Forex Signals Sept 24: Markets Eye Key Inflation and Policy Updates: Australian CPI & SNB

This week’s focus shifts to fresh inflation signals from Australia and a policy update from the Swiss National Bank (SNB), both carrying...

•

Last updated: Wednesday, September 24, 2025

Quick overview

- This week, attention is on inflation signals from Australia and a policy update from the Swiss National Bank, both of which could impact global market sentiment.

- U.S. stock indices experienced a pullback after a strong rally, with the Nasdaq leading the decline at 0.95%.

- Economic data showed softer PMI readings, but all measures remained above 50, indicating continued expansion despite a slowdown.

- Fed Chair Jerome Powell highlighted the balancing act of managing inflation risks while navigating a vulnerable labor market.

This week’s focus shifts to fresh inflation signals from Australia and a policy update from the Swiss National Bank (SNB), both carrying potential implications for global market sentiment.

Wall Street Takes a Breather

After weeks of strong momentum, U.S. stock indices finally ran out of steam today. Markets had become stretched after an extended rally, particularly in the Nasdaq, which had outperformed over the past month. The pullback appeared less about negative news and more about investors taking profits after a strong run.

PMI Data Soft but Still Expansionary

Economic data offered a mixed signal. The September flash PMI readings came in softer than the prior month, with manufacturing at 52.0 compared to 53.0 previously, services at 53.9 versus 54.5, and the composite slipping to 53.6 from 54.6. Although weaker, the key reassurance was that all three measures remained above the 50 mark, underscoring that activity continues to expand, albeit at a slower pace.

Indices Retreat After a Strong Month

The major indices all closed in negative territory, led by the Nasdaq’s 0.95 percent drop, its sharpest since early September. The S&P 500 fell 0.55 percent, while the Dow Jones Industrial Average slipped 0.19 percent. These declines follow a strong stretch dating back to late August, where the Nasdaq had led broader gains. The modest retreat signals a healthy correction after nearly a month of consistent advances.

Powell’s Remarks Highlight Balancing Act

Adding to the cautious tone was Fed Chair Jerome Powell, who spoke publicly for the first time since the FOMC rate decision. His comments suggested a central banker carefully navigating competing risks, likening the task to driving in heavy traffic with both hands on the wheel and a foot hovering over the brake. Powell acknowledged that inflation risks remain skewed to the upside, while the labor market now shows increasing signs of vulnerability. He stressed that there is no risk-free path forward: cutting rates too quickly risks leaving inflation unresolved, while keeping policy too restrictive could weaken employment unnecessarily.

Data in Focus This Week

Australian CPI – Wednesday

Australia’s August Monthly CPI Indicator is expected to climb to 2.9% Y/Y from 2.8%, with Westpac projecting a firmer 3.1% due to base effects. July’s reading surprised on the upside at 2.8% Y/Y, driven by electricity, new dwellings, and holiday travel.

For August, Westpac expects electricity rebates in NSW and the ACT to partially offset increases elsewhere, pencilling in a 3% rise in power prices. Headline CPI is forecast to edge just 0.1% higher M/M, nudging the annual pace to 3.1%. Upside risks remain, particularly from homebuilders’ margins.

SNB Policy Decision – Thursday

The Swiss National Bank is widely expected to keep rates unchanged at 0.00%, after cutting to the zero lower bound in June. August inflation held steady at 0.2% Y/Y, broadly in line with forecasts but still slightly above the SNB’s Q3 projection.

Chairman Schlegel has emphasized that the bar for negative rates remains high, though the option is not off the table if needed. While CHF appreciation is a concern, the SNB views it as less severe in the context of global prices. Market odds of another cut are just 5%, with attention shifting to December’s meeting for clearer guidance.

Last week, markets were quite volatile again, with gold soaring to $3,6065. EUR/USD continued the upward move toward 1.17.80, while main indices closed higher again. The moves weren’t too big though, and we opened 35 trading signals in total, finishing the week with 23 winning signals and 12 losing ones.

Gold Continues the March with Another High

Although demand for safe haven assets is still high, gold fell precipitously from record highs following the Fed’s most recent rate decrease as profit-taking was prompted by Powell’s cautious tone. Earlier this week, gold jumped beyond $3,700 and reached $3,707.42 following the Federal Reserve’s announcement of a 25 basis point rate decrease to 4.25%. But the impetus soon waned, and prices dropped back to $3,627, a $80 decline from the new all-time high. As traders locked in profits after the rally driven by dovish predictions, there was a sudden fall but buyers returned on Friday pushing the price $60 higher. Yesterday buyers continued to push and XAU reached another record high at $3,791 before retreating late in the day.

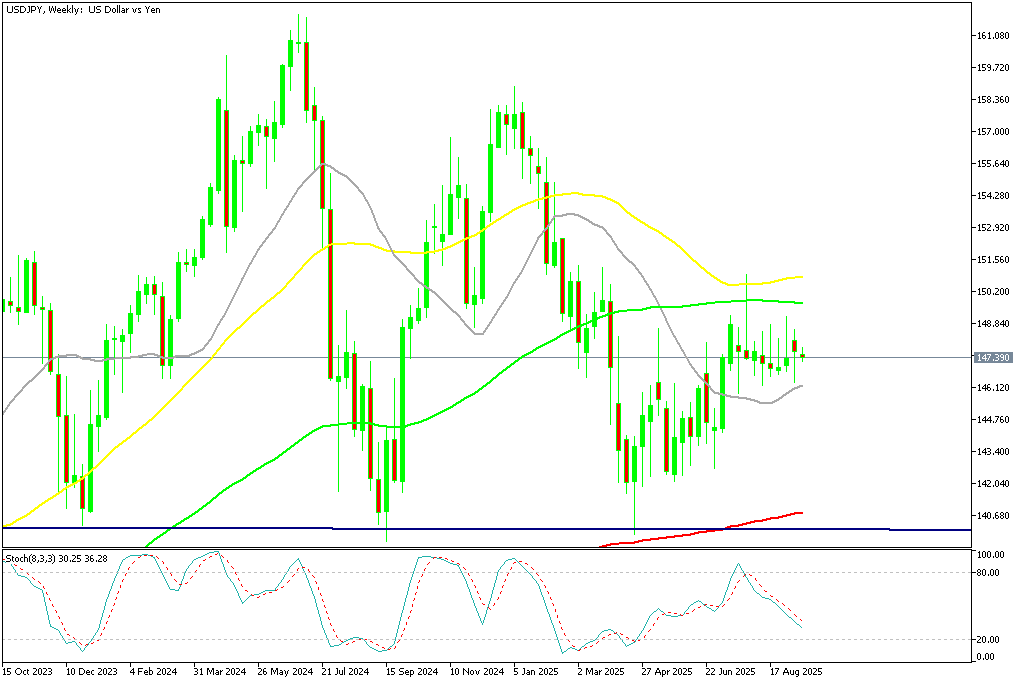

USD/JPY Continues Trading in the Range

Foreign exchange markets saw sharp swings. Early in the week, U.S. yield differentials and Japanese capital outflows pushed the dollar above ¥150, but disappointing U.S. jobs data triggered profit-taking, causing the USD/JPY to slide by four yen from its peak. The move underscored persistent volatility as traders weighed Japan’s intervention risks against evolving Fed expectations.

USD/JPY – Weekly Chart

Cryptocurrency Update

Bitcoin Returns Lower to the 100 SMA

Cryptocurrencies remained highly active over the summer. Bitcoin (BTC) climbed to fresh highs of $123,000 and $124,000 in July and August, supported by institutional inflows and technical strength. However, remarks from Treasury Secretary Scott Bessent ruling out U.S. increases to BTC reserves triggered a steep pullback, sending the coin down to $113,000 before recovering above $116,000 last week, however sellers returned and sent BTC below $110,000, however we saw a rebound off the 20 weekly SMA (gray) but the price is returning down again.

BTC/USD – Weekly chart

Ethereum Heads to $4,o00 Again

Ethereum (ETH) has been similarly strong, surging toward $4,800, its highest since 2021 and near its all-time peak of $4,860. Despite a dip last week, ETH found support at the 20-day SMA, with retail enthusiasm and renewed institutional participation driving fresh upside momentum. However buying resumed and on Sunday ETH/USD printed another record at $4,941. However we saw a retreat toward $4,000 lows over the weekend.

ETH/USD – Daily Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

ABOUT THE AUTHOR

See More

Skerdian Meta

Lead Analyst

Skerdian Meta Lead Analyst.

Skerdian is a professional Forex trader and a market analyst. He has been actively engaged in market analysis for the past 11 years. Before becoming our head analyst, Skerdian served as a trader and market analyst in Saxo Bank's local branch, Aksioner. Skerdian specialized in experimenting with developing models and hands-on trading. Skerdian has a masters degree in finance and investment.

Related Articles

Sidebar rates

Related Posts