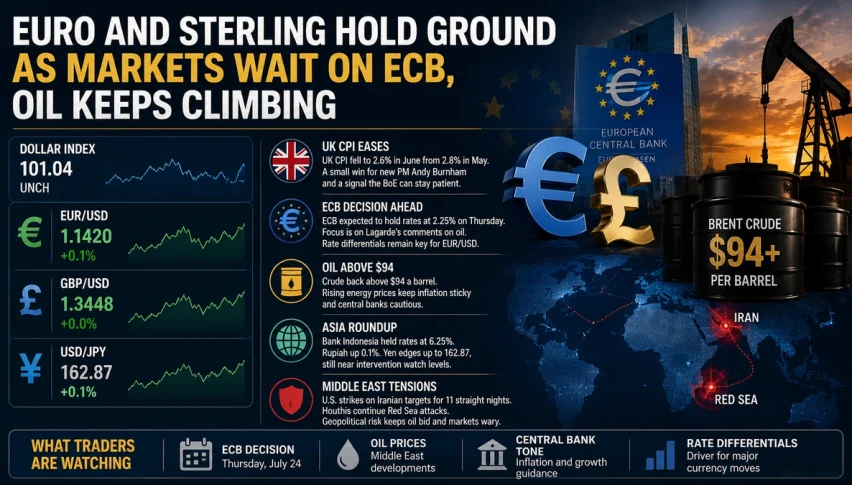

Don’t Forget the US Jobs Reports This Week!

This week we have two more major central banks on the agenda which will attract all attention until Thursday, after three meetings last week

This week we have two more major central banks on the agenda which will attract all attention until Thursday, after three meetings last week, which kept markets volatile last week and will likely continue the same behavior this week. But, this week we have several very important employment reports from the US, which might turn everything around, as employment is still very important at this point in the economic recovery, with the FED looking closely at the numbers.

The main report is obviously the NFP (Non-Farm Payrolls) on Friday, however, before the January NFP numbers, we have the December JOLTS Job Openings and Labor Turnover Survey tomorrow. The labor market was showing some weakness in early Autumn, as the first reading for October showed a decline to 8.73M, which was revised higher to 8.79 last month though. 8.85M. But, in November the JOLTS data is expected to show job vacancies to resume the declining trend as they should fall marginally from the 8.79 million to 8.73M in December.

Overall, the labour sector gradually improved during last year, but let’s see if the trend will continue this week. On Wednesday, we will get to see the Q4 employment cost data, which will show if the slowing in pay growth is maintained in the last quarter of 2023. Expectations are for a modest slowdown from the 1.1% rate that we saw in the previous quarter. The headline ADP Non-Farm Employment Change is expected to slow down to 143K, but that comes after a strong jump to 164K in the previous week.

Will the NFP Numbers Steal the Spotlight from the FED?

On Friday comes the main jobs report, with the consensus for the headline NFP forecast 162k jobs to be added to the US economy this month, although expectations from different surveys range from 135K, up to 280k. Average hourly earnings are expected to rise by 0.3% month on month, which is a tick lower than the 0.4% increase observed in December, while average workweek hours are expected to tick higher to 34.4 hours/week from 34.3 hours in December. The unemployment rate is expected to remain constant at 3.7% which is a great level.

Analysts also point out that the January jobs data will include final benchmark revisions for 2023, with some expecting a negative revision, but this tells us little about recent trends. The FED will likely repeat the comments from December, that they would like to ease the policy this year, but the pace of the rate cuts will depend on the economic data, such as this week’s employment and inflation figures.

Gold XAU Live Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts