US Session Forex Brief, June 5 – The USD Keeps Declining on Services Day

The US ISM non-manufacturing came much better than expected, but the USD continues to be bearish on the day

The day started with the Australian GDP report coming out early this morning and the economy in Q1 grew by 0.4% as expected. Although, the economy has slowed down since then, so I expect the GDP report for Q2 to be weaker. Monday was a manufacturing day with reports for this sector being released from major economies, while today is a day for services. We had a number of services report being released in the European session, while later the US ISM non-manufacturing report will be released.

Even in Britain which is in the middle of a big mess, the service activity expanded last month, while manufacturing fell into contraction. The European Commission started the disciplinary procedure against Italy today, but EUR/USD continued to climb on more USD weakness, especially after the soft ADP employment figures released a while ago.

European Session

- Final Eurozone Services PMI – The Eurozone economy has slowed considerably and the manufacturing sector is in deep contraction, but at least the service sector is holding up well. The German services PMI which was released this morning increased to 55.4 points from 55.0 previously, although the French services PMI moved lower to 51.5 points from 51.7 points. But the Eurozone services PMI was mostly affected by Germany and the Eurozone services PMI moved higher to 52.9 points from 52.5 previously as expected.

- UK Services PMI – The services report from the UK was released just a while ago. Some of the other sectors of the economy have dived into contraction, so there was a good chance that to see a negative services number today. But, the activity in this sector increased this month and the PMI indicator moved to 51 points in May against 50.6 points expected, up from 50.5 points in April. Although, composite PMI remained unchanged at 50.9 points as it was against 51.0 expected. The services improved slightly last month but the main increase came from the expectations component, which rose from 63.9 in April to 65.4 in May. As a whole, the composite reading remains unchanged and the surveying firm Markit notes that this suggests that the UK economy is “close to stagnation”.

- Eurozone PPI Inflation – The PPI (producer price index) decreased in the last two months of last year in the Eurozone as Oil prices were on a free-fall, but they increased in the first two months of this year. Although, we saw another reversal in March as last month’s report showed and PPI declined by 0.1%, For April, expectations were for a 0.4% increase, but PPI inflation declined again by 0.3%.

- China Playing Good Cop – China’s commerce ministry commented earlier that trade differences with US should be resolved via dialogue, negotiations. Trade talks should be based on mutual respect. They hoped that the US would stop its wrongdoings and meet them halfway.

- Retail Sales – Retail sales posted a big decline of 1.6% in December, but they increased in January and February this year. Although, in March sales fell flat at 0.0%. Today’s report was expected to show another decline of 0.5% but they beat expectations, although they still declined by 0.4%.

- European Commission Starts EDP on Italy – Towards the end of last year, we saw quite a commotion between the EU and Italy. Italy’s debt is pretty high at 130% of the county’s GDP and they were aiming for the deficit this year to be around 2.4% of the GDP, but after the clash with the EU they pulled it lower to around 2%. But that was just on paper, because the reality is harsher. The economic weakness continues and now the Italian government wants to increase the deficit above 3% which is the ceiling by EU rules, which was broken in France’s case. The European Commission has started the disciplinary procedure on Italy today. The EU commission commented that Italy’s growing debt justifies the launch of a disciplinary procedure. EU Warns about Italian debt increasing due to ‘snowball effect’, saying that Italy is backtracking from structural overhauls, pension reform. Greece’s fiscal measures are a cause for concern as well.

- EU’s Dombrovskis on Italy – Italy hasn’t complied with debt criterion. Excessive debt procedure (EDP) is warranted for Italy. Recent Italian measures have damaged public finances. Recent policy choices have been damaging for the Italian economy. Italy’s growth has almost come to a halt.

US Session

- US ADP Non-Farm Employment – The ADP non-farm employment was declining during the first four months of this year, falling from 270k to 128k in April. Although we saw a decent jump to 270k again last month. This month was expected to post another decline to 185k, but the decline was much more with the ADP number coming at just 27k new jobs, which sent the USD for another ride down a while ago.

- US Final Services PMI – The US economy has been holding up well compared to the rest of the globe during the past year as we have seen some increased weakness in major global economies during this time. But, the US is joining the rest of the globe as the US economy also slowed down considerably in the last few months, with manufacturing and services PMI indicators falling close to stagnation. US services PMI declined to 50.9 points in May as the initial reading showed and the final reading remained the same.

- US ISM Non-Manufacturing PMI – This indicator is the best performing in the US economy right now. ISM non-manufacturing PMI also cooled off in the last two months but it remains in a decent place at 55.5 points. For May, this indicator was expected to tick higher to 55.6 points and it beat expectations coming at 56.9 points.

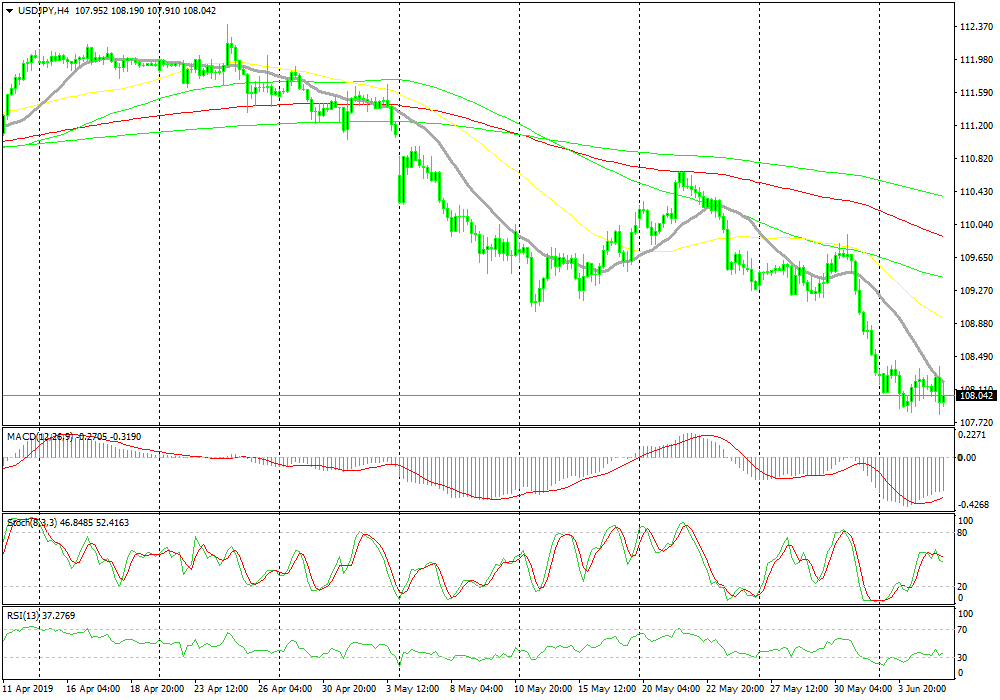

Bearish USD/JPY

- The main trend remains bearish

- The 20 SMA is pushing the price down

- Fundamentals are still bearish for this pair

The area around 108.20-30 has been tough to overcome

USD/JPY has turned pretty bearish in recent weeks as trade tensions escalate and the global economy weakens. The JPY has strengthened as a safe haven currency, together with Gold. USD/JPY broke below 108 yesterday but today it has been retracing higher during the European session. However, the buyers were having difficulties at the 20 SMA (green) on the H4 chart and the resistance level at 108.20-30. So we decided to sell there and booked profit a while ago. Although, the price still remains bearish for this pair.

In Conclusion

The US ISM non-manufacturing PMI came better than expected, showing that this sector is in good shape despite the recent economic weakness in the US. The USD made an attempt to turn bullish but it is a pretty weak attempt so far, so the USD weakness continues despite a great non-manufacturing report. But, we will follow it to see if it will finally turn bullish after four really bearish days.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts