Forex Signals Brief September 12: Locked for the ECB Rate Cut, US PPI

Today the ECB rate cut meeting highlights the day, but we also have the PPI producer inflation and Unemployment Claims from the US.

Yesterday started with the GDP report from the UK, which showed yet another flat month in stagnation at 0.0%, missing expectations of 0.2% for July. That was the third flat reading in the last four months, which shows that the UK economy is suffering. The other data releases such as Industrial and Manufacturing Production, were even worse, showing a decline, but that didn’t hurt the GBP much, especially not as much as the US CPI inflation report, which sent this pair almost 1 cent lower.

The US Core CPI for the month showed a 0.3% month-over-month increase, slightly exceeding the expected 0.2%. Year-on-year, the Core CPI remained steady at 3.2%, unchanged from the previous month and in line with expectations. On a brighter note, the headline CPI also met expectations, posting a 0.2% increase, though the unrounded figure was just below that mark. The year-on-year headline inflation figure dropped from 2.9% to 2.5%, indicating a gradual slowdown.

In light of these figures, real weekly earnings rose by 0.5%, reversing last month’s decline of -0.2%. Initially, markets reacted negatively to the data, with bond yields rising and equities declining, and the US dollar also strengthening. The Dow Jones industrial average experienced a dramatic turnaround, plunging as much as 700 points during the session but eventually closing 125 points higher. Similarly, the NASDAQ fell by 240 points, or 1.35%, at session lows but managed to recover somewhat by the end of the day.

Today’s Market Expectations

the main event of the day is he ECB meeting. The European Central Bank (ECB) is expected to lower its policy rate by 25 basis points to 3.50%, a move anticipated since July. Markets are pricing in continuous 25 basis point cuts at every meeting until mid-2025. While ECB President Christine Lagarde may not officially commit to another cut in October, she will likely keep the option open, contingent on upcoming economic data.

On the US front, the Jobless Claims report remains a key weekly indicator for the labor market’s health. Initial claims have remained within the 200K-260K range since 2022, signaling stable layoff levels. Continuing claims have been slowly increasing, although they recently showed signs of improvement. This suggests layoffs are low, but hiring has become more moderate. For this week, Initial Claims are forecast to rise slightly to 230K from 227K last week, while Continuing Claims are expected to increase to 1,850K from 1,838K. These metrics will provide further insight into the overall labor market trajectory. We also have the producer inflation PPI, with core PPI MoM expected to increase by 2 points.

Yesterday many traders got caught on the wrong foot by the increase in the US core CPI inflation, which led to a jump in the USD, while expectations leaned on the softer side, which would have dragged the USD lower. We also got caught during that move but nonetheless, we ended the day in breakeven with two winning and two losing signals.

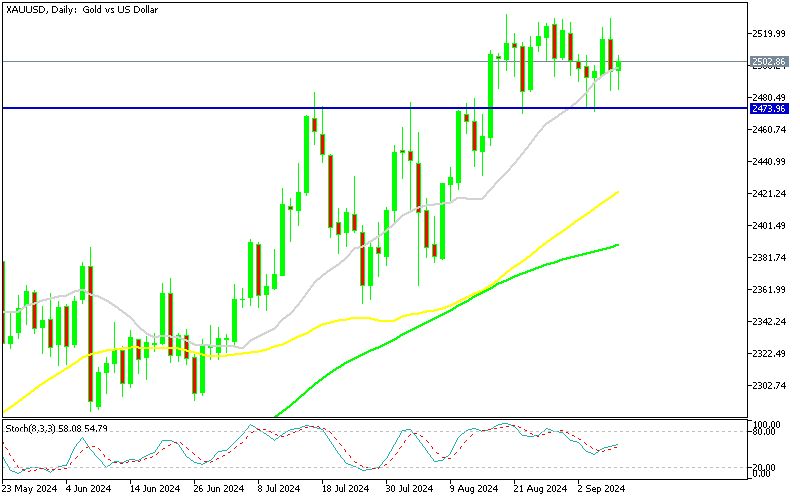

Gold Holds Above the 20 Daily SMA

In early August, gold reached a record high of $1,531.60, but despite multiple attempts, buyers were unable to push prices beyond this level. Last week, another effort was made, but it faltered after the release of the U.S. Non-Farm Payrolls (NFP) data. During the volatility surrounding the NFP, XAU/USD briefly spiked to $2,529, only to reverse and form a bearish engulfing candlestick pattern, indicating potential further declines. Although gold prices fell along with U.S. Treasury yields, the 20-day SMA remains a critical support level. Gold managed to bounce back and close above this average on Monday, and yesterday, it formed another bullish candlestick.

XAU/USD – Daily chart

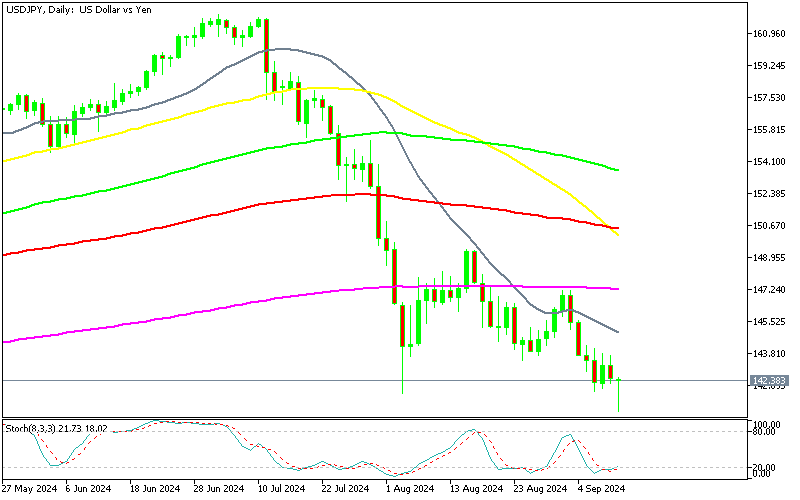

USD/JPY Testing the Support Zone at 142 Again

In the USD/JPY market, a 20-cent dip to 141.69 at the beginning of August was met with strong buying interest, driving the pair up by 7.5 cents and breaking above 149. However, the rise was short-lived, with sellers regaining control and forcing the pair back below 142, creating a support zone. A decisive break below this zone yesterday suggested further losses ahead, potentially pushing the price below the December 2023 lows around 140. With US Treasury yields continuing to decline, the Yen has had a positive week, gaining strength against the dollar.

USD/JPY – Daily Chart

Cryptocurrency Update

Bitcoin testing the Resistance at $57,000 Again

BTC/USD – Daily chart

Ethereum Bounces Off the Support

Ethereum, on the other hand, has been on a downward trajectory since March, consistently forming lower highs that point to further declines. After a steep drop from $3,830 to under $3,000, Ethereum saw a short-lived recovery in June, surpassing its 50-day SMA. However, the price slid to $2,200 due to ongoing selling pressure. Strong support at this level has triggered a rebound, with Ethereum showing three consecutive bullish daily candlesticks, suggesting renewed buying interest.

ETH/USD – Daily chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts