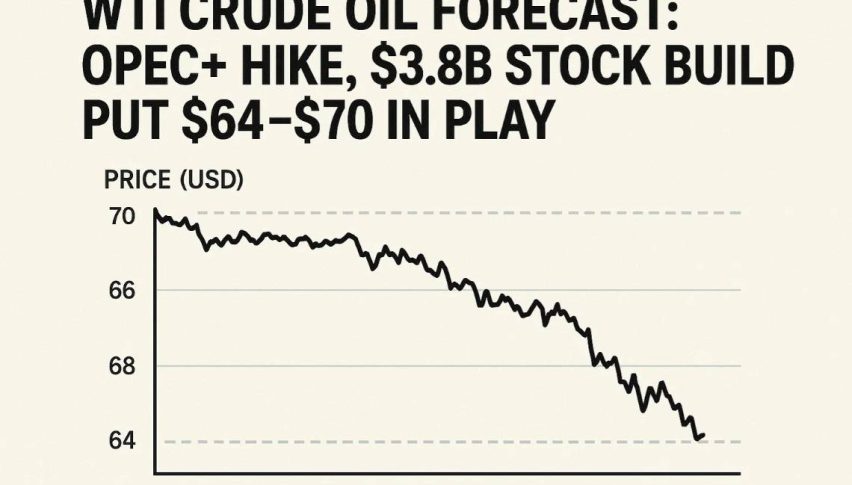

WTI Crude Oil Drops From a 5-Month High of $ 43.50 – Economic Growth Concerns!

Crude oil prices were unable to continue their overnight 5-month high gains, pulling back toward the $ 41.66 level, mainly due to the...

During Thursday’s Asian trading session, the WTI crude oil prices were unable to continue their overnight 5-month high gains, pulling back toward the $ 41.66 level, mainly due to the worries that the economic recovery could be halted, due to the resurgence of the coronavirus. In the meantime, the geopolitical tensions between the world’s two biggest economies also weighed on the risk sentiment and contributed to the oil losses. Meanwhile, the weakness of the broad-based US dollar, triggered by multiple factors, became the key factor that capped further losses in the crude oil prices. Let me remind you; the overnight gains in crude oil were supported by the upbeat API Weekly Crude Oil report, and the sharp declines in the US dollar also resulted in a recovery for crude. At the moment, crude oil is trading at $ 41.80 and consolidating between 41.65 and 42.45.

On the US-China front, the rising tensions between the United States and China continued to pick up pace. It is worth recalling that President Trump announced yesterday that TikTok has to find a new buyer within one-month, or it will be banned in the US, in the wake of significant security threats. China’s ambassador to the US recently warned against the US move to send ships to the South China Sea, claiming that this could raise further tensions between the nations and harm the trade deal. On the flip side, the US secretary of state, Mike Pompeo criticized China and advised American citizens to avoid travelling to China. These lingering Sino-US tensions could keep crude oil prices under pressure as we head into the weekend.

Apart from this, the fears of rising numbers of COVID-19 cases in the US, Australia, Japan and some of the notable Asian nations, like India, continue to fuel worries that the economic recovery could be stopped in its tracks. These fears were further boosted by the Federal Reserve’s recent comments that the second wave of the virus was slowing the economic recovery in the world’s biggest economy. World Health Organization (WHO) President, Dr. Tedros Adhanom Ghebreyesus, also added fuel to the fire, stating that the perfect vaccine for the pandemic may never be found, and this also weighed on oil prices.

Due to the coronavirus damages, the ADP report revealed a rise of only 167,000 private-sector jobs in July, while the manufacturing employment is still depressed, as per the ISM report. In the meantime, the broader services sector also seems depressed, and this data adds a further burden to the broad-based US dollar, capping further losses in crude oil.

As a result, the broad-based US dollar failed to halt its losing streak, taking the further offer on the day, as the United States was still facing damages from the coronavirus woes, as is evident from the downbeat US data. However, the losses in the US dollar helped to limit deeper losses in the crude oil price, as it is inversely related to the price of the US dollar. Meanwhile, the US Dollar Index, which tracks the greenback against a basket of other currencies, dropped to 92.823. Looking forward, the market players will keep an eye on the risk catalysts, like the US stimulus headlines and COVID-19, news for fresh direction ahead. Good luck!

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account