btc-usd

Forex Signals Sept 16: Stable UK Jobs and Canada Inflation, US Spending Picks Up

Global markets face a packed day of data releases that could guide central bank expectations and investor sentiment.

•

Last updated: Tuesday, September 16, 2025

Quick overview

- Global markets are experiencing volatility with a mix of optimism and selloff, influenced by key data releases and central bank expectations.

- Tech stocks, particularly Google and Tesla, are in focus due to significant developments in AI and insider trading, respectively.

- The Federal Reserve's upcoming policy decision is central to market sentiment, with expectations leaning towards a dovish tone and a potential rate cut.

- In Canada, stronger manufacturing data has bolstered the Canadian dollar, while inflation figures will be crucial for the Bank of Canada's policy outlook.

Live BTC/USD Chart

BTC/USD

0.0000

MARKETS TREND

Global markets face a packed day of data releases that could guide central bank expectations and investor sentiment.

Market Turmoil Despite Early Optimism

Equities started Monday with modest gains that built steadily, but the upbeat tone faded into a broader market selloff by the end of the day. Sentiment had been lifted late last week after Elon Musk disclosed a $1 billion purchase of Tesla stock, his first major insider buy in years. Optimism also received a boost from a dovish reading on the Empire Fed index, giving investors hope that looser monetary conditions may be on the horizon.

Tech Stocks in Focus

Google shares hit record territory after unveiling its new Nano Banana model, part of growing momentum around its Gemini AI platform. The excitement around artificial intelligence kept technology stocks in the spotlight and provided some insulation against wider market weakness. Tesla, too, maintained strength on the back of Musk’s purchase, underscoring how influential high-profile moves remain in shaping near-term sentiment.

Fed Expectations and Market Risks

The week’s central focus is the Federal Reserve’s policy decision. Markets are positioned for a dovish tone and a widely expected 25 basis point cut, though the odds of a larger 50-point move have now faded to nearly zero. The US dollar has softened as traders bet on lower rates, while gold and other risk-sensitive assets have struggled to gain momentum. A potential “sell-the-fact” reaction remains a risk once the Fed decision is released on Wednesday, particularly given the limited leaks from policymakers this time around.

Canadian Dollar and Commodity Support

On the currency front, stronger manufacturing data helped push back against fears of a NAFTA breakdown, lifting the Canadian dollar to a 10-day high. Commodity-linked currencies broadly benefited from renewed strength in gold, which printed a record high for the first time in a week. This rally in precious metals further underpinned support for exporters, bolstering the Canadian dollar’s performance.

Key Market Events to Watch Today

UK Jobs Report: Labor Market Under the Microscope

The UK employment report will reveal whether the labor market is holding steady or showing fresh cracks. Economists expect the 3-month unemployment rate for July to remain at 4.7%, while wage growth is projected to tick higher to 4.7% from 4.6%. Morgan Stanley anticipates slower job creation of around 200k, with vacancies largely unchanged. However, the bank warns of ongoing inaccuracies in ONS data collection, which has added uncertainty to recent releases. Pay pressures are expected to remain contained, with wage growth excluding bonuses seen at 4.6%, reflecting the absence of new major pay deals.

US Retail Sales: Gauging Consumer Resilience

Across the Atlantic, US retail sales are forecast to increase by 0.3% in August, slightly cooler than July’s 0.5%. Excluding autos, the figure is expected to match July’s 0.3%. Bank of America data showed household spending rose modestly, though growth continues to diverge across age groups. Younger households and Gen X are experiencing weaker income gains, with smaller pay bumps from job changes weighing on momentum. Meanwhile, easing rental costs could help narrow the spending gap between renters and homeowners, offering some relief for household budgets.

Canadian CPI: Inflation and BoC Outlook

In Canada, CPI figures will play a crucial role in shaping expectations for the Bank of Canada’s policy path. Inflation remains inside the BoC’s 1–3% range but is hovering near the upper bound. Recent deliberations highlighted policymakers’ concern with underlying inflation strength, even as growth and jobs data have softened. With tariffs still a factor, the central bank expects growth to resume in Q3 while inflation steadies around 2%. Markets will be watching closely to see if the data strengthens the case for further easing.

Last week, markets were quite volatile again, with gold soaring to $3,6065. EUR/USD continued the upward move toward 1.17.80, while main indices closed higher again. The moves weren’t too big though, and we opened 35 trading signals in total, finishing the week with 23 winning signals and 12 losing ones.

Gold Reaches Another Milestone

Gold continues to attract strong safe-haven flows although we saw a slight pullback yesterday. Prices surged above $3,685 early yesterday, hitting a new record high, so buyers are in total control, while China has resumed buying bullion. Technical charts now highlight the $3,700 level as the next major resistance, which will be broken soon as the upside accelerates, however an upside-down daily candlestick is a bearish signal, which could indicate a deeper pullback after such a rally.

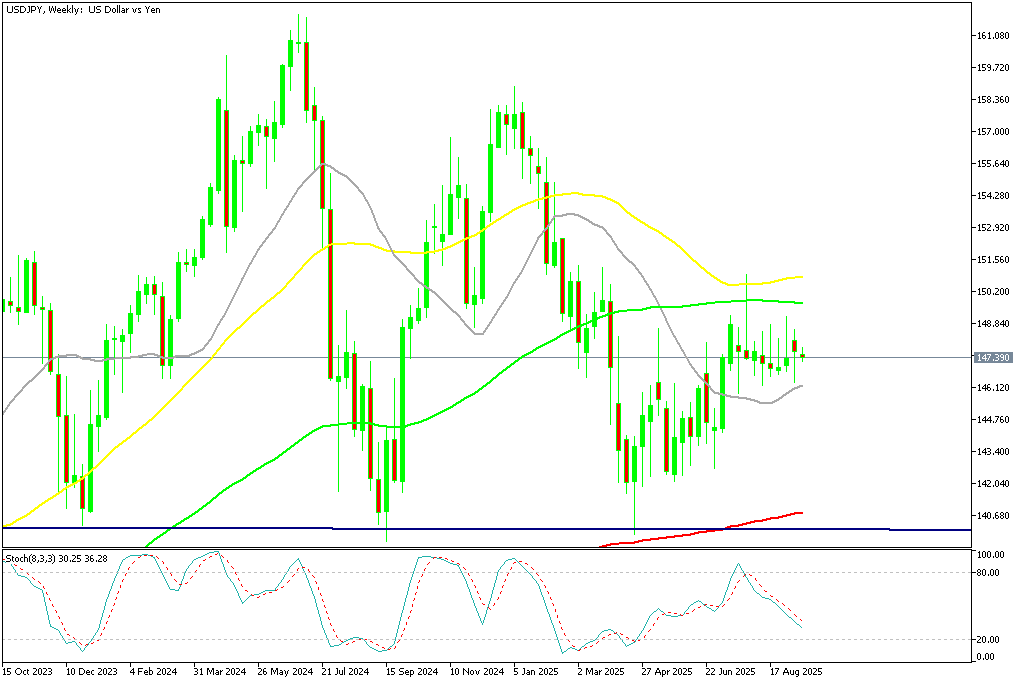

USD/JPY Continues Trading in the Range

Foreign exchange markets saw sharp swings. Early in the week, U.S. yield differentials and Japanese capital outflows pushed the dollar above ¥150, but disappointing U.S. jobs data triggered profit-taking, causing the USD/JPY to slide by four yen from its peak. The move underscored persistent volatility as traders weighed Japan’s intervention risks against evolving Fed expectations.

USD/JPY – Weekly Chart

Cryptocurrency Update

Bitcoin Starts Rebound Off the 20 SMA

Cryptocurrencies remained highly active over the summer. Bitcoin (BTC) climbed to fresh highs of $123,000 and $124,000 in July and August, supported by institutional inflows and technical strength. However, remarks from Treasury Secretary Scott Bessent ruling out U.S. increases to BTC reserves triggered a steep pullback, sending the coin down to $113,000 before recovering above $116,000 last week, however sellers returned and sent BTC below $110,000, however we saw a rebound off the 20 weekly SMA (gray) yesterday.

BTC/USD – Weekly chart

Ethereum Climbs Above $4,500

Ethereum (ETH) has been similarly strong, surging toward $4,800, its highest since 2021 and near its all-time peak of $4,860. Despite a dip last week, ETH found support at the 20-day SMA, with retail enthusiasm and renewed institutional participation driving fresh upside momentum. However buying resumed and on Sunday ETH/USD printed another record at $4,941. However we saw a retreat to $,000 lows over the weekend, but yesterday buyers returned.

ETH/USD – Daily Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

ABOUT THE AUTHOR

See More

Skerdian Meta

Lead Analyst

Skerdian Meta Lead Analyst.

Skerdian is a professional Forex trader and a market analyst. He has been actively engaged in market analysis for the past 11 years. Before becoming our head analyst, Skerdian served as a trader and market analyst in Saxo Bank's local branch, Aksioner. Skerdian specialized in experimenting with developing models and hands-on trading. Skerdian has a masters degree in finance and investment.

Related Articles

Sidebar rates

Related Posts

Ava