Producer Inflation Slows, Following Yesterday’s Softer US CPI

Yesterday the US CPI report showed that inflation slowed more than expected in May, today the PPI inflation followed suit, falling to 2.2%.

Yesterday the US CPI report showed that inflation slowed more than expected in May, today the PPI inflation followed suit, coming at 2.2%. However, while yesterday the USD dived more than 100 pips lower, today it continues to crawl higher, apart from a small dip following the release of the Producer Price Index numbers, also being affected by higher unemployment claims for last week.

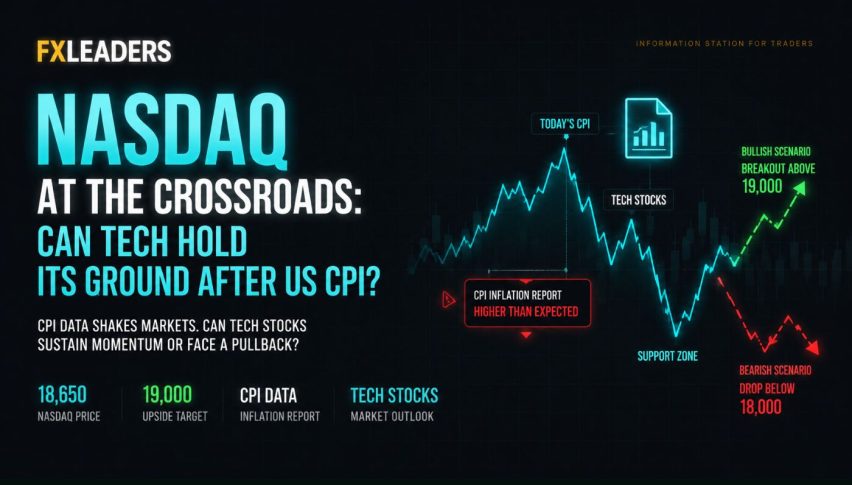

Came in at +0.16% (unrounded) vs. expected +0.3%. This indicates lower inflationary pressures than anticipated. The US dollar experienced significant selling pressure post-CPI release, particularly against riskier currencies and commodity-linked currencies. Stock markets, including the NASDAQ and S&P 500, surged to record highs on expectations that the Federal Reserve might adopt a more dovish stance in response to softer inflation data. But, contrary to market expectations of two rate cuts, the FOMC signaled only one rate cut for the year, suggesting a less dovish stance than anticipated.

Despite initial weakness post-CPI, the US dollar rebounded and strengthened as the FOMC’s decision diverged from market expectations. This divergence underscored the Fed’s cautious approach to monetary policy despite softer inflation data. The initial market reaction was based on expectations of a more accommodative Fed in response to subdued inflation. However, the actual FOMC decision to maintain a more conservative rate-cutting outlook surprised markets, leading to a reversal in the US dollar’s fortunes.

May 2024 US Producer Price Index (PPI)

Overall PPI:

- Year-on-Year (YoY): +2.2% vs. +2.5% expected (Prior: +2.2%)

- Month-on-Month (MoM) – Final Demand: -0.2% vs. +0.1% expected (Prior: +0.5%)

Excluding Food and Energy (Core PPI):

- YoY: +2.3% vs. +2.4% expected

- MoM: 0.0% vs. +0.3% expected (Prior: +0.5%)

Details:

- The decrease in May’s final demand prices was driven by a significant 0.8% decline in the index for final demand goods, the largest drop since October.

- Energy prices fell sharply by 4.8%, with gasoline prices leading the decline by dropping 7.1%.

- Prices for final demand services remained unchanged during the period.

Market Implications:

- Fed Policy Expectations:

- Fed Funds Futures: The market has adjusted its expectations, now fully pricing in two rate cuts this year, reflecting the softer inflation outlook as indicated by the PPI data. Yesterday FED fund rates fell to just one rate cut after the FOC meeting, while today after the soft PPI and unemployment claims we’re back to two rate cuts.

- US Inflation Outlook:

- Softer Inflation: The lower-than-expected PPI figures suggest a moderation in inflationary pressures for the retail consumer, so the CPI is likely to continue to fall further.

- Energy Prices: The significant decline in energy prices, particularly gasoline, contributed heavily to the lower PPI, indicating potential relief for consumers and businesses.

- US Economic Growth:

- Potential Support for Equities: Softer inflation data might support equities, as lower input costs can improve profit margins for companies.

- Bond Market: Lower inflation expectations could lead to declining bond yields, as investors anticipate less aggressive monetary tightening.

The May 2024 PPI data shows a softer inflation outlook than expected, with declines in both headline and core measures. This has led the market to fully price in two rate cuts by the Fed this year, reflecting a shift in expectations towards a more accommodative monetary policy stance. The significant drop in energy prices, particularly gasoline, played a crucial role in the lower PPI figures. As a result, this could provide some relief to consumers and businesses, potentially supporting economic growth and market sentiment.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts