Oracle Stock ORCL Breaks $270 Support as Insider Sales, Margin Woes Mount

Due to significant insider selling that has unnerved investors and new skepticism about its growth story, Oracle's momentum has drastically

Quick overview

- Oracle's stock has sharply declined, breaking key support levels amid concerns over growth and insider selling.

- Co-CEO Clay Magouyrk's recent sale of 40,000 shares has raised doubts about internal confidence in the company's future.

- After peaking above $345 in September, Oracle's shares have fallen over 25%, with analysts warning of potential further declines.

- Investor sentiment has shifted to skepticism as rising costs and thin margins challenge Oracle's AI expansion efforts.

Due to significant insider selling that has unnerved investors and new skepticism about its growth story, Oracle’s momentum has drastically slowed, with shares breaking important support levels this week.

Insider Selling Sparks Renewed Uncertainty

Oracle Corporation (NYSE: ORCL) continued its decline on Thursday, weighed down by reports of substantial insider sales. Regulatory filings revealed that newly appointed co-CEO Clay Magouyrk sold 40,000 shares worth roughly $11 million, a move that caught investors off guard. The timing of the sale — just after his promotion — amplified concerns about internal confidence and future growth prospects.

Institutional sentiment also cooled, with Buckhead Capital Management LLC cutting its Oracle holdings by more than 50%, signaling broader caution within the investor base.

Steep Drop from September Highs

After reaching record highs above $345 in early September, Oracle’s shares have now fallen more than 25%, trading below $260 and losing key technical support at the 50-day moving average. On a weekly basis, the stock has slipped under its 20-week SMA, a level that could now act as resistance if weakness continues.

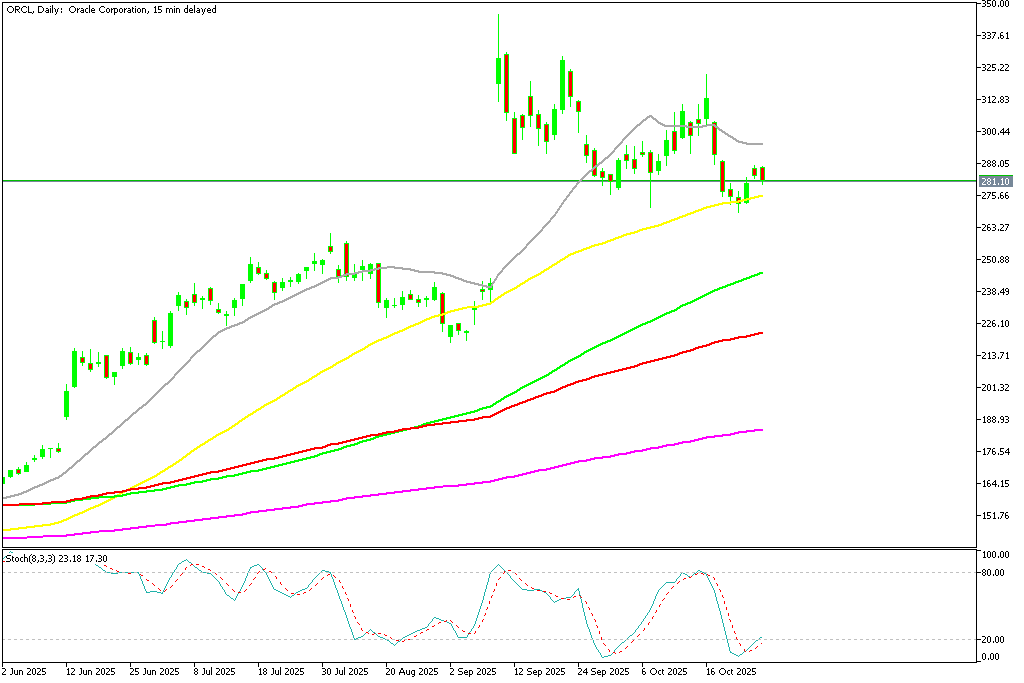

ORCL Chart Daily – Likely the Price Will Fall Below the 50 SMA

Technical analysts warn that if selling pressure persists, the stock could test the $240–$250 range — a zone that would mark a deeper retracement of its recent gains.

AI Profitability Raises Red Flags

Oracle’s earlier rally was powered by optimism around its cloud infrastructure initiatives, but fresh data points to thinner-than-expected margins. The company’s Nvidia-powered cloud segment reportedly generated about $900 million in revenue last quarter, but only $125 million in gross profit, translating to a 14% margin, well below key competitors.

Soaring energy costs and heavy infrastructure spending appear to be eroding profitability. This has led analysts to question whether Oracle’s story is more promotional than performance-driven, especially as peers like Microsoft and Amazon post far stronger returns from similar ventures.

Confidence Weakens as Growth Story Loses Steam

Investor sentiment toward Oracle has shifted from enthusiasm to skepticism. The company’s aggressive AI expansion has yet to show clear financial benefits, and rising costs continue to weigh on margins. Without evidence of sustained profitability or operational efficiency, Oracle risks losing relevance in the fast-evolving AI race.

For now, the narrative around Oracle has turned to profitability doubt, with the market waiting for tangible results to restore confidence.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts