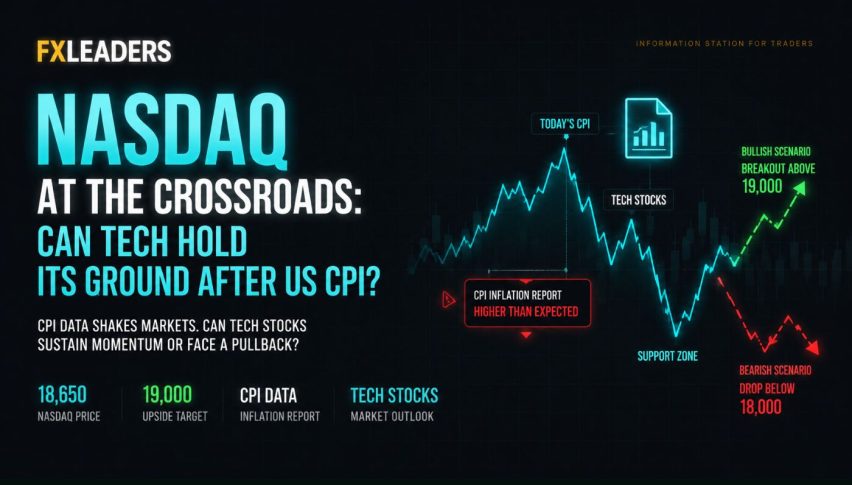

USD Dives As US Inflation CPI Heads to Normal Levels

The downward surprise in the US CPI inflation May inflation has led to a significant decline in the USD, sending all other assets higher.

The downward surprise in the US CPI inflation May inflation has led to a significant decline in the USD, sending all other assets higher. USD/JPY has lost more than 150 pips, reflecting broader US dollar selling across the board. This downward movement in the currency pair is part of a larger trend, with market sentiment shifting towards expectations of monetary easing by the Federal Reserve.

The May inflation estimate came in below expectations, and the unrounded numbers are even weaker than the rounded ones that appear in the headlines, which suggests that inflationary pressures may be moderating, prompting market participants to adjust their expectations for Fed policy.

The Fed funds market now anticipates 50 basis points of easing by year-end, with the first rate cut likely in September. This reflects a shift in sentiment towards a more dovish stance from the Federal Reserve in response to softer inflation data, which was influenced by various factors, including a stabilization in vehicle insurance prices and a decline in core services excluding shelter.

However, housing remains a source of high inflation still, with prices rising month-on-month. The CPI data may influence the decision-making of FOMC officials, particularly in their projections for interest rate changes as reflected in the dot plot. Some officials may signal a preference for two rate cuts this year, considering the softer inflation outlook.

US May 2024 Consumer Price Index (CPI) Data:

Headline CPI Inflation Measures:

- May CPI YoY: 3.3% (vs expected 3.4%)

- Prior YoY: 3.4%

- May CPI MoM: +0.2% (vs expected +0.3%)

- Prior MoM: +0.3%

- Prior Unrounded MoM: +0.313%

Core CPI Inflation Measures:

- Core CPI MoM: +0.2% (vs expected +0.3%)

- Prior MoM: +0.3%

- Unrounded Core MoM: +0.163% (prior +0.290%)

- Core CPI YoY: 3.4% (vs expected 3.6%)

- Prior YoY: 3.6%

- Supercore MoM: -0.045% (vs prior +0.422%)

- Supercore YoY: +4.8%

- Shelter MoM: +0.4% (same as prior month)

- Shelter YoY: +5.4% (vs prior +5.5%)

Additional Components:

- Real Weekly Earnings: +0.4% (vs prior -0.4%)

- Food MoM: +0.1% (vs prior +0.0%)

- Food YoY: +2.1% (vs prior +2.2%)

- Energy MoM: -0.2% (vs prior +1.1%)

- Energy YoY: +3.7% (vs prior +2.6%)

- Rents MoM: +0.4% (same as prior)

- Owner’s Equivalent Rent MoM: +0.4% (same as prior)

- Motor Vehicle Insurance MoM: -0.1% (still up 20.9% YoY)

- Full report (pdf)

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts