btc-usd

Forex Signals October 16: TSM, Schwab, U.S. Bancorp Earnings Before Market Open

Earnings season intensifies as Taiwan Semiconductor, Charles Schwab, and U.S. Bancorp unveil their Q3 results.

•

Last updated: Thursday, October 16, 2025

Quick overview

- Earnings season heats up with Taiwan Semiconductor, Charles Schwab, and U.S. Bancorp releasing their Q3 results.

- The U.S. dollar continues to weaken as dovish comments from the Fed suggest potential rate cuts ahead.

- Treasury Secretary Bessent emphasizes cooperation with China amid ongoing trade tensions, warning of economic repercussions.

- Oil prices decline while gold surges, reflecting diverging trends in commodities as investors seek safe havens.

Live BTC/USD Chart

BTC/USD

0.0000

MARKETS TREND

Earnings season intensifies as Taiwan Semiconductor, Charles Schwab, and U.S. Bancorp unveil their Q3 results.

Dollar Slides Further as Dovish Fed Tone Dominates

The U.S. dollar continued to weaken for a second consecutive session as traders reacted to dovish commentary from Federal Reserve Chair Jerome Powell. His remarks highlighted potential softness in the labor market and hinted that the central bank could soon pause its balance sheet runoff, reinforcing expectations for rate cuts.

Market pricing now reflects an anticipated 25-basis-point cut in both November and December, as investors adjust to the Fed’s more accommodative stance.

Bessent Urges Cooperation with China Amid Trade Tensions

Treasury Secretary Bessent struck a conciliatory tone on U.S.-China relations, saying that Washington “wants to help China, not hurt it.” However, he warned that Beijing’s economic coercion could ultimately undermine its own growth.

He added that multiple high-level meetings are scheduled this week to address China’s latest trade restrictions, a topic increasingly central to global market sentiment.

Fed Officials Reinforce Dovish Shift

Adding to the softer rhetoric, Fed Governor Miran—a recent Trump appointee known for her dovish leanings—remarked that “two more rate cuts this year sound realistic.”

Meanwhile, the Federal Reserve’s Beige Book painted a picture of a slowing but stable economy, noting that overall U.S. activity was little changed in recent weeks. Most districts described growth as modest or flat, with early signs of easing demand, while employment conditions remained steady.

Commodities Diverge: Oil Weakens, Gold Surges

Oil prices extended their downward slide, with WTI crude falling to $58.20, marking an 18% decline year-to-date—well below the $130 highs seen in 2022.

Analyst Adam Button noted that global oil demand has hit record levels, but OPEC+’s continued supply expansion has kept prices subdued.

In contrast, precious metals surged. Gold jumped $63 (+1.54%) to $4,206, Silver climbed $1.62 (+3.14%) to $53.07, with both on pace for record closing highs as investors sought refuge amid global uncertainty.

Stocks Mixed Ahead of Key U.S. Data

Major U.S. stock indices traded choppily through the session before closing mixed. The Dow Jones Industrial Average surrendered part of yesterday’s gains, while the S&P 500 and Nasdaq finished near mid-range levels, reflecting investor caution ahead of upcoming data releases.

Key Forex Events to Watch Today:

Thursday will bring Australia’s employment figures and, in the U.S., a trio of reports—PPI, retail sales, and weekly jobless claims—provided the government shutdown concludes in time. Friday’s focus will turn to the housing sector, with building permits and housing starts due for release.

UK Labor Data Keeps BoE on Hold

Across the Atlantic, the UK’s average earnings index (3m/y) is expected to remain at 4.7%, alongside an unchanged unemployment rate of 4.7%.

With wage growth still elevated, the Bank of England faces persistent inflation pressures and is likely to keep interest rates steady through year-end. Fiscal tightening and weak consumer spending continue to cloud the outlook for the British economy.

Major Earnings Releases – October 2025 Preview

Taiwan Semiconductor Manufacturing Co. (TSM)

- Earnings Release: Q3 2025 Results

- Time: Before Market Open (BMO)

- Consensus EPS Estimate: $2.63 per share

Focus Areas:

- Global chip demand recovery amid AI-driven orders

- Impact of U.S.-China trade tensions on supply chains

- Foundry pricing and capacity utilization outlook

- Market Sentiment: TSM’s results will serve as a barometer for semiconductor health and global tech manufacturing trends.

The Charles Schwab Corporation (SCHW)

- Earnings Release: Q3 2025 Results

- Time: Before Market Open (BMO)

- Consensus EPS Estimate: $1.25 per share

Focus Areas:

- Net interest income trajectory amid rate-cut expectations

- Client inflows and trading activity

- Brokerage margin recovery after a volatile quarter

- Market Sentiment: Investors will watch for commentary on retail trading volume and asset management growth as market volatility impacts client behavior.

U.S. Bancorp (USB)

- Earnings Release: Q3 2025 Results

- Time: Before Market Open (BMO)

- Consensus EPS Estimate: $1.12 per share

Focus Areas:

- Loan growth and credit quality trends

- Deposit stability amid competition for yields

- Cost-cutting measures and digital banking adoption

Gold Makes It Above $4,200

Although demand for safe haven assets is still high, gold fell precipitously from record highs following the Fed’s most recent rate decrease as profit-taking was prompted by Powell’s cautious tone. Earlier this week, gold jumped beyond $3,700 and reached $3,707.42 following the Federal Reserve’s announcement of a 25 basis point rate decrease to 4.25%. But the impetus soon waned, and prices dropped back to $3,627, a $80 decline from the new all-time high. As traders locked in profits after the rally driven by dovish predictions, there was a sudden fall but buyers returned on Friday pushing the price $60 higher. Yesterday buyers continued to push and XAU reached another record high at $4,218.

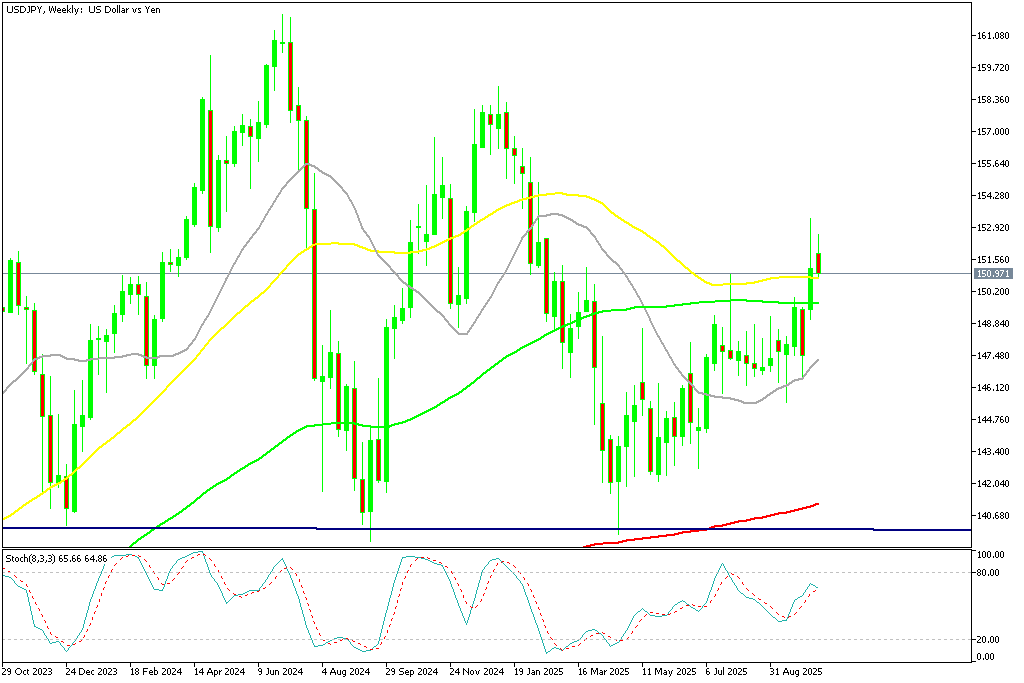

USD/JPY Breaks Above the Range After the New BOJ Governor

Foreign exchange markets saw sharp swings. Early in the week, U.S. yield differentials and Japanese capital outflows pushed the dollar above ¥150, but disappointing U.S. jobs data triggered profit-taking, causing the USD/JPY to slide by four yen from its peak. However, the new BOJ governor the JPY has weakened and USD/JPY soared to 153 but returned below 152 yesterday.

USD/JPY – Weekly Chart

Cryptocurrency Update

Bitcoin Rebounds Off Support

Cryptocurrencies remained highly active over the summer. Bitcoin (BTC) climbed to fresh highs of $123,000 and $124,000 in July and August, supported by institutional inflows and technical strength. However, remarks from Treasury Secretary Scott Bessent ruling out U.S. increases to BTC reserves triggered a steep pullback, sending the coin down below $105,000 before finding support at the 200 daily SMA (purple) and recovering above $115,000. However this week BTC has turned lower again, approaching $110K.

BTC/USD – Weekly chart

Ethereum Returns Above $4,000 After the Flash Crash

Ethereum (ETH) has been similarly strong, surging toward $4,800, its highest since 2021 and near its all-time peak of $4,860. Despite a dip last week, ETH found support at the 20-day SMA, with retail enthusiasm and renewed institutional participation driving fresh upside momentum. ON Friday we saw a dive below $3.500 however buying resumed on Sunday and ETH/USD climbed above $4,000.

ETH/USD – Weekly Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

ABOUT THE AUTHOR

See More

Skerdian Meta

Lead Analyst

Skerdian Meta Lead Analyst.

Skerdian is a professional Forex trader and a market analyst. He has been actively engaged in market analysis for the past 11 years. Before becoming our head analyst, Skerdian served as a trader and market analyst in Saxo Bank's local branch, Aksioner. Skerdian specialized in experimenting with developing models and hands-on trading. Skerdian has a masters degree in finance and investment.

Related Articles

Sidebar rates

Related Posts