btc-usd

Forex Signals Oct 28: Focus Turns to UNH UnitedHealth Earnings, Visa, UPS

A busy earnings day kicks off with UnitedHealth leading the spotlight, as major healthcare, finance, and logistics firms prepare to unveil t

•

Last updated: Tuesday, October 28, 2025

Quick overview

- UnitedHealth leads a busy earnings day as major firms prepare to report third-quarter results.

- The S&P 500 and Nasdaq Composite both saw significant gains, driven by positive trade negotiation news.

- Gold prices fell below the $4,000 mark for the first time since October 12, reflecting profit-taking amid improved risk appetite.

- Investors are closely watching upcoming earnings reports from key companies like UnitedHealth and Visa for insights into economic resilience.

Live BTC/USD Chart

BTC/USD

0.0000

MARKETS TREND

A busy earnings day kicks off with UnitedHealth leading the spotlight, as major healthcare, finance, and logistics firms prepare to unveil their third-quarter results.

Stocks Extend Rally, Nasdaq Leads the Charge

The S&P 500 advanced 1.2%, while the Nasdaq Composite surged 1.9%, marking its second consecutive breakout session. Investors responded enthusiastically to reports confirming progress on trade negotiations between Washington and Beijing, driving a broad-based risk-on sentiment across Wall Street.

Tech stocks once again led the advance, propelling the Nasdaq to fresh highs as traders embraced cyclical and growth names. The rally pushed major indices to finish at their intraday peaks, underscoring renewed market confidence.

Gold Breaks Below Key Support Level

In contrast to the equity surge, gold prices tumbled $120 to settle at $3,990 per ounce, slipping below the symbolic $4,000 mark for the first time since October 12. The move reflected heavy profit-taking following months of sustained gains, with prices retracing to the 38.2% Fibonacci level from the August rally.

The sharp reversal suggests investors are unwinding defensive positions as risk appetite improves and confidence grows in the broader economic outlook.

Oil and Bonds Hold Steady

WTI crude oil remained relatively flat, easing just 15 cents to $61.35, while U.S. 10-year Treasury yields dipped by 1 basis point to 3.98%. The mild retreat in yields indicates that investors are maintaining a cautious stance toward inflation and monetary policy, even as equity markets surge.

Currency Markets Stay Calm Despite Tariff Noise

The foreign exchange market saw limited movement, with most major currency pairs trading within narrow ranges. The Australian dollar found modest support on improved Chinese trade sentiment, while the Canadian dollar edged slightly higher despite new tariff warnings from President Trump.

Market analysts noted that the renewed threats failed to spark much reaction. “The tariff threat has lost its teeth,” said Adam Button, Chief Currency Analyst at investingLive, in comments to Reuters. “The Canadian dollar’s reaction shows the market has largely shrugged off the risk.”

Key Market Events to Watch This Week: Central Banks and Big Tech in Focus

Earnings Week Takes Center Stage

Looking ahead, attention now turns to a busy slate of corporate earnings reports, which could shape market direction in the days ahead. With limited economic data expected due to the ongoing U.S. government shutdown, investor focus will remain on company results and forward guidance for clues about the economy’s resilience.

Earnings Preview Highlights:

UnitedHealth Group (UNH) – Reports before market open (BMO)

- Analysts expect EPS of $2.81, reflecting continued pressure from higher medical costs and increased claims activity.

- Investors will be watching for updates on membership growth, healthcare utilization trends, and Medicare Advantage margins.

- Any signs of rising cost ratios could weigh on sentiment despite the company’s stable cash flow profile.

Visa Inc. (V) – Reports after market close (AMC)

- Expected EPS of $2.97, supported by resilient consumer spending and cross-border payment volumes.

- Focus will be on transaction growth in emerging markets and how macro headwinds impact discretionary spending.

Novartis AG (NVS) – Reports before market open (BMO)

- Forecast EPS of $2.31, with investors watching for updates on drug pipeline progress and cost efficiency measures.

- Currency fluctuations and pricing pressures remain key risks to margins.

HSBC Holdings (HSBC) – Reports before market open (BMO)

- No official EPS forecast, but analysts expect solid results driven by higher interest income.

- Focus will be on capital return plans and exposure to slowing Chinese credit markets.

United Parcel Service (UPS) – Reports before market open (BMO)

- Expected EPS of $1.31, with analysts noting potential headwinds from slower e-commerce growth.

- Freight volumes and operating margins will be closely watched, alongside management’s holiday season outlook.

Today’s lineup of corporate reports could set the tone for the rest of the week, with UnitedHealth’s performance likely to shape sentiment across the healthcare sector, while Visa’s results will provide a crucial snapshot of global consumer health. As markets hover near record highs, investors will be looking for earnings confirmation to sustain momentum amid rising rate and cost pressures.

Gold Breaks Below the $4,000 Support

Although demand for safe haven assets is still high, gold fell precipitously from record highs following the Fed’s most recent rate cut comments, as profit-taking was prompted by Powell’s cautious tone. Earlier this month, gold jumped above $4.3800 following the Federal Reserve’s announcement of a 25 basis point rate decrease. But the impetus soon waned, and prices dropped back to $4,004. The 20 daily SMA (gray) held as support last week, but it gave way yesterday as sellers pushed Gold below $4,000.

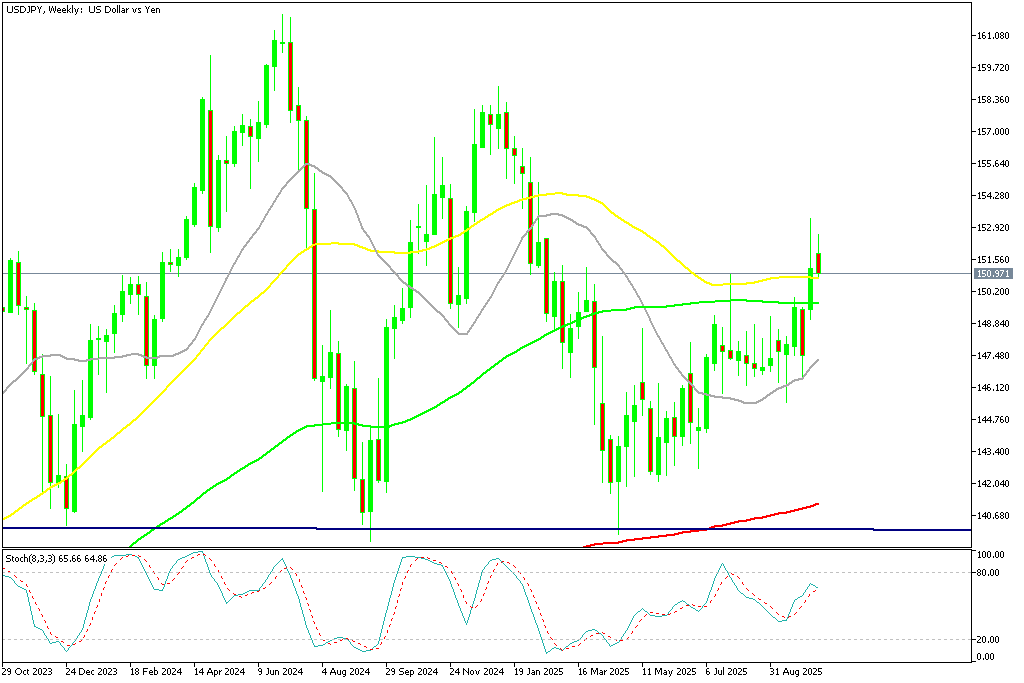

USD/JPY Returns to 150

Foreign exchange markets saw sharp swings. Early in the week, U.S. yield differentials and Japanese capital outflows pushed the dollar above ¥150, but disappointing U.S. jobs data triggered profit-taking, causing the USD/JPY to slide by four yen from its peak. However, the new BOJ governor the JPY has weakened and USD/JPY soared to 153 but returned below 152 yesterday.

USD/JPY – Weekly Chart

Cryptocurrency Update

Bitcoin Retests the Support Indicator

Cryptocurrencies remained highly active over the summer. Bitcoin (BTC) climbed to fresh highs of $123,000 and $124,000 in July and August, supported by institutional inflows and technical strength. However, remarks from Treasury Secretary Scott Bessent ruling out U.S. increases to BTC reserves triggered a steep pullback, sending the coin down below $105,000 before finding support at the 200 daily SMA (purple) and recovering above $115,000 but then fell toward $100K again. However last week BTC has turned higher again, climbing above $114K over the weekend.

BTC/USD – Daily chart

Ethereum Climbs Above $4,000

Ethereum (ETH) has been similarly strong, surging toward $4,800, its highest since 2021 and near its all-time peak of $4,860. Despite a dip last week, ETH found support at the 20-day SMA, with retail enthusiasm and renewed institutional participation driving fresh upside momentum. ON Friday we saw a dive below $3.500 however buying resumed on Sunday and ETH/USD climbed above $4,500 but returned back down below $4,000 again this week.

ETH/USD – Daily Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

ABOUT THE AUTHOR

See More

Skerdian Meta

Lead Analyst

Skerdian Meta Lead Analyst.

Skerdian is a professional Forex trader and a market analyst. He has been actively engaged in market analysis for the past 11 years. Before becoming our head analyst, Skerdian served as a trader and market analyst in Saxo Bank's local branch, Aksioner. Skerdian specialized in experimenting with developing models and hands-on trading. Skerdian has a masters degree in finance and investment.

Related Articles

Sidebar rates

Related Posts