same time, the two largest school districts in the most populous state, Los Angeles and San Diego, also decided to revert to online teaching only, when classes resume in August.

Apart from the virus woes, the US-China dispute remained on the cards, due to the recent differences between the US and China over trade issues, and also regarding Hong Kong’s national security laws. As a result, the US Secretary of State, Michael Pompeo, issued a statement on Monday, rejecting Chinese claims in the South China Sea. Moreover, the tussle between the US and China over the Huawei ban flashed red signals, which also favored the bearish trend in crude oil.

As a result, the broad-based US dollar extended its early-day bullish moves, remaining well bid, as investors turned to the safe-haven in the wake of an intensified tussle between the US and China. However, the gains in the US dollar kept the crude oil price lower, as the price of crude oil is inversely related to the US dollar price. The US Dollar Index, which tracks the greenback against a basket of other currencies, gained 0.03%, rising to 96.537 by 9:36 AM ET (2:36 AM GMT).

However, the hopes of further stimulus from the US, backed by the comments by the President and CEO of the Federal Reserve Bank of Dallas, Robert Kaplan, and combined with the positive results achieved in testing of the much-championed drug, Remdesivir, kept a lid on any additional losses in the oil prices. On the other hand, the S&P 500 Futures diverted from the downbeat Wall Street performance to print 0.21% gains, to around 3,155. However, the US 10-year Treasury Yields remain depressed at around 0.62%.

The US Consumer Price Index (CPI) data for the previous month will be key to watch. The market traders will keep their eyes on the Organization of the Petroleum Exporting Countries (OPEC) meeting, which is due on Wednesday, to discuss whether to keep the production cuts of 9.6 million barrels per day (BPD) in place, or to roll them back, possibly by 2 million BPD. Traders will keep their focus also on USD price dynamics and coronavirus headlines, which could play a key role in influencing the intraday momentum. Good luck!

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account