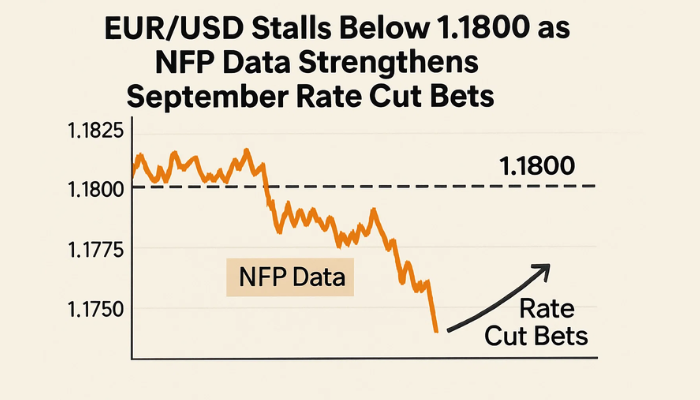

Risk Sentiment Dampens, USD Up As Labour Market Remains Robust

Risk currencies took a dive yesterday after the strong ADP employment report, followed by a bounce in ISM services, which gave the USD a boo

At the beginning of the year, recession predictions were widespread and unanimous, with only a minority suggesting an alternative outcome. However, what has transpired is quite the opposite, as the economy has heated up significantly. Jobs growth has consistently outperformed expectations for 14 consecutive months, and if yesterday’s ADP jobs report is any indication, it is likely to extend that streak to 15 months.

The Non-Farm Employment (NFP) report will be released soon, although judging by yesterday’s price action following the ADP report, chances are that we will see further bullish action on the USD, and softer risk sentiment, since this means more hikes by the FED.

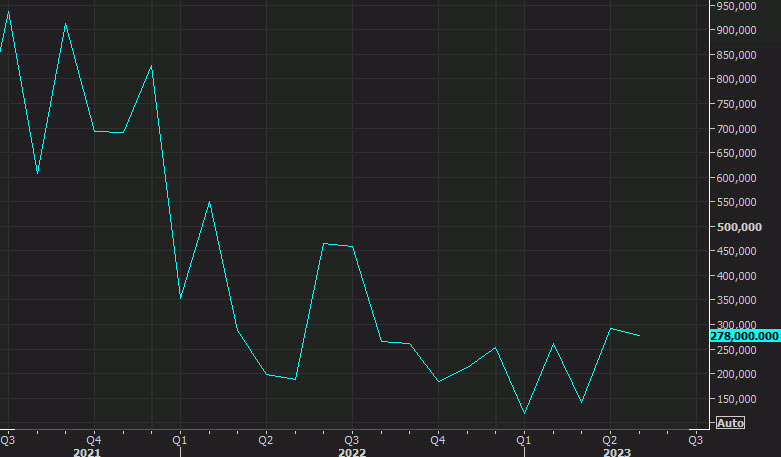

June 2023 Employment Numbers from ADP

- June ADP employment +497K vs +228K expected

- Largest increase since Feb 2022

- May ADp employment was 278K

Details:

- Small (less than 50 employees) +299K vs +116K prior

- Medium firms (500 – 499) +183K vs +112K prior

- Large (greater than 499 employees) -8K vs +106K prior

- Job stayers 6.4% vs 6.5%

- Job changers 11.2% vs 12.1%

The US 2-year yield topped 5% for the first time since early March on the data and the US dollar is stronger across the board. The high for the year is 5.08%.

“Consumer-facing service industries had a strong June, aligning to push job creation higher than expected,” said Nela Richardson, chief economist, ADP. “But wage growth continues to ebb in these same industries, and hiring likely is cresting after a late-cycle surge.”

In the breakdown, the leisure/hospitality industry added 232K of the jobs with education/health services adding another 74K. Construction was also strong at +97K.

June US Services Survey from the Institute for Supply Management

- June ISM services 53.9 points vs 51.0 expected

- May ISM services were 50.3 points

Details:

- Employment index 53.1 points versus 49.2 prior

- New orders index 55.5 points versus 52.9 expected

- Prices paid index 54.1 points versus 56.2 prior

- New export orders 61.5 points versus 59.0 last month

- Imports 54.6 points versus 50.0 last month

- Backlog of orders 43.9 points versus 40.9 last month

- Inventories 55.9 points versus 58.3 last month

- Supplier deliveries 47.6 points versus 47.7 last month

- Inventory sentiment 54.0 points versus 61.0 last month

You could see this one coming after the S&P Global survey and ADP. That may have limited the market reaction, though we’re still at highs in the US dollar and lows in equities.

Comments in the report:

- “Stabilizing inflation rates are helping our overall situation. (High inflation has) done much to disrupt our pricing for services and rent over the past two years.” [Agriculture, Forestry, Fishing & Hunting]

- “We have been very busy in June, with great content coming out of the studios and the summer guest traffic.” [Arts, Entertainment & Recreation]

- “Monitoring China’s anti-espionage legislation going into effect on July 1 that may have an impact on normal supply chain business operations like market research, recruitment, trade secret leakage, employing former government officials and data sharing between Chinese and foreign companies in joint domestic or cross-border projects, including transfer of technology or information sharing.” [Construction]

- “General business conditions are still active and steady. We’re ramping up for a busy third quarter with some expansion and preparations for early 2024 capital projects.” [Finance & Insurance]

- “Strong procedural volumes are driving above-budget revenue performance, but profitability continues to suffer due to higher expenses. Inflationary pressures, staffing challenges, limited capacity and insufficient payer rates continue to financially challenge the health system. Supply chains continue to moderately improve.” [Health Care & Social Assistance]

- “Supply chain lead times have stabilized and prices are holding or, in some cases, dropping slightly. It’s been a long time coming.” [Information]

- “Our company is maintaining an overall cautious approach, with inflation and the economy as main concerns. With oil prices stabilizing at around (US) $70 a barrel, we hope they start refilling the Strategic Petroleum Reserve to replace the oil withdrawn via emergency-use release during the pandemic.” [Management of Companies & Support Services]

- “Increased demand for new transformation programs, with prices holding and an increase in clients’ capital budget allocations.” [Professional, Scientific & Technical Services]

- “Business remains higher than a year ago but is falling short of forecasts and projections.” [Real Estate, Rental & Leasing]

- “Overall business conditions are good, but growth is at a slow pace.” [Retail Trade]

- “Labor rates continue to be a challenge even with more people looking to return to work. Inflation is most likely a cause for this. Some incremental lower pricing on food.” [Transportation & Warehousing]

- “High operational expenses continue to put pressure on our business and limit hiring. Service levels from suppliers continue to improve. Trucking metrics and sales also improved.” [Wholesale Trade]

EUR/USD Live Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account