btc-usd

Forex Signals Brief August 26: Okta, BNS and MDB Earnings Follow US Durable Goods

Today we have the US Durable Goods orders, to be followed by the Okta, MDB, and MDB Q2 earnings reports.

•

Last updated: Tuesday, August 26, 2025

Quick overview

- The US dollar rebounded today after a sharp drop following Fed Chair Jerome Powell's dovish remarks, closing higher against all major currencies.

- Political instability in France, triggered by a confidence vote announcement, pressured the euro and led to wider bond spreads.

- US equity markets started the week on a softer note, with the S&P 500 closing firmly in the red despite earlier positive momentum.

- US new home sales for July slightly exceeded expectations, but a monthly decline raised concerns about underlying demand.

Live BTC/USD Chart

BTC/USD

MARKETS TREND

Today we have the US Durable Goods orders, to be followed by the Okta, MDB, and MDB Q2 earnings reports.

USD Rebounds After Powell’s Dovish Signal

Following last Friday’s sharp drop triggered by Fed Chair Jerome Powell’s dovish remarks, the US dollar staged a notable recovery today. Although the move was orderly, the greenback steadily gained strength throughout the US session, ultimately closing higher against all major currencies. The euro emerged as the weakest performer, weighed down by renewed political instability in France.

French Political Risks Pressure Euro and Bonds

French Prime Minister François Bayrou announced a confidence vote scheduled for September 8th on sweeping budget cuts, prompting immediate pushback from opposition parties. The political uncertainty rattled markets, leading to wider French bond spreads and dragging the CAC 40 lower. The turbulence in Europe further supported the dollar’s advance.

Mixed Session for US Equities

On Wall Street, equity markets started the week on a softer note. The Nasdaq, despite trading in positive territory earlier in the session, gave up its gains to finish lower. The S&P 500 fared worse, never trading in positive territory and closing firmly in the red. The Dow also struggled, reflecting a fragile risk tone despite last week’s upbeat momentum.

US Housing Data Offers Modest Support

The day’s only major economic release, US new home sales for July 2025, slightly exceeded expectations at 0.652 million compared with forecasts of 0.630 million. However, the data revealed a 0.6% monthly decline, following a robust 4.1% increase in June. June’s figure was revised upward to 0.656 million from the initial 0.627 million, softening the impact of July’s dip.

Key Market Events Today

Durable Goods Orders

Markets now turn their focus to tomorrow’s durable goods report. Headline orders are expected to show a steep -5.0% m/m decline, primarily due to lower aircraft orders. Excluding transportation, orders are projected to be flat, underscoring weakness in underlying demand. Meanwhile, core capital goods orders are forecast to rebound 0.3% m/m after June’s -0.8% decline, though shipments are likely to remain stagnant—limiting near-term momentum for business investment.

Q2 Earnings Reports Scheduled for Today

Both Okta and MongoDB report after the bell today, with expectations centered on solid earnings growth. The results will not only highlight each company’s individual momentum but could also provide broader insight into enterprise software demand, cybersecurity spending, and cloud adoption trends going into the second half of 2025.

🔹 Okta, Inc. (OKTA)

- Announcement Timing: After Market Close (AMC)

- EPS Expectation: $0.85 per share

🔹 MongoDB, Inc. (MDB)

- Announcement Timing: After Market Close (AMC)

- EPS Expectation: $0.66 per share

Last week, markets were quite volatile once, with gold retreating and then bouncing to finish the week close to $4,000 but yesterday it retreated again. EUR/USD continued the upward move toward 1.17, while main indices closed higher. The moves weren’t too big though, and we opened 35 trading signals in total, finishing the week with 23 winning signals and 12 losing ones.

Gold Rebounds After Powell

Gold also joined the rally: after briefly dipping below $3,268/oz following the Fed’s steady-rate decision, the metal climbed nearly $50 higher by week’s end. Strong safe-haven demand and stable labor data lifted prices above the 100-day SMA, reinforcing bullish momentum. Technicals continue to highlight the $3,450–$3,500/oz zone as the next key breakout area.

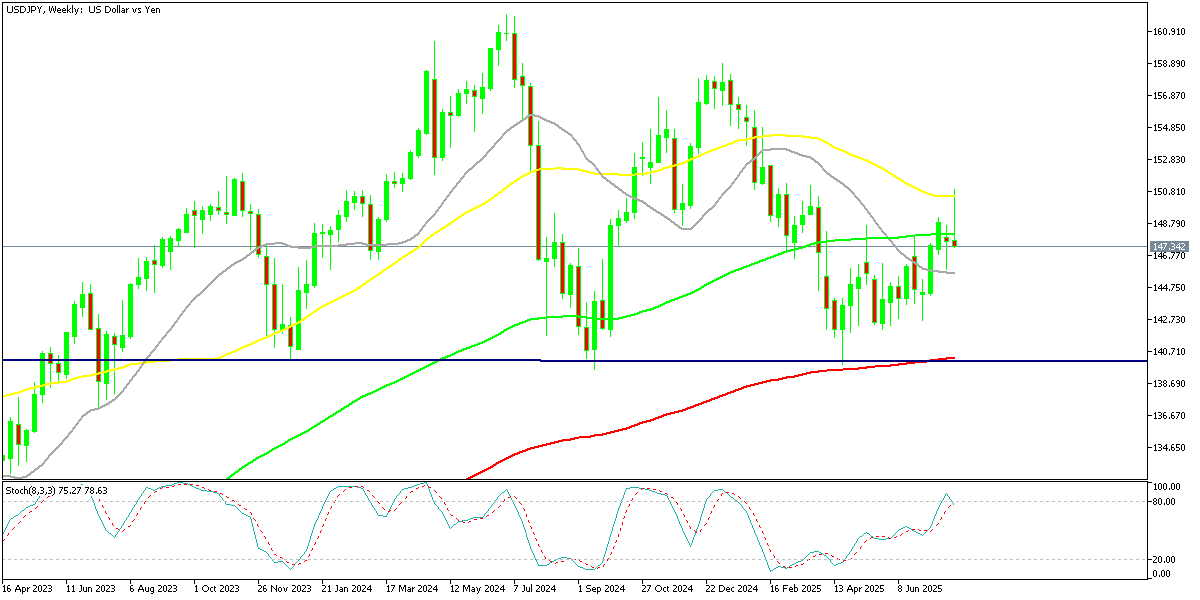

Yen Recovery from ¥150 Shock

Foreign exchange markets saw sharp swings. Early in the week, U.S. yield differentials and Japanese capital outflows pushed the dollar above ¥150, but disappointing U.S. jobs data triggered profit-taking, causing the USD/JPY to slide by four yen from its peak. The move underscored persistent volatility as traders weighed Japan’s intervention risks against evolving Fed expectations.

USD/JPY – Weekly Chart

Cryptocurrency Update

Bitcoin Returns Below $110K Support

Cryptocurrencies remained highly active over the summer. Bitcoin (BTC) climbed to fresh highs of $123,000 and $124,000 in July and August, supported by institutional inflows and technical strength. However, remarks from Treasury Secretary Scott Bessent ruling out U.S. increases to BTC reserves triggered a steep pullback, sending the coin down to $113,000 before recovering above $116,000 last week, however sellers returned and sent BTC below $110,000.

BTC/USD – Weekly chart

Ethereum Fails to Move Above $5K After Printing A New High

Ethereum (ETH) has been similarly strong, surging toward $4,800, its highest since 2021 and near its all-time peak of $4,860. Despite a dip last week, ETH found support at the 20-day SMA, with retail enthusiasm and renewed institutional participation driving fresh upside momentum. However buying resumed and on Sunday Eth/USD printed another record at $4,941.

ETH/USD – Daily Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

ABOUT THE AUTHOR

See More

Skerdian Meta

Lead Analyst

Skerdian Meta Lead Analyst.

Skerdian is a professional Forex trader and a market analyst. He has been actively engaged in market analysis for the past 11 years. Before becoming our head analyst, Skerdian served as a trader and market analyst in Saxo Bank's local branch, Aksioner. Skerdian specialized in experimenting with developing models and hands-on trading. Skerdian has a masters degree in finance and investment.