Stock Markets Stall, As Global Services and Manufacturing Weakens Further

Eurozone, UK and US services and manufacturing fell deeper in contraction in September, indicating that the global recession is on the way

Stock markets have been showing some bullish signs this month despite still being bearish on the larger charts. Comments from SF FED Mary Daly who is a mouthpiece for Jerome Powell, that the FED will have to slow down, improved the sentiment, which sent risk assets higher.

Today stock markets were bullish during the European session, but they have retreated in the US session after the US services and manufacturing reports, which were soft. Services activity fell further into negative territory while manufacturing also fell in contraction. Although, this could turn out to be a positive event for risk assets, since it puts pressure on the FED to stop raising rates.

German Index Dax H4 Chart – Turning Bullish This Month?

Can DAX overcome and hold above the 200 SMA?

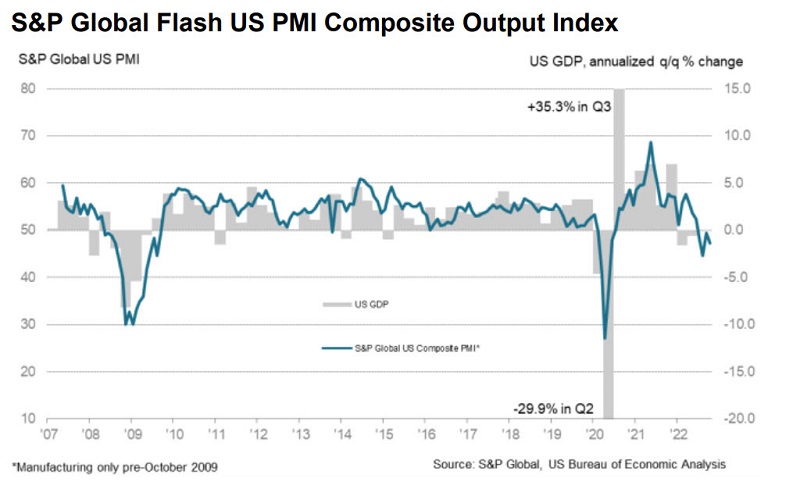

S&P Global US September Services Report

- September flash services PMI 46.6 points vs 49.2 expected

- Second-fastest fall in almost two-and-a-half years

- Firms linked the decrease to weak client demand and the impact of inflation and higher interest rates

- Services input price inflation rose

- August services were 49.3 points

- Manufacturing 49.9 points vs 51.0 expected

- Prior manufacturing 52.0points

- Manufacturing new orders fell back into contraction

- Decrease in client demand was the sharpest since May 2020

- “Alongside domestic inflationary pressures, total new orders were dampened by challenging economic conditions in key export destinations and dollar strength, as new export orders fell steeply.”

- Composite 47.3 points vs 49.3 expected

- Prior composite was 49.5 points

- Firms’ optimism about the outlook meanwhile deteriorated markedly in October. The resulting degree of confidence was among the lowest in the survey history and the weakest for just over two years.

This is a poor reading and will be a test on whether bad news is good news, as it puts pressure on the FEDto stop rate hikes. Commenting on the flash PMI data, Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

“The US economic downturn gathered significant momentum in October, while confidence in the outlook also deteriorated sharply. The decline was led by a downward lurch in services activity, fuelled by the rising cost of living and tightening financial conditions. While output in manufacturing remains more resilient for now, October saw a steep drop in demand for goods, meaning current output is only being maintained by firms eating into backlogs of previously placed orders. Clearly, this is an unsustainable absence of a revival in demand, and it’s no surprise to see firms cutting back sharply on their input buying to prepare for lower output in coming months.

“One upside of this drop in input buying has been a further alleviation of supply constraints, which alongside the stronger dollar have helped cool price pressures in the manufacturing sector.

“Although price pressures picked up slightly in the service sector due to high food, energy, and staff costs, as well as rising borrowing costs, increased competitive forces meant average prices charged for services grew at only a fractionally faster rate. Combined with the easing of price pressures in the goods-producing sector, this adds to evidence that consumer price inflation should cool in the coming months.

“The surveys, therefore, present a picture of the economy at increased risk of contracting in the fourth quarter at the same time that inflationary pressures remain stubbornly high. However, there are clearly signs that weakening demand is helping to moderate the overall rate of inflation, which should continue to fall in the coming months, especially if interest rates continue to rise.”

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account