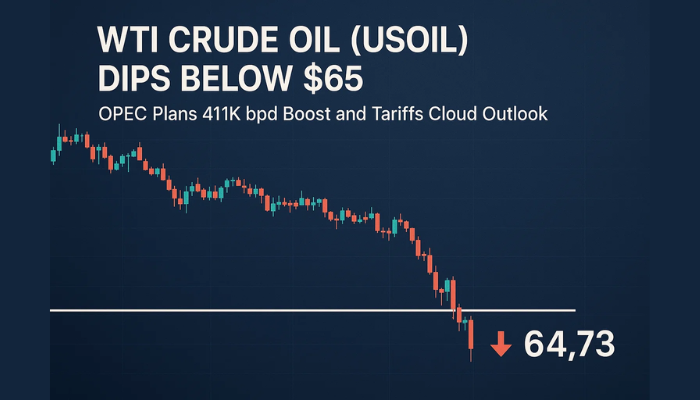

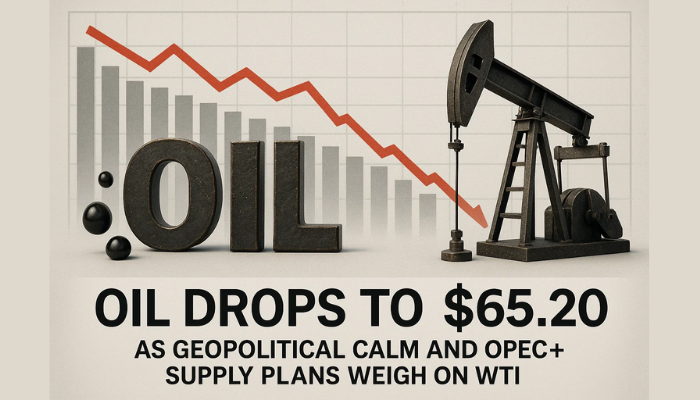

Crude Oil Heads for $70 Fast, Ahead of the EIA Crude Inventories

Crude Oil has been losing $4 in each of the last two days and yesterday's API private inventories showed a bigger-than-expected buildup

Crude Oil was quite bullish since the middle of October after the support zone around $70 held, showing confidence while the rest of the market was showing uncertainty after the last round of rate hikes from central banks. But, on Tuesday we saw a strong reversal lower which continued yesterday, and Oil lost around $8 as it heads down for $70 again.

Thin liquidity and cash flows exacerbated the sharp swings in the market while crude Oil only headed south. The unclear situation in China which is the main Oil importer in the world is overweighting the bid to boost its economy. The sanctions against Russia dragged its Oil flows to 2022 lows late last month, it hasn’t helped Oil much, so the has been little relief to Oil buyers this week.

WTI Crude Oil Daily Chart – The 50 SMA Held As Resistance

The downtrend remains intact

So, yesterday US WTI crude lost around $4/barrel, posting the biggest decline of the first two trading days of the year for more than 30 years. Traders seem worried about Oil demand as the global economy slows down and the COVID situation continues in China.

The crude Oil inventories from the API privately surveyed Oil stock data showed a buildup that was bigger than expected, ahead of the EIA official government data later today out of the US. The headline via Twitter:

Adding in further info:

Expectations were as shown below:

Headline crude +1.2 mn barrels

Distillates -0.4 mn bbls

Gasoline -0.5 mn

US WTI Crude Oil Live Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account