ECB Seems Content With Loose Monetary Policy

The ECB has eased the monetary policy, but the attitude remains dovish, so further easing is on the cards

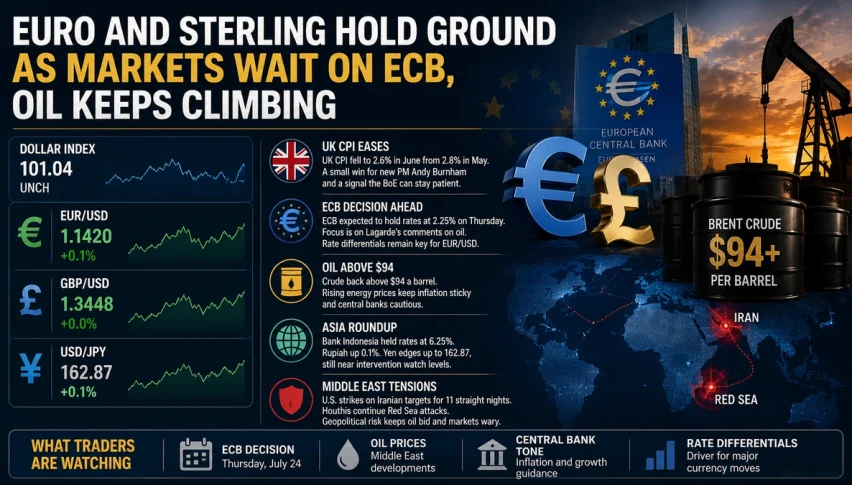

The European Central Bank cut deposit rates further in September to -0.50% and they restarted the QE programme this month. These actions were overdue since the economy of the Eurozone has weakened tremendously this year. The ECB let traders know that they are done with monetary easing now.

But that’s not so certain and comments from ECB members show that they would be more comfortable with extensive monetary and fiscal policy easing than the opposite. Below are some of their comments:

Comments by ECB chief economist, Philip Lane

- Euro exchange rate is not a target of monetary policy

- Loosening policy has had positive trade balance effect

- It is plausible that impact of rate cuts on the euro has intensified over time

- Especially since negative rates were introduced in 2014

- QE measures have had large and persistent effects on the euro

Comments by ECB vice president, Luis de Guindos

- Countries with fiscal space should do more

- Fiscal policy in the context of very interest low rates is much more powerful for the business cycle

- Data not pointing towards recession but growth will be below potential

- If euro area growth is below potential, need to pay close attention

- Should not be complacent about an inflationary shock in the euro area

- Monetary policy cannot address all problems in the world economy

- ECB still has ammunition but side effects of policy are becoming more evident

The Euro exchange rate is not a target for the ECB, Lane says, so it means that the ECB wouldn’t mind if the Euro keeps weakening. They also keep pressuring Eurozone governments to increase fiscal spending, which is aimed at Germany. This sort of attitude should keep the Euro bearish in the long term.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts