US Session Forex Brief, March 18 – Risk Currencies Benefit From Weaker USD

Markets have been quiet today as we wait for the third Brexit vote tomorrow, but the USD continues to remain weak

The US Dollar continues to remain soft today. The Buck had a bad week last week as it turned bearish on Friday the previous week after the soft non-farm employment change. Earnings and the unemployment rate posted some decent figures on the same day, but the market turned bearish on the employment figures which kept the Buck subdued for the entire week. Today, the situation seems pretty similar as the USD continues to slide lower across the board.

The Euro was one of the biggest winners from that price action last week with EUR/USD climbing more than 100 pips higher despite a dovish shift in the European Central Bank. Today the uptrend continues and it has stretched further above, breaking last week’s resistance at 1.1340. Although, the biggest winner today have been the commodity currencies and the Aussie in particular. Iron ore prices have been increasing which have helped the AUD, as well as the widening bond spreads. That has pulled the NZD higher as well. The GBP, on the other hand, has been pretty quiet today, but tomorrow is the third Brexit vote which will be the final chance for Theresa May, so that makes sense.

European Session

- Germany Doesn’t Like Hard Brexit – Germany’s foreign minister, Heiko Maas, commented early this morning saying that “it’s worth having another round of talks before it comes to a hard Brexit”. They said last week that talks are over, but we know no one likes a hard Brexit. Although, what do they expect to change if they still keep the same positions?

- OPEC Talking Oil Higher – The OPEC+ April meeting seems to be postponed for May which should be held in Riyadh as Bloomberg reported. A joint statement from OPEC+ suggested that members will exceed voluntary output adjustments in coming months. They see overall February output cuts conformity at 90% and have also added Nigeria, Kazakhstan, Iraq and UAE as members. The Saudi Oil Minister also commented that the inventory glut needs to be drained before cuts are ended. But he is confident that March oil output cuts compliance will exceed 100%.

- Emergency EU Brexit Summit? – The editor of BBC’s Europe, Katya Adler, tweeted that there are rumours in EU quarter that an emergency EU summit on Brexit will take place on March 28. Well, today is the third time that Theresa May will try to push her Brexit deal past the British Parliament, so there’s lots of things on the agenda until March 28.

- Eurozone Trade balance – The trade balance has been shrinking in the Eurozone during September and October as reports released towards the end of last year showed. Although, it started increasing again in November and December from €12.5 billion in October to €15.6 billion in December which was revised higher to €16 billion. Today’s report was expected to show another increase to €17.2 billion. The actual number missed expectations slightly but increased from the previous month, coming at €17 billion. I don’t think Donald Trump will like that. Wait for auto tariffs to come along soon.

- UK Government Prefers Short Brexit Extension – The UK PM spokesman James Slack commented earlier and this was the main takeaway. He added that if the vote fails tomorrow, we will seek longer extension. Is there anyone serious enough in this process? The UK will then have to take part in European Parliament elections and the Brexit date can be changed with secondary legislation. Talks are ongoing between government and DUP Party. The government doesn’t rule out a Brexit vote next week but it is still preparing for no-deal Brexit.

The US Session

- Foreign Securities Purchases in Canada – In December last year, the total value of domestic stocks, bonds, and money-market assets purchased by foreigners during declined dramatically by $18.96 billion which was revised lower today to $-20.49 billion. Although, that was reversed completely today as Foreign Securities Purchases increased by $28.40 billion, beating expectations of $15.03 billion.

- US NAHB Housing Market Index – This housing market index dipped to 56 points in December as the sentiment turned negative that month and the US economy went through a soft spot during the last few months of last year. But, it started increasing in January and it grew to 62 points last month. This month this indicator was expected to tick higher to 63 points but missed expectations and remained unchanged.

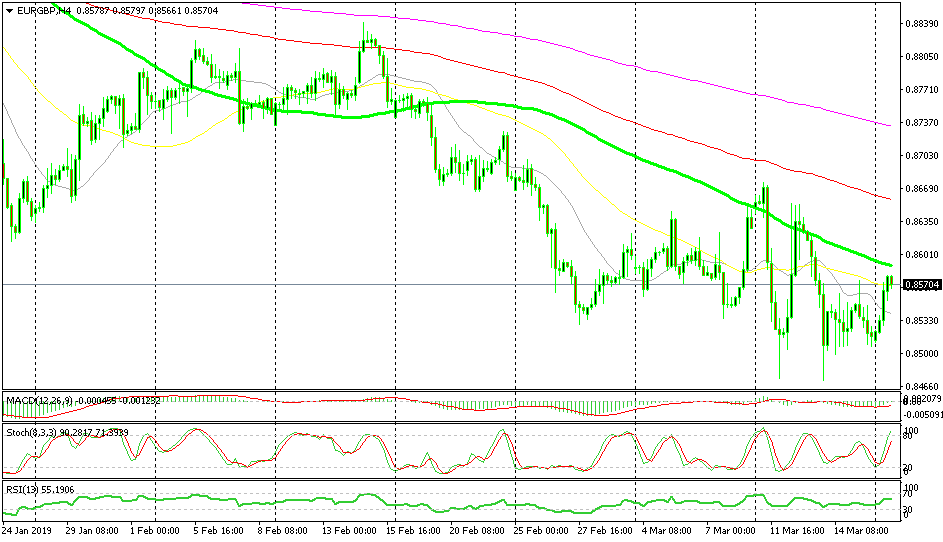

Bullish EUR/GBP

- The trend is bearish

- The retrace up is complete

- The 100 SMA is waiting to provide resistance above

The 100 SMA should provide resistance again today

This pair turned bearish in the first week of February as odds of a hard Brexit diminished. The odds have increased again this month but the trend remains to be bearish. Today, this pair has climbed higher as EUR/USD continues to march higher stubbornly but the bullish retrace is complete now as the stochastic indicator shows on the H4 time-frame chart. If the buyers continue to push higher, the 100 SMA (green) will be waiting to provide resistance.

In Conclusion

All the economic data is out today, not that there was much to be worried about or to move markets around. For the remainder of the day we will have to trade the market sentiment, but the market will be mostly concentrated on the Brexit vote which will take place tomorrow. So, don’t expect too much price action today.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts