btc-usd

Forex Signals Brief Sept 1: NFP Highlights Employment Week, Then Broadcom Earnings

This week we have a number of US employment reports, with NFP taking center stage, followed by APLD earnings report.

•

Last updated: Sunday, August 31, 2025

Quick overview

- This week features significant US employment reports, with the Non-Farm Payrolls (NFP) report expected to dominate market attention.

- Last week's market activity was lively despite a lack of major news, with U.S. GDP for Q2 revised higher to 3.3%, indicating economic resilience.

- Geopolitical tensions are influencing tech stocks, as Nvidia's shares fell following news of Alibaba's new AI chip development.

- Traders should prepare for heightened volatility this week as key inflation data and labor market reports are released across multiple regions.

Live BTC/USD Chart

BTC/USD

MARKETS TREND

This week we have a number of US employment reports, with NFP taking center stage, followed by APLD earnings report.

Last week was relatively quiet on the data and news side, but market activity remained lively. The key focus earlier in the week was the U.S. PCE report, which matched expectations across all measures. Additionally, Canadian GDP for Q2 showed a sharper contraction than anticipated, though investors largely brushed it off as outdated with Q3 nearly over and attention shifting toward Q4. Meanwhile, U.S. GDP for Q2 was revised higher to 3.3%, reinforcing signs of economic resilience.

Stock Market Moves

Momentum picked up once U.S. equities opened. Both the S&P 500 and Nasdaq sold off, weighed down by heavy losses in Nvidia. The trigger came from a Wall Street Journal report suggesting that Alibaba had developed a new AI chip, positioned to partly fill Nvidia’s gap in China.

Geopolitical and Tech Angle

China’s efforts to build domestic AI chip alternatives continue to intensify, particularly under the shadow of restrictions from the Trump administration. While Nvidia shares slipped on the news, Alibaba stock gained as investors welcomed its strategic push into advanced semiconductors.

Key Market Events This Week

This week’s calendar is packed with key inflation data, GDP updates, and labor market releases. The U.S. Jobs Report on Friday will dominate market attention, shaping expectations for Federal Reserve policy into the final quarter of 2025. Meanwhile, Eurozone inflation, Australian GDP, and Chinese PMI data will help gauge the health of global growth. Traders should expect heightened volatility, particularly toward mid-to-late week, as labor market and inflation themes converge across regions.

Week Ahead: Key Events and Data Releases

Markets face a busy calendar this week, with labor data, inflation prints, and central bank updates likely to steer sentiment across currencies, equities, and commodities.

Monday – Market Holiday, Manufacturing Focus

- US Labor Day: U.S. markets closed, likely lowering global trading volumes.

- China Caixin Manufacturing PMI (Final): A closer look at private-sector factory conditions; revisions could move sentiment.

- Eurozone, UK, US Manufacturing PMI (Final): Updates will help confirm the pace of industrial activity.

- New Zealand Terms of Trade (Q2): An important release for NZD traders, reflecting export-import price dynamics.

Tuesday – Inflation and Manufacturing in Focus

- Eurozone Flash HICP (Aug): The most important inflation print for the ECB this week.

- US ISM Manufacturing PMI (Aug): A leading U.S. manufacturing indicator, key for growth expectations and Fed policy outlook.

Wednesday – Central Bank Decision and Growth Data

- National Bank of Poland (NBP) Announcement: Potential policy signals as inflation and growth pressures diverge.

- Australia Real GDP (Q2): Will confirm whether the economy is slowing amid high interest rates.

- US ADP National Employment (Aug): A precursor to Friday’s NFP, providing an early labor market signal.

- China Caixin Services PMI (Final): Important gauge of post-pandemic recovery momentum in services.

- Eurozone, UK, US Services PMI (Final): Updated readings to confirm the state of services-driven growth.

- US Durable Goods Orders (Revised, Jul): May refine expectations for U.S. business investment trends.

Thursday – Services and Inflation Indicators

- Sweden CPIF (Aug): Riksbank’s key inflation measure, influencing Nordic monetary policy.

- US ISM Services PMI (Aug): Closely watched U.S. services data, critical for Fed’s growth-inflation balance.

Friday – Jobs Reports Take Center Stage

- UK Retail Sales (Aug): Indicator of consumer health amid persistent inflationary pressures.

- Eurozone GDP (Q2, Revised): May adjust growth outlook and ECB policy expectations.

- US Non-Farm Payrolls (Aug): The week’s highlight; job creation, wage growth, and unemployment rate will heavily influence Fed rate-cut bets.

- Canada Jobs Report (Aug): Important for CAD traders, assessing labor strength in the face of BoC policy shifts.

Earnings Reports This Week

- Salesforce, Inc. – Q2 2026 Earnings Announcement (After Market Close)

- American Eagle Outfitters, Inc. – Q2 2025 Earnings Announcement (After Market Close)

- Broadcom Inc. (AVGO) – Q3 2025 Earnings Announcement (After Market Close)

- lululemon athletica inc. – Q2 2025 Earnings Announcement (After Market Close)

Last week, markets were quite volatile once, with gold retreating and then bouncing to finish the week close to $4,000 but yesterday it retreated again. EUR/USD continued the upward move toward 1.17, while main indices closed higher. The moves weren’t too big though, and we opened 35 trading signals in total, finishing the week with 23 winning signals and 12 losing ones.

Gold Approaches $3,400

Gold also joined the rally: after briefly dipping below $3,268/oz following the Fed’s steady-rate decision, the metal climbed nearly $200 higher by week’s end. Strong safe-haven demand and stable labor data lifted prices above the 100-day SMA, reinforcing bullish momentum. Technicals continue to highlight the $3,450–$3,500/oz zone as the next key breakout area.

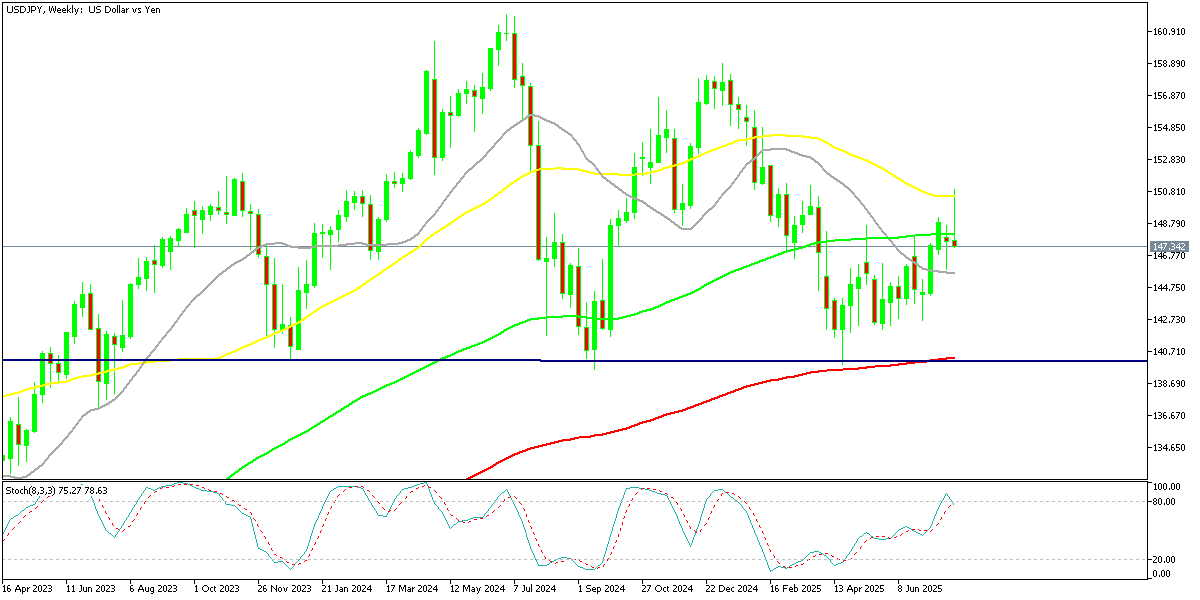

Yen Holds In A Tight Range

Foreign exchange markets saw sharp swings. Early in the week, U.S. yield differentials and Japanese capital outflows pushed the dollar above ¥150, but disappointing U.S. jobs data triggered profit-taking, causing the USD/JPY to slide by four yen from its peak. The move underscored persistent volatility as traders weighed Japan’s intervention risks against evolving Fed expectations.

USD/JPY – Weekly Chart

Cryptocurrency Update

Bitcoin Slips Below $110K Again

Cryptocurrencies remained highly active over the summer. Bitcoin (BTC) climbed to fresh highs of $123,000 and $124,000 in July and August, supported by institutional inflows and technical strength. However, remarks from Treasury Secretary Scott Bessent ruling out U.S. increases to BTC reserves triggered a steep pullback, sending the coin down to $113,000 before recovering above $116,000 last week, however sellers returned and sent BTC below $110,000, however we saw a rebound off the 20 weekly SMA (gray) yesterday.

BTC/USD – Weekly chart

Ethereum Heads to the $4,500 Level Again

Ethereum (ETH) has been similarly strong, surging toward $4,800, its highest since 2021 and near its all-time peak of $4,860. Despite a dip last week, ETH found support at the 20-day SMA, with retail enthusiasm and renewed institutional participation driving fresh upside momentum. However buying resumed and on Sunday ETH/USD printed another record at $4,941. However we saw a retreat to $,000 lows over the weekend, but yesterday buyers returned.

ETH/USD – Daily Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

ABOUT THE AUTHOR

See More

Skerdian Meta

Lead Analyst

Skerdian Meta Lead Analyst.

Skerdian is a professional Forex trader and a market analyst. He has been actively engaged in market analysis for the past 11 years. Before becoming our head analyst, Skerdian served as a trader and market analyst in Saxo Bank's local branch, Aksioner. Skerdian specialized in experimenting with developing models and hands-on trading. Skerdian has a masters degree in finance and investment.