btc-usd

Forex Signals Brief Aug 18: From Powell to Walmart and PANW Earnings This Week

Markets enter a pivotal week with a heavy lineup of central bank decisions, inflation releases, and corporate earnings that could define...

•

Last updated: Monday, August 18, 2025

Quick overview

- Markets are poised for a significant week with central bank decisions, inflation data, and corporate earnings that could influence equities, currencies, and commodities.

- U.S. retail sales rose 0.5% in July, indicating steady consumer demand, while inflation pressures have tempered expectations for a September Fed rate cut.

- Geopolitical developments include a meeting between U.S. and Russian leaders, which brought cautious optimism regarding Ukraine.

- Key market events this week include Fed Chair Jerome Powell's speech, inflation reports from Canada and the UK, and earnings from major corporations like Home Depot and Walmart.

Live BTC/USD Chart

BTC/USD

0.0000

MARKETS TREND

Markets enter a pivotal week with a heavy lineup of central bank decisions, inflation releases, and corporate earnings that could define near-term momentum across equities, currencies, and commodities.

U.S. Retail Sales Steady in July

U.S. retail sales rose 0.5% in July, matching expectations and following an upwardly revised 0.9% increase in June (originally reported at 0.6%). The ex-auto measure also aligned with forecasts, signaling steady underlying consumer demand. The control group, a key gauge for GDP that strips out volatile components, advanced 0.5%, slightly exceeding the 0.4% projection after June’s robust 0.8% growth.

Inflation Pressures and Fed Outlook

Traders were reminded of the lingering impact of tariffs as import prices posted a stronger-than-expected 0.4% gain, defying projections for no change. This came against a mixed inflation backdrop earlier in the week, the Producer Price Index (PPI) rose sharply by 0.9%, well above forecasts, while Consumer Price Index (CPI) increased 0.3%, in line with estimates.

The combination has cooled expectations for a September Fed rate cut, with markets now pricing it at 94% versus 100% earlier in the week. Fed officials have adopted a more cautious tone, with Austan Goolsbee noting “a note of unease,” particularly over stubbornly high service-sector inflation.

Geopolitical Developments

On the geopolitical front, U.S. President Donald Trump and Russian President Vladimir Putin met in Alaska over the weekend. Both leaders made encouraging remarks on Ukraine, including the possibility of a summit with President Volodymyr Zelenskiy. Trump remarked, “Let the world be at peace,” signaling cautious optimism on cease-fire progress.

Key Market Events for the Week Ahead

This week’s lineup combines high-stakes central bank commentary, inflation readings, and heavyweight earnings reports, setting the stage for potential volatility. Powell’s Jackson Hole remarks will anchor the narrative, but data from New Zealand, Canada, the UK, and Europe could inject further market-moving surprises. With corporate giants from mining, retail, and tech all reporting, investors should prepare for a week where policy signals and earnings momentum intersect to drive sentiment.

Powell at Jackson Hole (Friday, 10:00 AM ET)

- The highlight of the week, Fed Chair Jerome Powell’s speech will shape expectations for the September FOMC decision.

- Investors will be listening closely for signals on whether a 25 bps cut is locked in and for any clues on the Fed’s outlook for year-end policy.

Reserve Bank of New Zealand (Tuesday night, 10:00 PM ET)

- RBNZ is widely expected to cut rates by 25 bps, aligning with global dovish trends.

- Markets will watch whether policymakers hint at further easing or adopt a wait-and-see stance.

Canada CPI (Tuesday, 8:30 AM ET)

- A key test for the Bank of Canada’s policy path.

- Any upside surprise could temper easing bets, while a soft print reinforces expectations of a cut later this year.

UK CPI (Wednesday)

- Inflation trends remain critical after the Bank of England’s hawkish rate cut at its last meeting.

- Governor Andrew Bailey’s remarks on Saturday could clarify how cautious or aggressive the BoE intends to be.

Europe & U.S. PMIs + Jobless Claims (Thursday)

- Flash PMIs will give the first look at August economic activity across manufacturing and services.

- Initial jobless claims will also be key in gauging U.S. labor market resilience, especially after recent mixed data.

Corporate Earnings in Focus

- BHP Group (H2 2025 Results): A bellwether for the mining sector, with results giving insight into global demand trends for commodities.

- Palo Alto Networks (Q4 2025): Cybersecurity spending remains robust; results could signal whether the sector maintains growth momentum amid tighter IT budgets.

- Home Depot (Q2 2025): Closely watched for signs of U.S. consumer and housing market strength.

- Walmart (Q2 2026): Retail giant’s earnings will be a gauge of household spending and inflation’s impact on consumers.

Last week, markets were quite volatile once, with gold retreating and then bouncing to finish the week close to $4,000 but yesterday it retreated again. EUR/USD continued the upward move toward 1.17, while main indices closed higher. The moves weren’t too big though, and we opened 35 trading signals in total, finishing the week with 23 winning signals and 12 losing ones.

Gold Holds Despite Pressure

Gold prices briefly dipped below $3,268/oz following the Fed’s decision last week to keep rates steady. The metal eventually stabilized near $3,500/oz, ending the session down $21.52 (-0.63%). Technical backdrop: Support from the 20-week SMA and falling U.S. unemployment rates continue to provide a bullish undertone. Key breakout zone: The $3,450–$3,500 level remains a critical threshold for bulls.

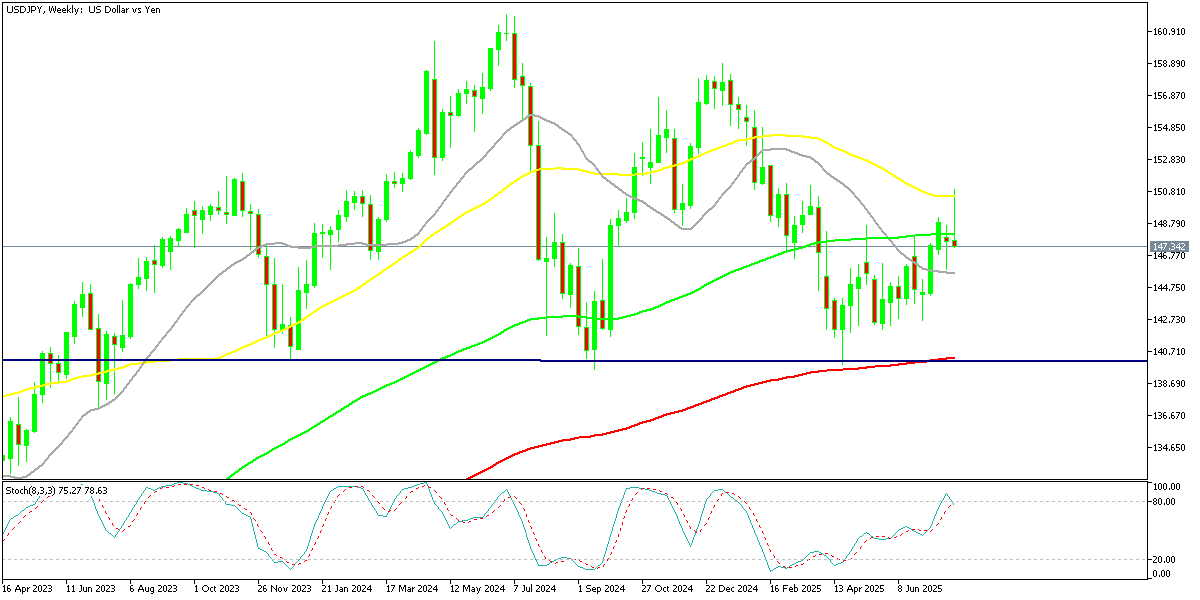

Dollar-Yen Volatility

Currency markets saw turbulence as the U.S. dollar briefly topped ¥150 earlier in the week, driven by yield differentials and Japanese capital flows. However, a combination of profit-taking and a stronger yen—spurred by weak U.S. jobs data—pulled the USD/JPY down by four yen from the highs.

USD/JPY – Weekly Chart

Cryptocurrency Update

Bitcoin and Ethereum: Diverging Momentum

The cryptocurrency market has remained active through the summer. Bitcoin (BTC) surged to record highs above $123,000 in July and $124,000 in August, fueled by institutional demand and technical momentum. Optimism suggested BTC could be approaching the $150,000 mark.

However, enthusiasm faltered after Treasury Secretary Scott Bessent confirmed the U.S. would not expand Bitcoin reserves and inflation data came in hotter than expected. This triggered a sharp correction, dragging BTC down to $117,000 over the weekend. Chart signals: Two consecutive doji candlesticks hinted at exhaustion, and the pullback found solid support at the 50-week SMA, reinforcing the long-term bullish trend.

BTC/USD – Weekly chart

Ethereum Extends 2024 Rally

Meanwhile, Ethereum (ETH) has surged past $4,300, its highest since 2021, and appears poised to challenge its all-time high of $4,860. The rally has been driven partly by retail enthusiasm, but fresh institutional flows and bullish chart setups provide additional support.

ETH/USD – Daily Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

ABOUT THE AUTHOR

See More

Skerdian Meta

Lead Analyst

Skerdian Meta Lead Analyst.

Skerdian is a professional Forex trader and a market analyst. He has been actively engaged in market analysis for the past 11 years. Before becoming our head analyst, Skerdian served as a trader and market analyst in Saxo Bank's local branch, Aksioner. Skerdian specialized in experimenting with developing models and hands-on trading. Skerdian has a masters degree in finance and investment.

Related Articles

Sidebar rates

Related Posts