US Session Forex Brief, Dec 18 – The Buck Gets Smashed Ahead of the Last Rate Hike for the Year

The Italian budget problem finally found a solution today, but I think that it will return again next year.

There have been three major issues that the global economies have been facing this year: the trade war between US and China, the Italian budget for next year and Brexit. All of them are coming to an end as we head towards the end of the year. Brexit will go one way or another in January although it looks increasingly likely that Britain might crash out of the EU with no deal. The war between China and the US is cooling off as well after the meeting between Donald Trump and China’s President Xi in the G20 summit, although the clashes between the two titans continue at the World trade Organization. Now, we see that the issue with the Italian budget deficit has been resolved as well.

The Italian leaders Luigi Di Maio and Salvini wanted the deficit for next year at 2.4%, but the European Commission had been stubbornly rejecting it on the basis that Italy already has a huge national debt at 130% of the GDP, also arguing for a lower economic growth next year than what the Italian leaders were projecting. The EU was threatening Italy with fines and it seems that the Italian leaders have accepted the lower deficit, which is now projected at 2.04%, from 2.4% previously. Although, I think that the Italians will sweep the deficit rules under the carpet next year and go ahead with their plan, increasing the deficit.

We have also had inflation reports being released today. Early this morning, the UK CPI (consumer price index) report was released and it ticked lower from last month, although that’s not a bad thing for Britain since inflation has been quite high during this year. But, a decline in inflation is not good for Canada. Prices fell by 0.4% in November in Canada, which is the third decline in four months. Let’s see the reports in the sections below.

The European Session

- German PPI – Producer price index was expected to have declined by -0.1% in Germany in November, but it increased by 0.1% instead. The PPI is holding on well in Germany despite falling Oil prices.

- Eurozone Construction Output – Construction output for October in the Eurozone declined by 1.6%. September was quite good as the output increased by 2.0% which was revised higher to 2.1% today. September’s annualized number was also revised higher to 4.8% from 4.6% today, but the annualized construction number for October came at 1.8%.

- UK CPI Inflation – The CPI (consumer price index) ticked lower to 2.3% in Britain in November as expected, from 2.4% previously. The House price index also cooled off to 2.7% against 3.3% expected. October’s number was also revised lower to 3.0% from 3.5% previously. The PPI input declined 2.3%, which is a smaller decline than 2.8% expected.

- Italian Budget Deficit – The European Commission and the Italian leaders finally came to a consensus on the deficit for next year’s budget. DI Maio and Salvini agreed to lower the deficit to 2.04% from 2.4% previously. But, I don’t think they will stick to it next year. They just convinced the EU to pass the budget.

- Saudis Try to Prop Up Oil Prices – The Saudi Oil Minister said a while ago that fundamentals are not to blame for the decline in Oil prices. What happened to the oil market was political, macroeconomic and speculative trading, and inventories are drawing down by the end of Q1 2019. He added that all OPEC countries are committed to cuts of 3% and that non-OPEC countries have committed to cuts of 2%, including Russia.

The US Session

- US MBA Mortgage Applications – Mortgage applications declined by 5.9% in the second week of December. Purchase index came at 238.6 vs 256.1 prior, market index came at 325.9 vs 346.0 prior, and refinancing index also declined to 832.2 against 851.6 in the previous week.

- Canadian CPI Inflation – YoY CPI inflation cooled off to 1.7% in Canada against 1.8% expected and down from 2.4%. Although in November, inflation declined by 0.4%. Core common CPI came at 1.9% against 1.9% previously, core median ticked lower to 1.9% from 2.0% prior, and core trim also fell to 1.9% from 2.1% previously.

- US Current Account for Q3 – The US current account came at $124 billion against $125 billion expected. Although, the number for Q2 was revised a bit higher. As a percentage of US GDP, the deficit increased to 2.4 percent from 2.0 percent. The increase mainly reflected a $24B increase in the deficit on goods

- Junker Tries to Scare the British Leavers – The Head of the European Commission Juncker said that a disorderly Brexit would be an absolute catastrophe for the UK. Both sides are trying to play the chicken game, trying to force concessions from the other side.

- FED Meeting – Today, the Federal Reserve will meet for the last time this year and they have planed one last rate hike. But, the market has priced that in already so the interest will concentrate on the statement and the press conference from Powell.

Trades in Sight

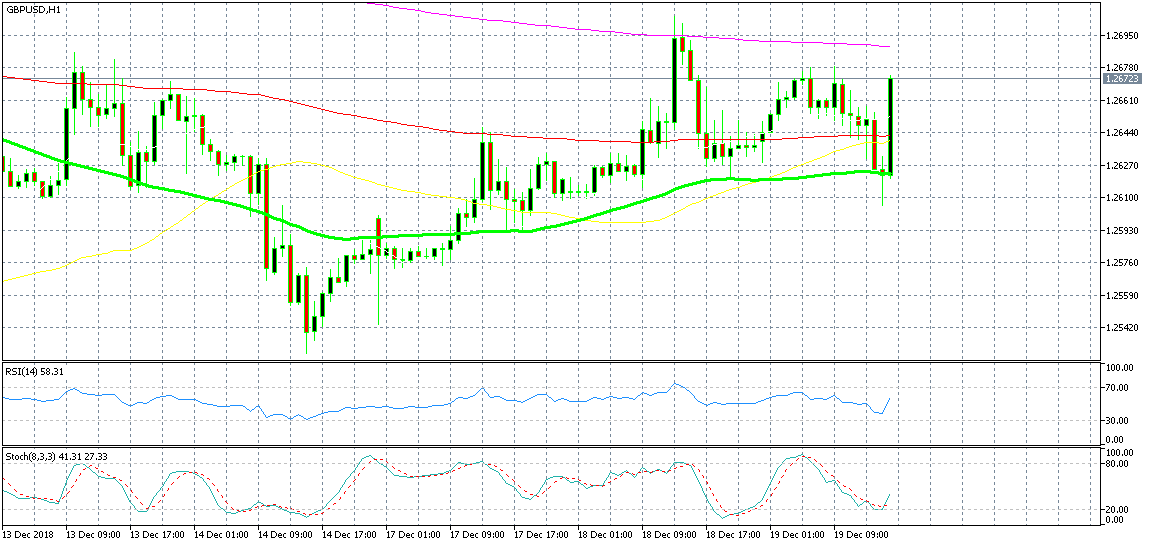

Bullish GBP/USD

- The trend has turned bullish for this pair this week

- The retrace lower was complete an hour ago

- The 100 SMA was providing support

- The candlestick formed a doji

The 100 SMA held well today

GBP/USD has turned bullish this week. This pair retraced lower during the European session but the 100 SMA (green) held its ground just like yesterday. The price formed a doji above it which is a reversing signal. The retrace lower was complete as stochastic got oversold so the reversing pattern was complete. Now, it has jumped around 50 pips higher.

In Conclusion

The final FED meeting for the year is approaching. It will be held this evening and the FED is expected to hike interest rates to 2.50% from 2.25% previously. Although, the USD is in decline since the market is assuming that the FED will turn dovish today and cool off the pace of rate hikes for next year.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts