EUR/USD to Fall Further As US Services Increase, While in Europe They Cool Off

US Services show that the US economy will have an easy winter, unlike in Europe

It seems like the divergence between the US and Eurozone economies is beginning to resurface again. We remember from last year that after the bounce in summer following the covid restrictions and lockdowns in Q2, the restrictions returned in full swing in Europe during the winter of 2020-21. The Eurozone economy fell into recession again, especially services which was the hardest hit sector obviously, while the US economy kept expanding at an impressive speed.

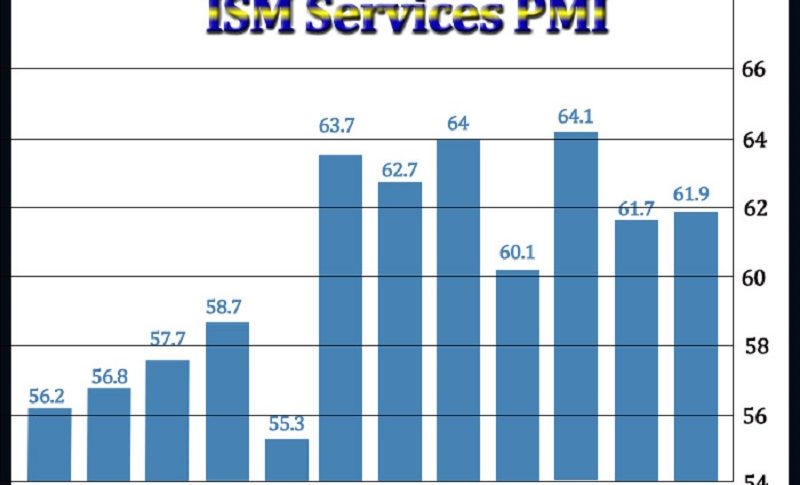

In summer, services recovered after the reopening of the countries, while the economy rebounded. Although, today’s final services report for September from the Eurozone showed that this sector is cooling off again, falling to several-month lows, while now the US ISM non-manufacturing report showed an improvement instead. So, Europe might be heading toward another recession in winter and this is the first sign. If that happens, then expect EUR/USD to fall further.

EUR/USD Live Chart

US service sector data from the ISM

- September ISM services index 61.9 points vs 60.0 expected

- August ISM non-manufacturing was 61.7 points

- Employment 53.0 points vs 53.7 prior

- New orders 63.5 points vs 63.2 prior

- Prices paid 77.5 points vs 75.4 prior

- Business activity 62.3 points vs 60.1 prior

- Backlog of orders 61.9 points vs 61.3 prior

- New export orders 59.5 points vs 60.6 prior

- Imports 47.7 points vs 48.7 prior

- Inventories 46.1 points vs 46.9 prior

- “Transportation bottlenecks are increasing, resulting in longer lead times and missed appointments.” [Accommodation & Food Services]

- “Constraints on logistics from a cost and availability standpoint continue to be an issue.” [Construction]

- “Lead times on electronics and computer chips have greatly increased. Outlook for higher education remains flat for most colleges, not including elite and Ivy League institutions.” [Educational Services]

- “International and domestic demand remains very strong.” [Finance & Insurance]

- “Retaining clinical and temporary staffing is critical at this time. With the Delta variant’s spread, we continue to see increased (COVID-19) cases, but not as bad as January 2021. Vaccinations are clearly working. Most inpatient hospitalizations are of unvaccinated patients. The supply chain is still being impacted significantly by increased lead times for equipment and supplies.” [Health Care & Social Assistance]

- “The semiconductor (shortage is) impacting server delivery. Alternate parts and engineering efforts are being used to create workaround solutions.” [Information]

- “Both domestic and international logistics are increasing lead times about six weeks for ocean freight and two weeks for domestic freight.” [Management of Companies & Support Services]

- “Inventories shrinking due to global shipping logistics being a seller’s/provider’s market, with primary focus on yield versus market expansion.” [Professional, Scientific & Technical Services]

- “Lead times have improved slightly over the last period, but still remain lengthy relative to pre-pandemic levels. We continue to see rising costs for both supply and service inputs. The effects of these price increases have the potential to significantly impact our operations through the end of the year, especially if seasonal trends prove exceptionally strong.” [Public Administration]

- “Business volumes remain remarkably high, although material shortages persist.” [Real Estate, Rental & Leasing]

- “Still experiencing very strong demand. Supply chain is still a challenge.” [Retail Trade]

- “Demand far outweighs supply for goods and services.” [Transportation & Warehousing]

- “We continue to deal with extended delivery lead times and high costs. Stress on the supply chain beginning to be reflected in the quality of products offered and delivered. Current buying strategy is to wait – except with equipment, as (price) increases are expected.” [Utilities]

- “Continued constrained supply of many key product groups. Also, inflationary pressures in most areas of the business keep driving costs higher. Inconsistent COVID-19 restrictions throughout the country are creating unstable business conditions that are concerning. However, business continues to be strong overall.” [Wholesale Trade]

The bolded is informative because it speaks to inflation expectations. If you expect prices to continue rising, you buy anyway. If you think they’re going to come back down, you wait. However, it’s interesting to note that price inflation is becoming embedded in equipment (at least in the utilities sector).

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts