Forex Signals Brief September 11: US CPI Threatens the USD!

Today the US CPI inflation is more likely to send the USD down on a soft reading, than sending it up on a strong reading.

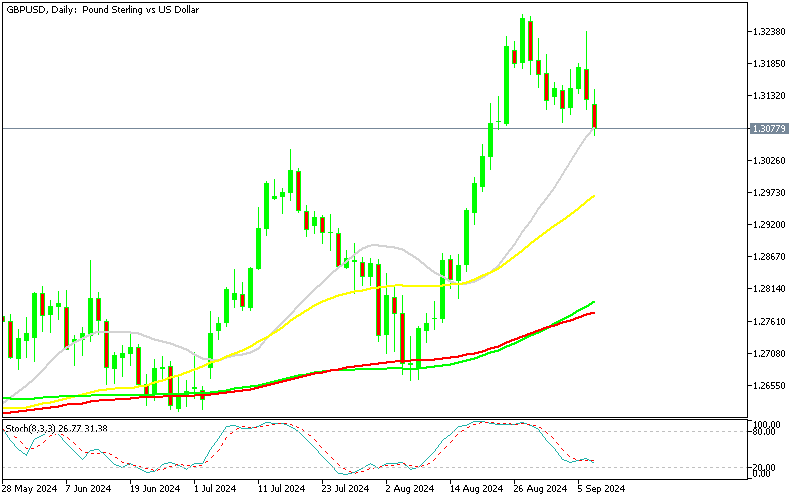

Yesterday started with the Chinese trade balance, which showed a slowdown in imports, setting the risk tone to negative for financial markets, with European and Asian stock markets ending up lower. The UK employment report for July leaned on the positive side, as the unemployment rate ticked lower to 4.1% while the number of new jobs increased more than expected, but GBP/USD ended the day lower the negative sentiment kept risk currencies down, and the USD supported.

Bank of Canada Governor Macklem’s remarks suggested the possibility of a 50 basis point rate cut at the October meeting if economic data, particularly on growth, continues to disappoint. This dovish stance has bolstered the USD/CAD, especially as oil prices continue to fall, hurting the value of the Canadian dollar. Oil, which has been bearish for six of the last seven days, has fallen to its lowest level since 2021, reflecting broader concerns about the global economy.

As oil prices decline, safe-haven assets like gold, the Japanese yen (JPY), and the Swiss franc (CHF) have gained strength. Falling bond yields have further supported these safe-havens. The USD/JPY pair dropped by about 1 cent, wiping out its weekly gain and ending the day just 50 pips above the August spike low. This signals that yen trades are teetering on the edge of a potential breakdown, which could serve as a warning for broader financial markets.

Today’s Market Expectations

Today starts with a batch of economic data from the UK, most notably the monthly GDP report for July. In June the UK economy fell flat, stagnating at 0.0%, but in July the economy is expected to have expanded by 0.2%, which would be positive for the GBP. However, the Manufacturing Production, Industrial Production and Construction Output are all expected to slow down.

The key event this week is the U.S. inflation report, with expectations that the headline CPI year-over-year (Y/Y) will come in at 2.6%, down from 2.9% previously. The month-over-month (M/M) measure is projected to remain steady at 0.2%. Similarly, Core CPI Y/Y is expected to hold at 3.2%, unchanged from the prior reading. Although inflation remains a key economic indicator, the labor market is currently the Fed’s main focus. The Fed has even stated that any positive inflation surprises won’t significantly change their outlook. This suggests that inflation data may carry less weight in immediate policy decisions. However, a weak inflation report could boost expectations of a 50 basis point rate cut, potentially raising those odds to around 50%, which would likely put pressure on the U.S. dollar. On the other hand, a strong inflation report is more likely to be overlooked by the market given the Fed’s current focus on employment.

Expectations for the US CPI:

- Headline CPI Y/Y expected at 2.6%, M/M steady at 0.2%.

- Core CPI Y/Y predicted to remain at 3.2%.

- The Fed is prioritizing the labor market, reducing the immediate importance of inflation data.

- A weak CPI report could increase expectations of a 50 bps rate cut, negatively affecting the USD.

Yesterday things complicated somewhat after we had a good start to the week yesterday, with markets reversing as risk sentiment improved by midday. However, the price action in Gold was quite straightforward, so we got a few good trades there. We opened eight forex signals in total, ending the day with four winning signals and three losing ones, while one remained open for today.

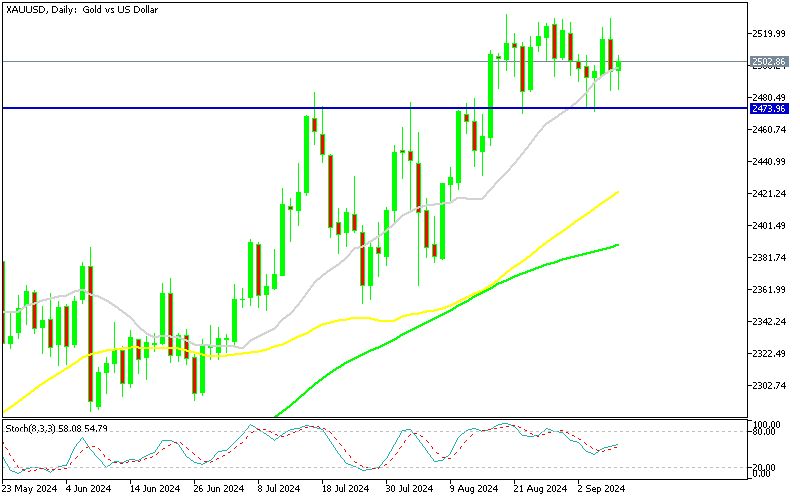

Gold Holds Above the 20 Daily SMA

In early August, gold reached a record high of $1,531.60, but despite multiple attempts, buyers were unable to push prices beyond this level. Last week, another effort was made, but it faltered after the release of the U.S. Non-Farm Payrolls (NFP) data. During the volatility surrounding the NFP, XAU/USD briefly spiked to $2,529, only to reverse and form a bearish engulfing candlestick pattern, indicating potential further declines. Although gold prices fell along with U.S. Treasury yields, the 20-day SMA remains a critical support level. Gold managed to bounce back and close above this average on Monday, and yesterday, it formed another bullish candlestick.

XAU/USD – Daily chart

USD/JPY Testing the Support Zone at 142 Again

in August, risk aversion in financial markets drove the USD/JPY pair below 142, though it quickly recovered. Yesterday, the pair returned to 142, with sellers regaining control, and it now seems likely that a further break below this level is imminent. While the Bank of Japan (BOJ) recently raised interest rates, BOJ officials have made it clear that there are no further rate hikes planned. Meanwhile, the Federal Reserve is preparing to initiate a cycle of policy easing, though the extent of the rate cuts will depend on key employment and inflation data—particularly the upcoming August CPI report. Diverging central bank policies are creating bearish signals for USD/JPY, and today’s CPI data could push the pair down toward 140.

GBP/USD – Daily Chart

Cryptocurrency Update

Bitcoin testing the Resistance at $57,000 Again

BTC/USD – Daily chart

Ethereum Bounces Off the Support

Since March, Ethereum has been in a steady downtrend, forming a series of lower highs, signaling the potential for further drops. After a sharp decline from $3,830 to under $3,000, Ethereum saw a brief rebound in June, surpassing its 50-day SMA. However, continued selling pressure pushed the price down to $2,200. Strong support at this level has helped the price recover, with Ethereum posting three consecutive bullish daily candlesticks, suggesting renewed buying interest.

ETH/USD – Daily chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts