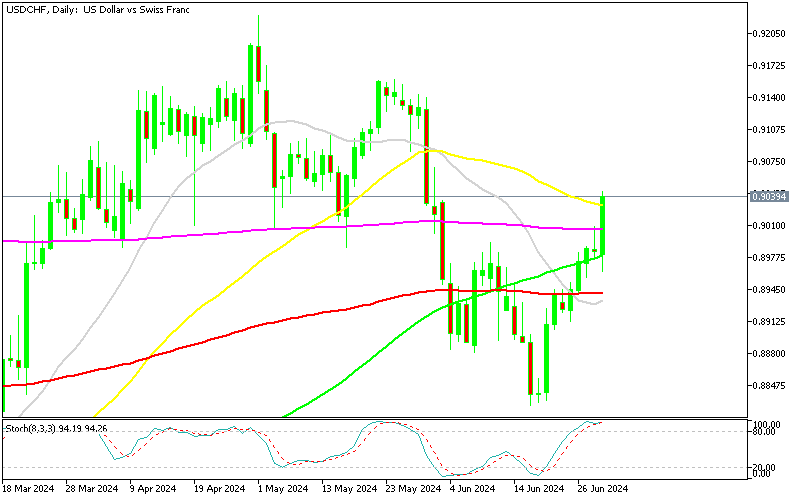

USDCHF Above 0.90 Despite Softer ISM Manufacturing

The USD has been showing some resilience lately, with CHF to USD rate being bullish in the last two weeks and climbing above 0.90.

The USD has been showing some resilience lately, with CHF to USD rate being bullish in the last two weeks and climbing above 0.90. US dollar initially dropped following a disappointing ISM manufacturing index report but swiftly bounced back. The bond market is fueling this recovery, with 10-year Treasury yields climbing 12 basis points on the day and over 20 basis points from Friday’s post-PCE lows.

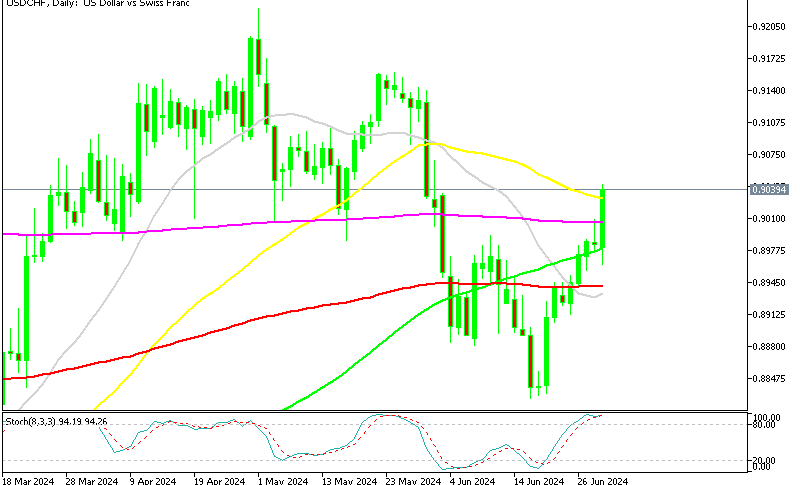

USD/CHF Chat Daily – Pushing Above the 50 SMA

USD/CHF has hit a new one-month high, gaining 40 pips to break above 0.90 for the first time since late May. The 50 SMA (yellow) has been broken now, which means that the bearish trend is over. Meanwhile, the recent advances in commodity currencies are fading, partly due to a stock market that hasn’t started as robustly as anticipated.

US ISM Manufacturing for June 2024

- US May ISM manufacturing index: 48.5 vs 49.1 expected, previous month 48.7.

- Prices paid: 52.1 vs 57.0 prior.

- Employment: 49.3 vs 51.1 last month.

- New orders: 49.3 vs 45.4 last month.

- Production: 48.5 vs 50.2 last month.

- Supplier deliveries: 49.8 vs 48.9 last month.

- Inventories: 45.4 vs 47.9 last month.

- Backlog of orders: 41.7 vs 42.4 last month.

- New export orders: 48.8 vs 50.6 last month.

- Imports: 48.5 vs 51.1 last month.

Comments in the report:

- High customer order volumes [Chemical Products].

- Customers cutting orders with short notice affecting suppliers [Transportation Equipment].

- Instability in consumer demand and inventories at retail and food service [Food, Beverage & Tobacco Products].

- Sufficient inventory from the previous month to meet current commitments [Computer & Electronic Products].

- Customers increasing orders to build buffer stocks for future shortages [Electrical Equipment, Appliances & Components].

- Weak demand in main divisions leading to inventory reduction [Fabricated Metal Products].

- Decreasing sales backlog resulting in workforce furloughs [Machinery].

- Lower production levels due to reduced product demand [Miscellaneous Manufacturing].

- Elevated financing costs dampening residential investment demand, leading to reduced inventory of production components [Wood Products].

- Slight increase in orders due to seasonal restocking [Plastics & Rubber Products].

USD/CHF Live Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts