U.S. Stocks May See Early Rally As Traders Digest Rate Cut

After ending yesterday's session moderately lower following late-day volatility, stocks are likely to show a strong move to the upside in early trading on Thursday. The major index futures are current...

After ending yesterday’s session moderately lower following late-day volatility, stocks are likely to show a strong move to the upside in early trading on Thursday. The major index futures are currently pointing to a sharply higher open for the markets, with the S&P 500 futures jumping by 1.6 percent.

The considerable upward momentum on Wall Street comes as traders continue to digest the Federal Reserve’s decision on Wednesday to slash interest rates by 50 basis points.

Fed officials also forecast continued rate cuts over the comings months and into next year, generating optimism the central bank will be able to engineer a soft landing for the economy.

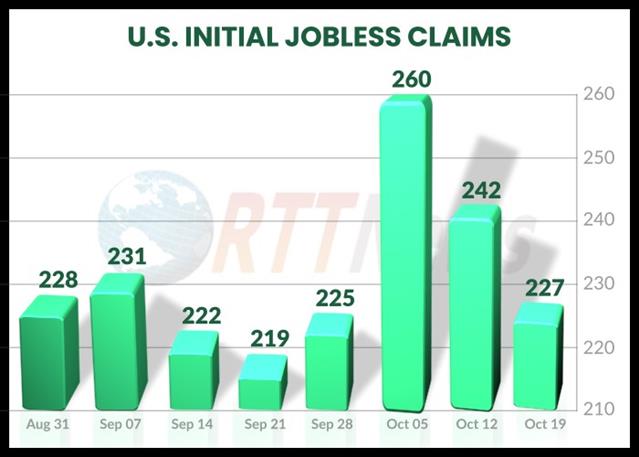

Potentially adding to the buying interest, the Labor Department recently released a report showing first-time claims for U.S. unemployment benefits unexpectedly fell to a nearly four-month low in the week ended September 14th.

The report said initial jobless claims slid to 219,000, a decrease of 12,000 from the previous week’s revised level of 231,000.

Economists had expected jobless claims to come in unchanged compared to the 230,000 originally reported for the previous week.

With the unexpected decline, jobless claims fell to their lowest level since hitting 216,000 in the week ended May 18th.

A separate report released by the Federal Reserve Bank of Philadelphia showed its reading on Philadelphia-area manufacturing activity returned to positive territory in the month of September.

Shortly after the start of trading, the National Association of Realtors is scheduled to release its report on existing home sales in the month of August. Existing home sales are expected to decrease to an annual rate of 3.90 million in August after jumping to a rate of 3.95 million in July.

The Conference Board is also due to release its report on leading economic indicators in the month of August. The leading economic index is expected to dip by 0.3 percent in August after falling by 0.6 percent in July.

Stocks saw considerable volatility late in the trading session on Wednesday following the Federal Reserve’s announcement of its decision to lower interest rates. The major averages showed wild swings back and forth across the unchanged line before eventually closing in negative territory.

The Dow and the S&P 500 reached new record intraday highs immediately following the Fed announcement but finished the day in the red.

The Dow fell 103.08 points or 0.3 percent to 41,503.10, the S&P 500 slipped 16.32 points or 0.3 percent to 5,618.26 and the Nasdaq dipped 54.76 points or 0.3 percent to 17,573.30.

In overseas trading, stock markets across the Asia-Pacific region moved mostly higher during trading on Thursday. Japan’s Nikkei 225 Index surged by 2.1 percent, while China’s Shanghai Composite Index climbed by 0.7 percent.

The major European markets have also shown strong moves to the upside on the day. While the French CAC 40 Index has jumped by 2.0 percent, the German DAX Index is up by 1.7 percent and the U.K.’s FTSE 100 Index is up by 1.0 percent.

In commodities trading, crude oil futures are climbing $0.70 to $71.61 a barrel after dipping $0.28 to $70.91 a barrel on Wednesday. Meanwhile, after inching up $6.20 to $2,598.60 an ounce in the previous session, gold futures are rising $11.90 to $2,610.50 an ounce.

On the currency front, the U.S. dollar is trading at 143.45 yen versus the 142.29 yen it fetched at the close of New York trading on Wednesday. Against the euro, the dollar is valued at $1.1130 compared to yesterday’s $1.1119.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account