btc-usd

Forex Signals Sept 29: PCE Inflation to Test Fed’s Patience on Policy and TSLA Sales

This week’s economic calendar is packed with pivotal Jobs data such the NFP that could influence not only U.S. monetary policy expectations

•

Last updated: Monday, September 29, 2025

Quick overview

- This week's economic calendar features crucial jobs data, including the Non-Farm Payrolls (NFP), which may impact U.S. monetary policy and global market sentiment.

- The latest PCE report indicates stable inflation at 0.2%, with rising personal spending and income suggesting robust consumer activity.

- Durable goods orders unexpectedly surged by 2.9%, signaling renewed strength in manufacturing and business investment.

- Investors are closely monitoring upcoming labor-market reports and inflation data from the Eurozone, as these could influence market dynamics and Federal Reserve policy.

Live BTC/USD Chart

BTC/USD

0.0000

MARKETS TREND

This week’s economic calendar is packed with pivotal Jobs data such the NFP that could influence not only U.S. monetary policy expectations but also global market sentiment.

PCE Report Highlights Stability in Inflation

Last Friday’s U.S. Personal Consumption Expenditures (PCE) report—the Federal Reserve’s preferred inflation measure—showed price growth steady at 0.2%, exactly as expected. Meanwhile, personal spending and personal income both rose, signaling that consumer activity remains robust despite recent market volatility.

A string of upbeat data shaped sentiment heading into the new week, pointing to underlying strength across major sectors of the U.S. economy.

Housing Shows Signs of Gradual Stabilization

Existing home sales came in at 4.00 million (vs. 3.96 million expected), dipping slightly by -0.2% month-over-month but still outperforming forecasts. Home prices climbed 2.0% year-over-year, while inventory rose 11.7% year-over-year—indicating that the housing market may be finding a floor, though recovery remains gradual.

Durable Goods Orders Deliver an Upside Surprise

In a bright spot for manufacturing, durable goods orders jumped +2.9% (vs. -0.5% expected), while core capital goods gained +0.6%. This marked a significant turnaround after several months of weak readings and suggests renewed strength in business investment. The goods trade deficit narrowed sharply to -$85.5 billion (vs. -$95.2 billion expected), reversing much of the earlier tariff-related distortions. However, wholesale inventories fell -0.2% in August, mainly in nondurable goods, highlighting softer restocking momentum as businesses remain cautious about demand.

Growth and Labor Market Remain Robust

The Q2 GDP was revised higher to +3.8%, driven by stronger consumer spending and final sales. On the labor front, initial jobless claims dropped to 218,000 (vs. 235,000 expected), keeping claims near the low end of their 2025 range and reinforcing the view that the jobs market remains resilient.

Data in Focus This Week

Investors will be particularly focused on the labor-market reports to gauge the health of hiring and wage dynamics. With inflation trends in the Eurozone and U.S. wage data also on deck, any surprise—positive or negative—could spark volatility across equities, bonds, and currencies. Markets are bracing for a potentially pivotal week that may shape the Fed’s next steps and set the tone for Q4 trading.

Tesla Q3 Sales

In an effort to take advantage of U.S. EV tax credits, analysts have raised their estimates for Tesla’s third-quarter sales to between 448,000 and 456,000 vehicles, which are anticipated midweek. But fears about demand are maintained by lackluster Europe figures, dwindling incentives, and impending cheaper models.

JOLTS Job Openings – Tuesday

- The latest Job Openings and Labor Turnover Survey (JOLTS) will offer insight into labor demand across the U.S. economy. Investors will be looking for any signs of cooling in job openings, which could indicate easing wage pressures.

RBA Cash Rate Decision – Tuesday

- The Reserve Bank of Australia’s cash rate is expected to remain steady at 3.60%. Any hints in the accompanying statement about future rate cuts or a change in tone could influence market sentiment on both equities and the dollar.

ADP Non-Farm Employment Change – Wednesday

- The ADP report will serve as an early gauge of private-sector hiring ahead of Friday’s official Non-Farm Payrolls (NFP) release. A stronger reading could raise expectations for a more robust labor market.

Eurozone CPI Flash Estimate y/y – Wednesday

- Inflation in the Eurozone is forecast to rise slightly from 2.0% in August to 2.2% in September. This modest uptick will be closely watched for clues about future European Central Bank policy and its impact on global bond yields and currency markets.

Weekly U.S. Unemployment Claims – Thursday

- Initial claims data will provide a near real-time snapshot of labor-market health. A sustained decline in claims would bolster confidence that the labor market remains resilient despite rate cuts and slower growth.

Non-Farm Payrolls (NFP) – Friday

- The marquee report of the week is expected to set the tone for markets heading into October. Any upside surprise in NFP could boost risk appetite in equities and weigh on bond prices, while a softer print might reinforce dovish Fed expectations.

U.S. Unemployment Rate – Friday

- The unemployment rate will be closely tracked to confirm whether labor market strength is holding up. A rise in unemployment could pressure the Fed to consider further easing.

Average Hourly Earnings m/m – Friday

- Wage growth remains a critical factor for inflation and Fed policy. A cooling in earnings would be welcomed by markets as it suggests inflationary pressures from labor costs may be easing.

Last week, markets were quite volatile again, with gold soaring to $3,6065. EUR/USD continued the upward move toward 1.17.80, while main indices closed higher again. The moves weren’t too big though, and we opened 35 trading signals in total, finishing the week with 23 winning signals and 12 losing ones.

Gold Consolidates After the Pullback

Although demand for safe haven assets is still high, gold fell precipitously from record highs following the Fed’s most recent rate decrease as profit-taking was prompted by Powell’s cautious tone. Earlier this week, gold jumped beyond $3,700 and reached $3,707.42 following the Federal Reserve’s announcement of a 25 basis point rate decrease to 4.25%. But the impetus soon waned, and prices dropped back to $3,627, a $80 decline from the new all-time high. As traders locked in profits after the rally driven by dovish predictions, there was a sudden fall but buyers returned on Friday pushing the price $60 higher. Yesterday buyers continued to push and XAU reached another record high at $3,791 before retreating yesterday.

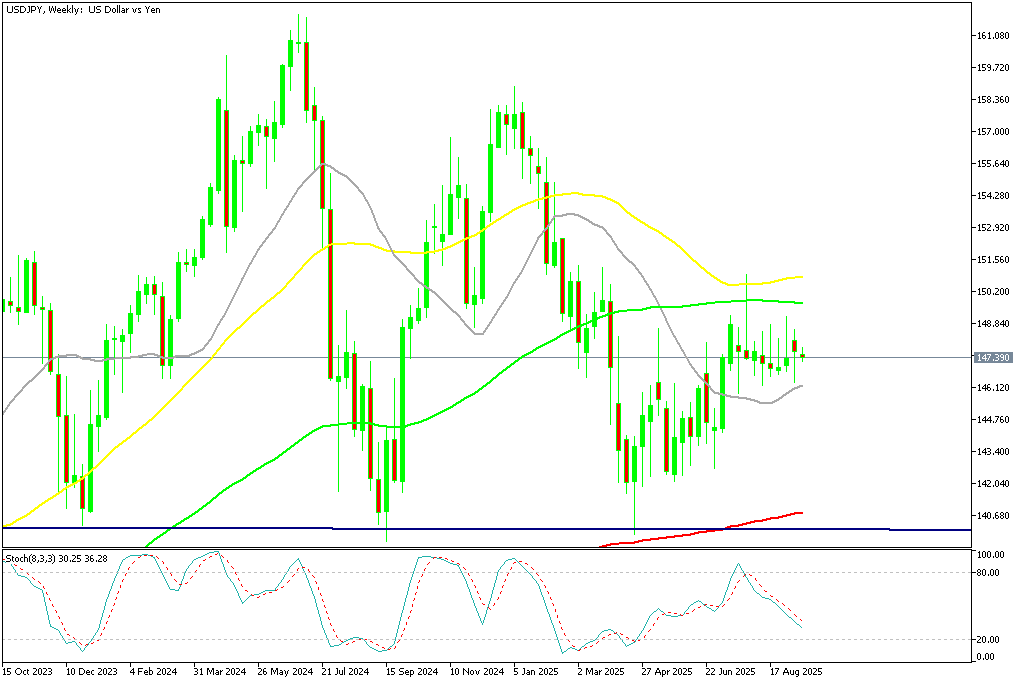

USD/JPY Continues Trading in the Range

Foreign exchange markets saw sharp swings. Early in the week, U.S. yield differentials and Japanese capital outflows pushed the dollar above ¥150, but disappointing U.S. jobs data triggered profit-taking, causing the USD/JPY to slide by four yen from its peak. The move underscored persistent volatility as traders weighed Japan’s intervention risks against evolving Fed expectations.

USD/JPY – Weekly Chart

Cryptocurrency Update

Bitcoin Returns Above $110K

Cryptocurrencies remained highly active over the summer. Bitcoin (BTC) climbed to fresh highs of $123,000 and $124,000 in July and August, supported by institutional inflows and technical strength. However, remarks from Treasury Secretary Scott Bessent ruling out U.S. increases to BTC reserves triggered a steep pullback, sending the coin down to $113,000 before recovering above $116,000 last week, however sellers returned and sent BTC below $110,000, breaking the 20 weekly SMA (gray) as well.

BTC/USD – Weekly chart

Ethereum Returns Above $4,o00 Again

Ethereum (ETH) has been similarly strong, surging toward $4,800, its highest since 2021 and near its all-time peak of $4,860. Despite a dip last week, ETH found support at the 20-day SMA, with retail enthusiasm and renewed institutional participation driving fresh upside momentum. However buying resumed and on Sunday ETH/USD printed another record at $4,941 but we saw a retreat which sent ETH below $4,000 yesterday.

ETH/USD – Daily Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

ABOUT THE AUTHOR

See More

Skerdian Meta

Lead Analyst

Skerdian Meta Lead Analyst.

Skerdian is a professional Forex trader and a market analyst. He has been actively engaged in market analysis for the past 11 years. Before becoming our head analyst, Skerdian served as a trader and market analyst in Saxo Bank's local branch, Aksioner. Skerdian specialized in experimenting with developing models and hands-on trading. Skerdian has a masters degree in finance and investment.

Related Articles

Sidebar rates

Related Posts