WTI Crude Oil Fails to Stop its Losing Streak – Trade Plan!

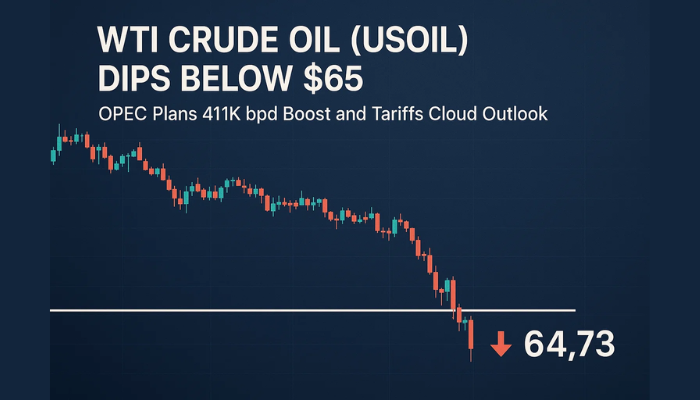

The WTI crude oil is trading at 37.55 level, holding mostly below an immediate resistance level of 38.50 level. Below this, the WTI may trad

During Friday’s Asian trading session, the WTI crude oil prices extended their previous losses, dropping further, to around the $ 37.00 level. However, the bearish sentiment surrounding the oil prices was mainly driven by the unexpected rise in US stockpiles, and slow demand, due to the resurgence of the COVID-19 pandemic. Furthermore, the losses in crude oil could also be attributed to the rising number of coronavirus (COVID-19) cases and the US-China tussle. It is worth mentioning that the on-going rise in the numbers of COVID-19 cases continues to fuel worries that the recovery of the global economy could come to a halt, which is adding a further burden to the crude oil prices.

On the contrary, the news that Saudi Aramco is increasing domestic fuel prices to compensate for overseas discounts became the key factor that is capping a further downside momentum in crude oil. Furthermore, the capping of losses in crude oil could be a result of the weakness of the broad-based US dollar, triggered by the risk-on market sentiment. At the moment, crude oil is trading at $ 37.24 and consolidating in the range between 36.98 and 37.38.

On the data front, the US Energy Information Administration (EIA) reported a 2.032 million-barrel build in crude inventories for the week ended September 4, against expectations of a 1.335 million-barrel draw. Thus, the EIA’s data is following in the footsteps of private inventory numbers released by the American Petroleum Institute, which rose beyond -6.36M, before +2.97M during the stated period.

The US refineries gradually returned to work after having shut down production sites earlier, due to hurricanes in the Gulf of Mexico and further afield. This could therefore be considered the key factor behind the rise in stockpiles, against all expectations. The WTI crude production is resuming after several storms, but a weaker demand forecast and the start of the maintenance season will keep the oil prices under pressure.

Coronavirus (COVID-19) fears could also be putting pressure on the oil prices. Let me remind you that the traders resumed the booking of tankers again, in order to store crude oil and diesel, as oversupply worries continued to mount. As per the latest report by Johns Hopkins University, there were approximately 28 million COVID-19 cases globally, as of September 11.

Apart from this, the on-going tension between China and the US is also favoring the oil bears. It is worth reporting that the US moves to punish Chinese technology companies and diplomats through several sanctions, and China’s warnings to the US over the visa restrictions, keep fueling the on-going conflict. Another factor that is challenging the market trading sentiment is the on-going Brexit worries.

On the contrary, the crude oil prices might gain some support from the news suggesting that Saudi Aramco has raised domestic fuel prices. This came after the Arab nation offered discounts to the US and Asian buyers earlier in the week.

On the USD front, the broad-based US dollar failed to maintain its earlier gains, dropping on the day, as US tech stocks continued their second week of selloffs. The continued bullish momentum in the euro, after the European Central Bank’s latest policy announcement, and a delay in the US Congress over pandemic relief funding, also weighed on the US dollar. Moreover, the losses in the US dollar could also be associated with a risk-on market sentiment. However, the losses in the US dollar turned out to be a major factor that capped any further downside momentum for the oil prices, as the price of oil is inversely related to the price of the US dollar. Meanwhile, the US Dollar Index, which tracks the greenback against a basket of other currencies, had dropped by 0.10%, to 93.295, by 9:40 PM ET (2:40 AM GMT).

Looking ahead, the market traders will keep their eyes on the US Consumer Price Index (CPI) for August, which is expected to come it at 1.2% against 1.0% YoY. Meanwhile, the release of Baker Hughes US Oil Rig Count, which has risen to 181, will be key to watch. Moreover, the updates surrounding the Sino-US tussle, as well as Brexit related headlines, have not lost any significance.

Daily Support and Resistance

S1 33.51

S2 35.63

S3 36.82

Pivot Point 37.74

R1 38.94

R2 39.86

R3 41.97

WTI crude oil is trading at the 37.55 level, holding mostly below an immediate resistance level of 38.50. Below this, trading in WTI may be bearish until the 37.19 level. Violation of this range could determine the next trend. For example, if the odds of a selling trend remain strong upon the breakout at the 37.19 level, it may lead the oil prices towards a support of 36.44. Conversely, the bullish crossover at the 38.50 level could lead oil prices until the 39.45 resistance mark. Good luck!

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account