US Session Forex Brief, May 15 – GBP Keeps Sliding as We Head Towards the Next Brexit Vote Without Anything Changing

Most of economic data today has been on the soft side and the sentiment is turning even more sour in financial markets

Today is pretty packed with economic data, starting with Australian wage price index for Q1 which missed expectations and the consumer sentiment. After that, a round of data was released from China with fixed asset investment, industrial production and retail sales all missing expectations and declining considerably from the previous month, especially industrial production. This shows that the Chinese economy is still weakening and the trade war which has precipitated will make things worse in the coming months.

There was a lot of Brexit chatter also around. But, despite the UK Brexit Secretary trying to sound optimistic, markets think that the next vote for the Brexit bill which will take place in about two weeks will not pass once again. This will be the last vote and if it fails, Britain will end up either with no deal or without Brexit at all.

European Session

- German Prelim GDP – The economy contracted by 0.2% in Q3 of last year and fell flat in Q4 in Germany. But it was expected to grow by 0.4% in Q1 of this year and today’s GDP came as expected. German officials sounded optimistic after that with the Economy Minister Altmier saying that Q1 GDP was a ‘first ray of hope’ after two quarters without expansion. But he noted that growth data is no reason to give the all-clear while international trade disputes remain unresolved. Germany must do everything possible to find acceptable solutions to free trade and the government must help companies and lower corporate, energy taxes. He continued by saying that the economy hasn’t fully emerged from weak period although the domestic demand was strong in Q1. Recovery will only be sustainable if external environment improves and indicators point to subdued development of exports in the coming months.

- China is Still Standing its Ground – China’s foreign ministry commented early this morning that if US doesn’t want to do business with us, others will fill the gap. The trade dispute will have some effects on the Chinese economy but they can be overcome. They have full confidence in China’s economic prospects. But today’s figures paint a different picture, as we mentioned above. China hopes that the US will stop using national security as pretext to suppress its firms. Urges US to create fair environment for Chinese companies. Trump’s tweet on US farmers confuses the truth, the US is the one defining the trade dispute as being a trade war and China is only taking actions in self defense.

- Brexit Talk – The DUP’s Dodds started the Brexit comments today and he said that May’s deal is doomed unless something has changed. There must be real change to protect the economic and constitutional integrity of the UK and deliver Brexit. UK trade secretary, Jeremy Hunt, followed with comments such as lawmakers will have to consider consequences of failing to deliver a Brexit deal and that continuing down the current path takes us to potential revocation of Article 50 or leaving without a deal. UK Brexit Secretary Stephen Barclay tried to calm things down as he said that Labour and Tories are closer on Brexit than what the image suggests. Brexit talks with Labour have been ‘serious’ and ‘challenging’. Cross-party talks need to come to a conclusion. Parliament will have the opportunity to vote on withdrawal bill in the 1st week of June

- Eurozone GDP – The GDP number for Q1 came as expected at 0.4%. GDP YoY also remains unchanged at 1.2% as previous. This report was pretty similar to the German GDP report which was released this morning showing a 0.4% expansion in Q1. Flash employment was expected to tick lower to 0.2%, but beat expectations, remaining unchanged at 0.3%.

US Session

- Canadian CPI Inflation Report – Inflation report from Canada was released a while ago. Inflation came as expected at 0.4% for April as expected, down from 0.7% in March. YoY CPI ticked higher to 2.0% as expected, from 1.9% previously. Although median CPI ticked lower to 1.9% against 2.0% expected. Common CPI remained unchanged at 1.8% vs 1.8% expected. Trimmed mean CPI also ticked lower to 2.0% vs. 2.1% expected, so inflation report was a tad on the soft side.

- US Retail Sales – Retail sales posted a nice jump in March and was revised higher to 1.7% from 1.6% previously reported, but that doesn’t change the fact that sales turned negative the following month. Retail sales report today showed a 0.2% decline in retail sales for April against a 0.2% increase expected. At least the core retail sales which excludes autos remained positive at 0.1% against 0.7% estimates. The prior month was revised higher as well to 1.3% from 1.2% previously reported. Retail sales excluding auto and gas turned negative, coming at -0.2% against 0.3% estimated. Last month’s sales excluding auto and gas were revised higher to 1.1% against 0.9% previously reported while the control group remained flat at 0.0% vs 0.3% estimate. Last month was also revised higher to 1.1% versus 1.0%.

- US Industrial Production – The industrial production turned negative in January declining by 0.6% and they turned negative again in March, declining by 0.1%. Although, today’s report which will be for April is expected to show that production remain unchanged at 0.0% which is not good. But at least it is not expected to decline again.

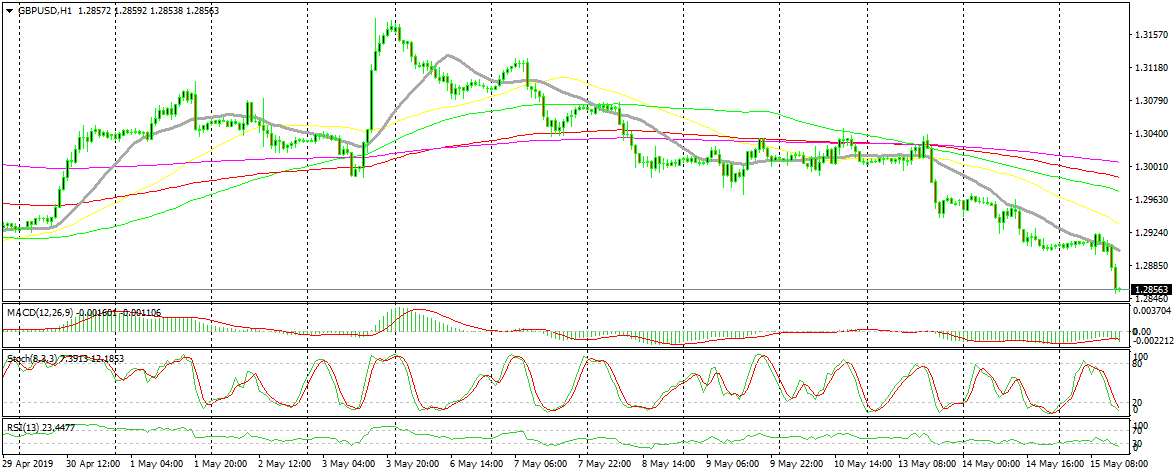

Bearish GBP/USD

- The trend remains bearish

- The 20 SMA is providing resistance

- Fundamentals are bearish

The 20 SMA has now turned into resistance

GBP/USD has turned pretty bearish in the last two weeks, losing more than 300 pips during this decline. In fact, the decline is picking up pace which can be spotted by the 20 SMA (grey) which has been providing resistance in the last two days. The price hasn’t even retraced higher before making the next bearish move, but the 20 SMA keeps pushing it down. Fundamentals are getting increasingly bearish as we head towards Brexit without any change, so we will wait for the 20 SMA to catch up again and probably go short when that happens.

In Conclusion

Markets have been pretty quiet today, moving pretty slowly, but they are picking up pace now. And it seems that the sentiment is turning negative again as risk assets slide lower. The US retail sales and Canadian inflation came out a bit on the soft side which is not helping the sentiment, and risk aversion is increasing now.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account