Bullish Reversal Unfolds in USD/JPY This Week

Last week USD/JPY formed a doji which signaled a bullish reversal after the retreat the previous week, this week this pair is 3 cents higher

Last week USD/JPY formed a doji candlestick which signaled a bullish reversal after the retreat the previous week, this week this pair is 3 cents higher as the USD regains some momentum.

The USD/JPY experienced a notable shift in late November after a strong two-month rally that added over 17 cents. In the final week of the month, the pair reversed course, losing 7 cents and falling below the critical 149 mark as market sentiment shifted, intensifying the selloff.

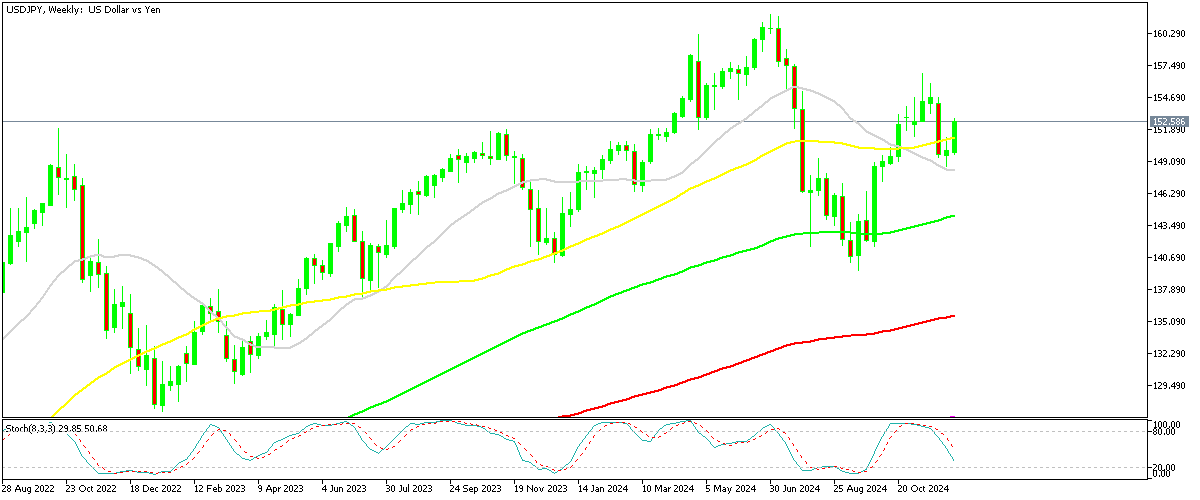

USD/JPY Chart Weekly – Bouncing Off the 20 SMA

However, the pair showed signs of stabilization last week, consolidating around the 150 level. This resulted in the formation of a doji candlestick on the weekly chart, signaling a potential positive turnaround. This week, the USD/JPY has regained its bullish momentum, climbing 3 cents as it found support at the 20 SMA on the weekly chart.

Drivers of Recent Movements in USD/JPY

- US Economic Data: Sticky US CPI and PPI inflation data supported the USD, even though they did not alter expectations for the Fed’s rate reduction timeline.

- BOJ Policy Outlook: The JPY faced broad declines, driven by market skepticism about any imminent changes in the Bank of Japan’s ultra-loose monetary policy.

Japan’s Economic Context

Japan’s economic growth remains fragile, with private spending and investment showing persistent weaknesses. The country’s revised GDP reading for Q3 came in at +0.7%, below the preliminary figure of +0.9%, underscoring the economy’s dependence on external stability and effective domestic policy measures. This vulnerability continues to weigh on the JPY, keeping it under pressure against stronger currencies like the USD. Early last night we had the Tankan Manufacturing and Non-Manufacturing index as well from Japan.

Tankan Manufacturing and Non-Manufacturing Index Highlights

Japan October Industrial Output

- +2.8% m/m (preliminary: +3.0%)

- +1.4% y/y (preliminary: -2.6%)

Bank of Japan Q4 2024 Tankan Report

- Big Manufacturers Index (December):

- +14 (highest since March 2022; Reuters poll: 12)

- Big Manufacturers Index (March forecast):

- Expected at +13 (Reuters poll: 11)

- Big Non-Manufacturers Index (December):

- +33 (Reuters poll: 32)

- Big Non-Manufacturers Index (March forecast):

- Expected at +28 (Reuters poll: 28)

Small Firms Indices

- Small Manufacturers Index (December):

- +1 (Reuters poll: -1)

- Small Manufacturers Index (March forecast):

- Expected at 0 (Reuters poll: -2)

- Small Non-Manufacturers Index (December):

- +16 (Reuters poll: 12)

- Small Non-Manufacturers Index (March forecast):

- Expected at +8 (Reuters poll: 10)

Currency Projections for FY2024/25

- All Firms:

- Dollar averaging 146.88 yen

- Euro averaging 159.03 yen

- Big Manufacturers:

- Dollar averaging 146.85 yen

Other Key Indicators

- Employment Index (December): -36

- Financial Condition Index (December): +12 (unchanged from September)

- Big Manufacturers’ Production Capacity Index (December): +3 (September: +2)

- Recurring Profit Forecasts (FY2024/25):

- Big manufacturers expect a -5.2% decline

- Capital Expenditure Forecasts (FY2024/25):

- Big firms: +11.3% (Reuters poll: +9.6%)

- Small firms: +4.0% (Reuters poll: +4.3%)

USD/JPY Live Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts