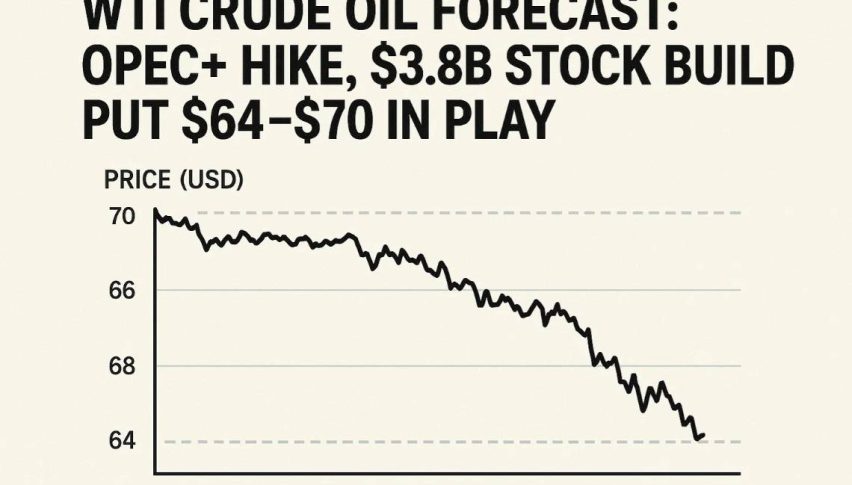

Crude Oil Consolidates Below 40 – Positive Talks Between Russian President and Saudi Crown Prince in Play!

WTI crude oil prices failed to stop its previous day losing streak and took further offer around below $40.00 level on the day mainly due ..

During Wednesday’s Asian trading session, the WTI Crude Oil prices failed to stop their losing streak of the previous day, taking further offers under the $ 40.00 level on the day, mainly due to the renewed concerns over the global economic recovery, as the number of COVID-19 cases continues to rise in Europe and the US. Let me remind you that the number of global cases crossed the 38 million mark, as of Oct. 14, according to Johns Hopkins University data. In the meantime, the prevalent fears of no US aid package being approved before the US elections, and the delay in the development of a COVID-19 vaccine, have also exerted downside pressure on the crude oil prices.

Across the pond, the geopolitical tensions between China and some notable countries, like the US and Australia, have also contributed to the slump in the oil price. On the other hand, the fresh bullish bias of the broad-based US dollar, triggered by the risk-off market sentiment, also dragged the crude oil prices down, as the price of oil is inversely related to the price of the US dollar. On the contrary, the positive talks between Russian President Vladimir Putin and Saudi Crown Prince Mohammed bin Salman, over the oil production cuts, have become the key factor that has helped to limit deeper losses in the crude oil prices. At the moment, crude oil is trading at $ 39.95 and consolidating in the range between 39.81 and 40.30.

As we have already mentioned, the fears of rising numbers of COVID-19 cases in the US, Europe and some of the notable Asian nations, like India, are continually fueling worries over economic recovery, which have undermined the crude oil prices. According to Johns Hopkins University data, the number of global cases has crossed the 38 million mark, as per the latest report on Oct. 14. The US, which is the biggest oil consumer globally, is still not showing any signs of decreasing infection rates, and this has raised concerns that the fuel demand will continue to stumble. On the European front, the number of newly confirmed cases per day has increased to 5,132, bringing the total number of infections in Europe up to 334,585, while the death toll has also risen by 40, taking the total to 9,677. There were 4,122 new cases the previous day, with 13 deaths, as per the latest data.

Apart from this, the prevalent fears that there will be no US aid package before the US elections, and the delayed progress in the development of a COVID-19 vaccine, also played a major role in undermining the crude oil prices. In the meantime, the intensifying fears of national lockdowns in Europe have added a further burden to the crude oil prices. Likewise, the on-going differences between the European Union (EU) and the UK are keeping the traders cautious.

On the US-China front, the rising tensions between the United States and China continued to pick up pace after China showed its disapproval over the White House arms sale to Taiwan, and China’s recent ban on the use of Aussie coal for power stations. This put additional pressure on the market sentiment, contributing to the losses in crude oil.

Moreover, the losses in the crude oil prices were further bolstered by the reports suggesting that Eli Lilly and Co. (NYSE: LLY) had suspended the government-led clinical trials of its COVID-19 antibody treatment, just one day after Johnson & Johnson (NYSE: JNJ) had halted its clinical trials for its COVID-19 vaccine, due to the illness of a participant. This, in turn, increased the safe-haven demand in the market.

As a result, the broad-based US dollar managed to put an end to its bearish bias, taking some fresh bids on the day. However, the gains in the US dollar could be short-lived or temporary, due to the weaker US Consumer Price Index (CPI) data and soft US inflation numbers, which incited fears of an economic slowdown. However, the gains in the US dollar could also be a key factor that has kept the crude oil prices down, as the price of oil is inversely related to the price of the US dollar. Meanwhile, by 10:12 PM ET (2:12 AM GMT), the US Dollar Index, which tracks the greenback against a basket of other currencies, had risen by 0.01%, to 93.550.

Across the pond, the Organization of the Petroleum Exporting Countries, or OPEC, has forecast that the fuel demand in 2021 is likely to increase by 6.54 million barrels per day (BPD), to 96.84 million, which is 80,000 BPD fewer than its September forecast, as most countries have re-imposed lockdowns after the second wave of the coronavirus, which has put pressure on the oil prices.

On the contrary, Russian President Vladimir Putin and Saudi Crown Prince Mohammed bin Salman, two of the world’s biggest oil producers, discussed the prevailing market conditions, whereby they also gave their assurance that OPEC and their producer allies, such as Russia – a group is known as OPEC+ – will adhere to their promises to reduce oil production cuts from January. This, in turn, has become the key factor that is helping to limit deeper losses in oil prices.

Looking forward, traders will keep their eyes on Japan’s Industrial Production figures for August, which are expected to remain unchanged at -13.3% YoY. Apart from this, the continuous drama surrounding the US-China relations and updates on the US stimulus package will not lose any significance. Good luck!

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account