Forex Signals Brief December 12: The SNB and ECB Follow Up With More Rate Cuts

Yesterday the Bank of Canada delivered a 50 bps rate cut while today the SNB and ECB are expected to continue the monetary policy easing.

Yesterday the Bank of Canada delivered a 50 bps rate cut while today the Swiss National Bank and the ECB are expected to continue the monetary policy easing and lower interest rates by 25 bps each.

The USD strengthened against all major currencies except the CAD, where it declined by 0.14%. The US CPI inflation report showed a slight increase as expected, primarily due to rising housing costs, leading to a modest pullback in the greenback after its early-morning rally. Both headline and core CPI readings rose by 0.3%, in line with expectations.

Core CPI has now recorded a 0.3% monthly increase for four consecutive months, keeping the year-over-year core rate at 3.3%, well above the Fed’s 2% target. Headline CPI edged up from 2.6% in the prior month to 2.7%. Despite the uptick, markets largely interpret the data as supportive of further Fed policy easing. When the Fed meets next week, a 25 basis point rate cut is almost guaranteed.

Reflecting market optimism, the Nasdaq climbed 1.77% to a record high, while the Dow experienced a modest decline. Meanwhile, the USD weakened against the CAD even as the Bank of Canada (BoC) delivered a widely anticipated 50 basis point rate cut, lowering its policy rate to 3.25% from 3.75%. This marks a cumulative 175 basis point reduction since the BoC began easing rates in June 2024, including a 100 basis point decline over the last two meetings following three consecutive 25 basis point cuts.

Today’s Market Expectations

Today started with the employment report from Australia. The November labor market data highlights robust employment growth, driven primarily by a significant increase in full-time positions. The unemployment rate fell to a historically low 3.9%, well below expectations, underscoring a tight labor market. However, the marginal dip in the participation rate and the decline in part-time jobs may indicate nuanced dynamics, such as shifts from part-time to full-time roles. These results suggest ongoing resilience in Australia’s labor market and could influence monetary policy considerations.

The market is currently pricing a 57% probability of a 50 basis point rate cut by the Swiss National Bank (SNB). The persistent strength of the Swiss franc has not eased inflation, which remains significantly below the central bank’s forecasts. Thomas Jordan’s successor as SNB Chairman, Martin Schlegel, has displayed a firmer stance by signaling a willingness to reintroduce negative interest rates if necessary to curb demand for the safe-haven currency.

Meanwhile, the European Central Bank (ECB) is expected to reduce its policy rate by 25 basis points to 3.00%. This follows a series of weaker-than-expected economic data that have driven aggressive market pricing. However, most ECB officials opposed a larger 50 basis point cut in December. Looking ahead, the market projects five additional ECB rate cuts in 2025, though such expectations might prove excessive if economic conditions improve next year.

In the US, the Jobless Claims report remains a critical weekly release, offering a more immediate gauge of the labor market’s health. Initial claims continue to hover within the 200K–260K range established since 2022, while continuing claims remain near cycle highs. Last week, continuing claims fell slightly to 1,871K from 1,896K, though there is no consensus on this week’s figures. Initial claims are expected to come in at 221K, down from the previous 224K.

Yesterday the USD dollar continued the bullish momentum in the European session, however the CPI inflation data didn’t help much. Most forex pairs traded in a range, so the volatility wasn’t exceptional and we had four closed trading signals, ending the day with three winning fore signals and a losing trade in USD/CAD after the dip on the BOC rate cut.

Gold Continues the Consolidation Between MAs

This week, gold has seen significant gains, climbing approximately $100 from its lows to its peak, buoyed by the US CPI inflation rate, which added further momentum. Gold is currently testing the $2,721 level—the high from November 25—after reclaiming the $2,700 mark and forming three consecutive daily bullish candlesticks. It has risen $40 on the day, reaching $2,718.50, its highest point since November 21.

XAU/USD – H1 Chart

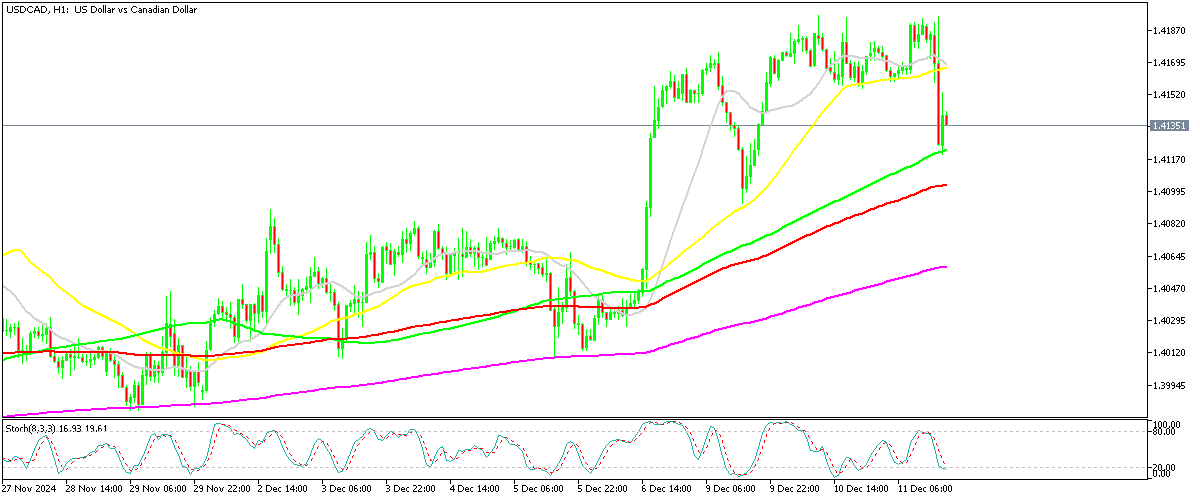

MAs Keep Supporting USD/CAD

In the USD/CAD pair, technical indicators like moving averages (MAs) continue to provide support, pushing the lows higher. On the fundamental side, a dovish Bank of Canada (BoC), which delivered its second consecutive 50 basis point rate cut, supports the pair. However, market dissatisfaction drove the pair about one cent lower earlier in the day. Despite this, USD/CAD rebounded in the US session, ending near the daily highs after the BoC’s monetary easing caused an initial dip to 1.41.

USD/CAD – H1 Chart

Cryptocurrency Update

Bitcoin Dips Below $95K but Bounces Again

BTC/USD – Daily chart

Ethereum Heads for $4,000 Again

Ethereum exhibited similar volatility, initially dropping below $3,000 before staging a strong recovery. It is now trading near $4,000, comfortably above $3,500 and its 50-day simple moving average (SMA). Ethereum is driving the broader cryptocurrency rally, supported by optimistic predictions of future price increases. This momentum reflects growing investor confidence and the overall resilience and strength of digital assets in the current market.

ETH/USD – Daily chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts