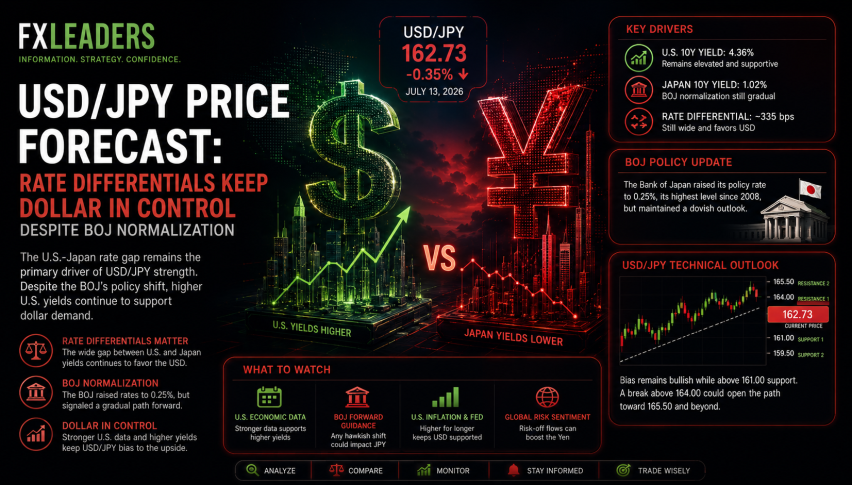

High Volatility in Yen to USD Rate, FED Speakers Balanced

The Yen to USD rate is showing high volatility, jumping 2 cents higher and giving it back, as FED speakers leave 25-50 bps cut options open.

The Yen to USD rate is showing high volatility, jumping 2 cents higher and giving it back, falling below 143 as FED members leave both options of a 25 bps and a 50 bps rate cut open. The market examines the August non-farm payrolls report and concluded that the data is not weak enough to warrant a 0.50% rate cut. This view is reinforced by balanced remarks from Fed officials Williams and Waller. Initially, the lower-than-expected headline NFP number and downward revisions for July pushed the odds of a 50 basis point jumping to 57%, leading to a decline in the US dollar initially.

However, the odds of a 50 bps cut have declined to 35% again, and the USD is back up, partly due to Fed members neutral stance, as they refrained from giving clear signals. The USD/JPY pair has experienced significant volatility, rising by 200 pips from its low to surpass 144, before reversing course and falling back below 142. Risk-sensitive currencies, including commodity-linked dollars, are also down, while the Euro is showing resilience against the USD.

USD/JPY Chart – The Downtrend Continues

Comments from FED Policy Member Williams

- Part of the rise in unemployment is due to the labor market cooling from its previously overheated state.

- The labor market is now more balanced and unlikely to generate future inflationary pressures.

- Signals readiness to begin cutting interest rates.

- Not quite ready to say how big first rate cut should be

- Monetary policy could shift to a more neutral stance, depending on future data.

- Williams hints at rate cuts: “Time to reduce policy restrictiveness.”

- Inflation is moving steadily toward the 2% target, increasing confidence in current policy success.

- Labor market is now “roughly in balance” and no longer a major driver of inflation.

- GDP growth forecast: 2-2.5% for the current year.

- Unemployment rate expected to hit 4.25% by year-end (up from 4.22% in today’s report).

- PCE inflation projected to ease to 2.25% this year, approaching 2% next year.

- Monetary policy may shift to a neutral stance over time, based on upcoming economic data.

- The Fed remains cautious of risks: labor market weakness, global economic slowdown, and unexpected inflation trends.

- Future policy decisions will remain data-driven and focus on maintaining the dual mandate.

He added that some of the increase in unemployment indicates that the labor market is cooling down from its previously overheated state. With the job market now more balanced, it is less likely to contribute to inflationary pressures going forward. The Federal Reserve is ready to begin lowering interest rates and could move towards a more neutral monetary policy stance, depending on economic data. Williams has signaled a willingness to ease rates, noting that it is “appropriate to reduce restrictiveness.” Inflation is gradually moving towards the Fed’s 2% target, boosting confidence in the effectiveness of current policies. This gives room for the Fed to adjust to a more neutral policy stance, depending on future data. However, future policy decisions will continue to be data-driven, focusing on stable prices and maximum employment.

FED Member Christopher Waller Remarks

- It’s time to start reducing the policy rate to maintain economic momentum at the next Fed meeting.

- Recent data shows labor market softening but not deteriorating; this assessment will be key in the upcoming decision.

- Multiple rate cuts are likely appropriate.

- Deciding the pace of rate cuts will be challenging.

- Waller is open to adjusting the size and timing of cuts, depending on incoming data.

- He supports front-loading rate cuts if necessary.

- If the labor market shows significant decline, the Fed can respond swiftly and aggressively.

- Waller is open to consecutive cuts or larger cuts if data warrants it.

- Does not believe the economy is in or heading toward a recession in the near term.

- Ready to act quickly to support the economy as needed.

- There’s room to cut rates while still keeping policy restrictive enough to manage inflation back to 2%.

USD/JPY Live Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts