Forex Signals Brief Feb 3: EZ Inflation to Weigh on Euro After trade Tariffs

EUR/USD opened with a gap lower last night after weekend tariffs and it might continue lower toward parity if Eurozone inflation comes weak.

EUR/USD opened with a gap lower last night after weekend tariffs and it might continue lower toward parity if today’s Eurozone inflation report comes weak.

Last week opened quite volatile for stock markets, after the release of DeepSeek, which sent shock waves through the tech market, as it offered a much cheaper alternative to the competition. Nvidias stock dived 17%, but then stabilized around $220, however, the tariffs have opened stock markets with a bearish gap over the weekend.

The currency and cryptocurrency markets were pretty quiet, with traders thinking that tariffs might be postponed as a Reuters article suggested, which improved the sentiment for a brief moment. We had two rate cuts from the ECB and the Bank of Canada, which are another reason for the Euro and the CAD to be bearish, with USD/CAD opening to an all-time high this morning after the tariffs. Gold on the other hand, was quite bullish, breaking above $2,800 and putting a record high as well, however it reversed lower last night.

This Week’s Market Expectations

This week has also started in a volatile manner, after the weekend news, which have propelled USD/CAD above 1.47 and EUR/USD down to 1.02 lows. But, we will also have the Eurozone CPI inflation report today, which might send this pair even lower.

Key Economic Events for the Week

Monday – Manufacturing and Inflation Data Dominate

- Bank of Japan (BoJ) Summary of Opinions – Insights into the BoJ’s latest policy discussions, potentially signaling future monetary policy shifts.

- Australia Retail Sales – A crucial indicator of consumer spending, influencing RBA rate expectations.

- China Caixin Manufacturing PMI – A key gauge of private-sector factory activity, reflecting economic momentum.

- Switzerland Manufacturing PMI – Measures industrial health, impacting CHF sentiment.

- Eurozone Flash CPI – Inflation data that could shape ECB rate expectations and the euro’s direction.

- Canada Manufacturing PMI – A barometer of industrial activity, relevant for CAD movements.

- US ISM Manufacturing PMI – A major indicator of the health of the US factory sector, influencing Fed outlook.

Tuesday – Labor Market in Focus

- US Job Openings (JOLTS) – Provides insight into labor market strength and potential wage pressures.

- New Zealand Employment Report – Key data on job growth and wage trends, impacting NZD outlook.

Wednesday – Services Sector and Employment Trends

- Japan Average Cash Earnings – A measure of wage growth, important for inflation expectations.

- China Caixin Services PMI – Indicates private-sector service activity, crucial for overall economic sentiment.

- Eurozone Producer Price Index (PPI) – Tracks inflation at the wholesale level, influencing future CPI trends.

- US ADP Employment Report – A prelude to NFP, offering a snapshot of private-sector job growth.

- Canada Services PMI – Reflects business conditions in the services sector, affecting CAD sentiment.

- US ISM Services PMI – A key indicator of service sector performance, significant for Fed policy direction.

Thursday – Central Bank and Labor Market Data

- Switzerland Unemployment Rate – A labor market health check for CHF traders.

- Eurozone Retail Sales – A key gauge of consumer activity, influencing ECB rate policy.

- Bank of England (BoE) Policy Decision – Market-moving event with potential rate guidance from the BoE.

- US Jobless Claims – Weekly data on layoffs, providing a near-term labor market trend.

Friday – Major Employment Reports and Consumer Sentiment

- Canada Employment Report – A critical release for CAD traders, impacting BoC expectations.

- US Non-Farm Payrolls (NFP) – The most closely watched labor market indicator, shaping Fed rate projections.

- US University of Michigan Consumer Sentiment – Offers insight into consumer confidence, influencing USD direction.

Risk assets, including stock markets and commodity-linked currencies, saw strong buying momentum last week, leading to a volatile but ultimately weaker U.S. dollar. Across 26 forex trades, we secured 19 wins and 7 losses, maintaining a predominantly long stance on equities and gold.

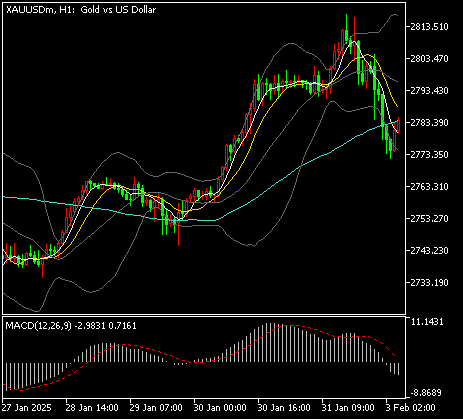

Gold Returns Below $2,800 Again

GOLD continues to exhibit strong bullish momentum, setting a new all-time high of $2,798.40 earlier today and holding above the previous peak of $2,790. Buyers remain firmly in control, signaling a likely move above $2,800 and potentially toward the $3,000 mark. The global economic and political climate remains supportive of safe-haven assets, reinforcing gold’s bullish outlook. The US GDP report provided a catalyst for XAU/USD, pushing it above the late October high near $2,790.

XAU/USD – H4 Chart

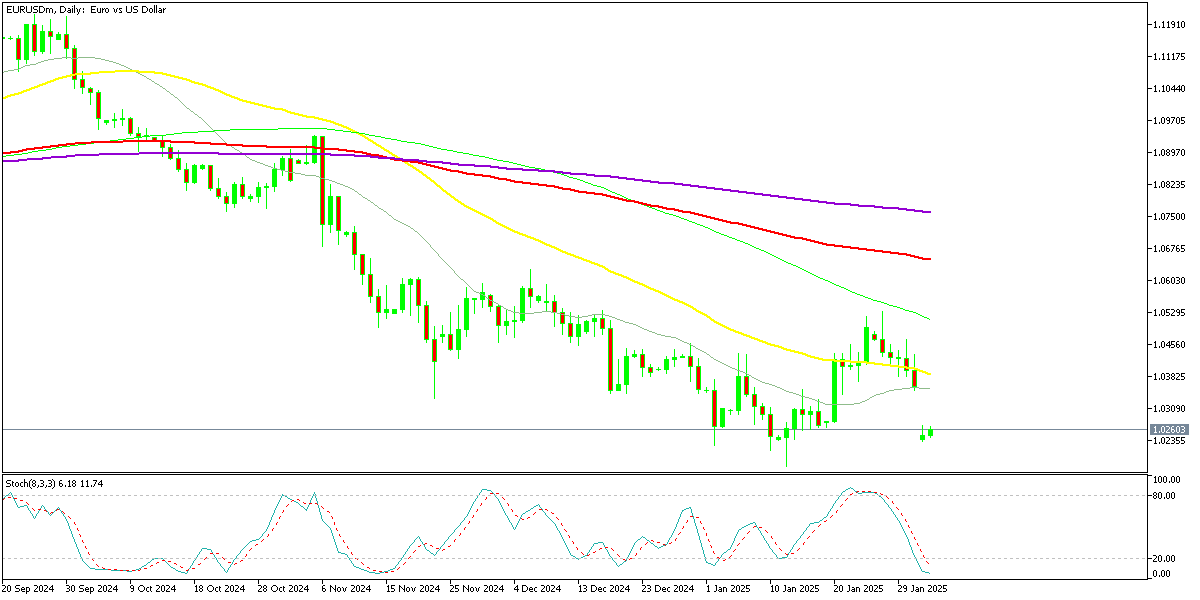

EUR/USD Heads to Parity Again

Meanwhile, the European Central Bank’s latest rate decision aligned with its December stance, delivering another dovish cut. This boosted the DAX to a new record and lifted broader European stock markets, though the euro saw only a temporary spike. EUR/USD briefly jumped 60 pips to 1.0460 but quickly retreated, later falling below 1.04 following tariff-related comments from Donald Trump.

EUR/USD – Daily Chart

Cryptocurrency Update

Bitcoin Returns Below $100K

BTC/USD – Daily chart

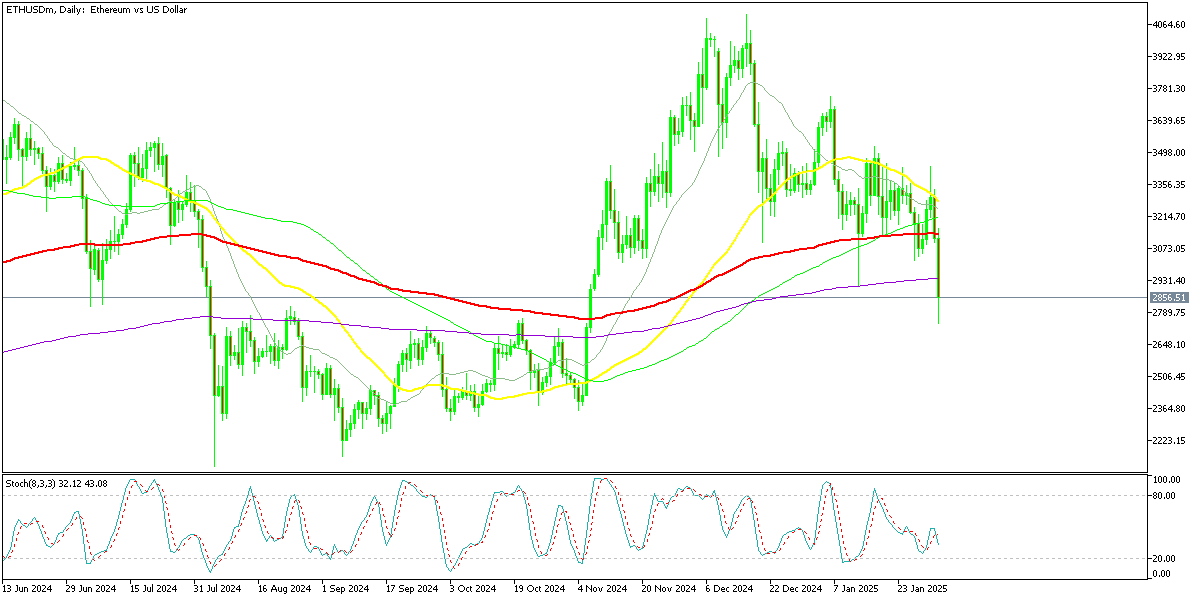

Ethereum Falls Below $3,000

ETHEREUM mirrored Bitcoin’s fluctuations, initially finding support near its 50-day SMA before slipping below $3,500 and later under $3,200. A broad crypto sell-off briefly pushed ETH below $3,000, but strong buying lifted it back above $3,500. Despite resistance at the 20-day SMA, broader crypto market strength has helped Ethereum stabilize, with the potential for further gains if buying pressure sustains.

ETH/USD – Daily Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts