US Session Forex Brief, March 19 – Great UK Earnings and Employment Report Couldn’t Move the GBP with Brexit Uncertainty Bound to Continue

Brexit seems to be postponed further but indications point to a possible deal at some point

The period of weakness continues today again for the US Dollar. Everything has been gaining on the expense of the Buck. Safe havens such as the JPY and GOLD are on the uptrend and at the same time the risk assets such as the stock markets and the commodity Dollars are also climbing higher. Speaking of commodity Dollars, China said early this morning that it will strengthen inspections and testing of Coal imports, yet the Aussie didn’t dive lower like it did last week when China closed the Dalian port for coal imports. Australia exports lots of coal and and other raw materials to China, so this hurts relationships further between the two countries, but we should keep this in mind for the larger picture for the Australian Dollar.

Although, the UK was back in focus today. The employment report was quite impressive once again with unemployment rate ticking lower to 3.9% and the 3-month/year average hourly earnings remaining at the highs. The year/year weekly earnings climbed to the highest since 2008 before the financial crisis. But, the GBP is trading Brexit now so it ignored the data. Speaking of Brexit, everything points to another extension but we will see if it will be a long or a short one. The CAD is the strongest currency today as USD/CAD has lost around 100 pips today but most of that decline came in the last hour as Oil prices made new highs today.

European Session

- Oil Makes New High on OPEC Rhetoric – Yesterday we head OPEC officials comment about keeping production in check which helped crude oil prices remain upbeat. Today we hard more comments, this time from OPEC chief Barkindo, that the market is responding positively to OPEC+ meeting. He added that Venezuela is addressing power blackouts, it is ‘practically impossible’ to cut Iran oil to zero and most importantly, OPEC would not serve the best interest of the US. He is probably referring to Donald Trump’s tweets asking OPEC to keep Oil prices down.

- China Deepens the Rout with Australia – China closed the Dalian port to coal imports last week which hurt the Aussie. Today China says it has strengthened testing and inspections of coal imports. The AUD didn’t really mind these comments today but this will eventually weigh on the Aussie if the restrictions on Australian coal imports continue.

- Germany Doesn’t Want A Hard Brexit – The German European Affairs minister, Michael Roth, commented that Germany’s key demand is that there be no no-deal Brexit. He requests Britain to make a sensible proposal on how it wishes to proceed because the EU patience as a whole is being sorely tried. The UK must be clear that if delay goes beyond June, Britain must take part in EU elections. Germany needs clear and precise proposals on why extension is needed. Angela Merkel also spoke, saying that she will fight to the last minute for an orderly Brexit. So, no hard Brexit then.

- UK Employment Report – The UK employment report was once again great; the unemployment rate fell to 3.9% from 4.0% previously while 3-month/year earnings also remained at 3.4%, against a decline to 3.2% expected. Year/year average weekly earnings increased to 3.7% which is the highest since 2008. The employment change increased by 222k against 120k expected, so it was an upbeat report allover.

- European ZEW Economic Sentiment – The economic sentiment deteriorated in Britain last year and it reached the bottom at -24.7 points in October. But it started improving slowly since then and this month it was expected to come at -11 points from -13.4 points in February. Although, it beat expectations coming at -3.6 points. The sentiment for the whole of the Eurozone has been negative as well; it was expected to improve slightly from last month and come at -015.1 points but it jumped to -2.5 points, so the trend looks good.

- Brexit to Be Delayed Again – Huffington Post’s deputy political editor, Arj Singh, commented early today that there is still no breakthrough in government talks with DUP Party of Northern Ireland. That puts May in a difficult position for the next Brexit vote so the chances are that the UK will ask for another extension beyond March 29. EU leaders responded by planning a contingent offer on Brexit extension. But, the extension offer is unlikely to be finalized at the summit and the extension would be finalized in days before 29 March; the plan basically is to allow for May to try and get the deal through next week.

The US Session

- May Still Determined to Find a Way for the Brexit Deal to Pass – May’s spokesman made these comments just a while ago. and he added that the Prime Minister is prepared not to revoke Article 50. There is a determination from the cabinet to find a way for the Parliament to vote on a Brexit deal, a long delay to Brexit would be a failure by politicians. If there were to be a vote on Brexit deal on Wednesday, the government would have to submit a motion today and that hasn’t happened yet (so no vote this week). The PM will write to EU’s Tusk before this week’s summit on extending Article 50. The cabinet discussed ongoing talks with the DUP on Brexit.

- US Factory Orders – Factory orders turned negative in October and November last year. But they turned positive in December again, growing by 0.1%. Today’s report which is for January was expected to show a 0.3% increase in orders that month, but missed expectations coming at 0.1%. This shows that factory orders remain quite soft.

- NZD GDT Price Index – Today is that day of the month again when the auction for global dairy products takes place in New Zealand. Dairy prices had a negative run from August last year until mid-November. But the trend reversed and shifted to positive since then. Last time, prices rose by 3.3%, so let’s see if the positive trend will continue today as well.

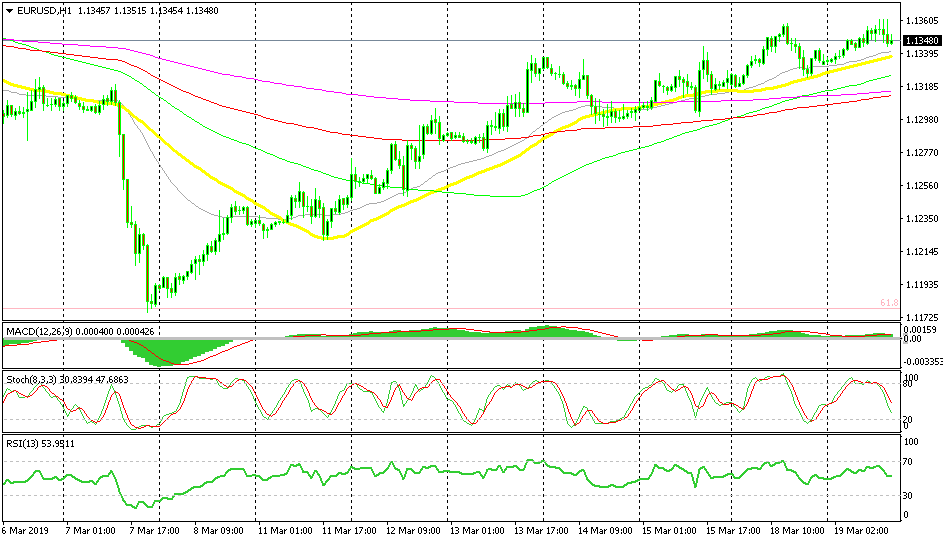

Bullish EUR/USD

- The trend is bullish

- The 50 SMA is waiting to provide support below

- The price is retracing lower

The 50 SMA has been a solid support indicator for EUR/USD in more than a week

Last week we got caught on the wrong side of the EUR/USD as this pair made a bullish reversal and climbed more than 100 pips higher. This week the uptrend is stretching further so we have changed direction and have a buy signal from yesterday. In the last few hours though, EUR/USD has been trying to retrace lower but the price is quickly becoming oversold as stochastic shows which means the retrace will be complete. The 50 SMA (yellow) is also waiting to provide support lower.

In Conclusion

The US Dollar continues the strange weak period. The factory orders didn’t help much as they came soft for another month, but the demand for safe havens has dried up in the last couple of hours as USD/JPY and EUR/CHF climb higher, although, Gold continues to march higher. So, these are the markets right now.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts