Oracle Stock ORCL Struggles to Recover as Peers Rebound, Signaling More Downside Action

Concerns regarding Oracle's expensive shift to AI and cloud infrastructure are rising as a result of its inability to recoup with the bigger

Quick overview

- Oracle's recent attempts at recovery have failed, raising concerns about its shift toward AI and cloud infrastructure.

- The company's stock has dropped approximately 40% since late September, reflecting waning investor enthusiasm and rising costs.

- Insider selling and deteriorating technical signals further contribute to negative sentiment surrounding Oracle's future performance.

- Intensifying competition in the AI and cloud sectors poses additional challenges, making it difficult for Oracle to maintain relevance.

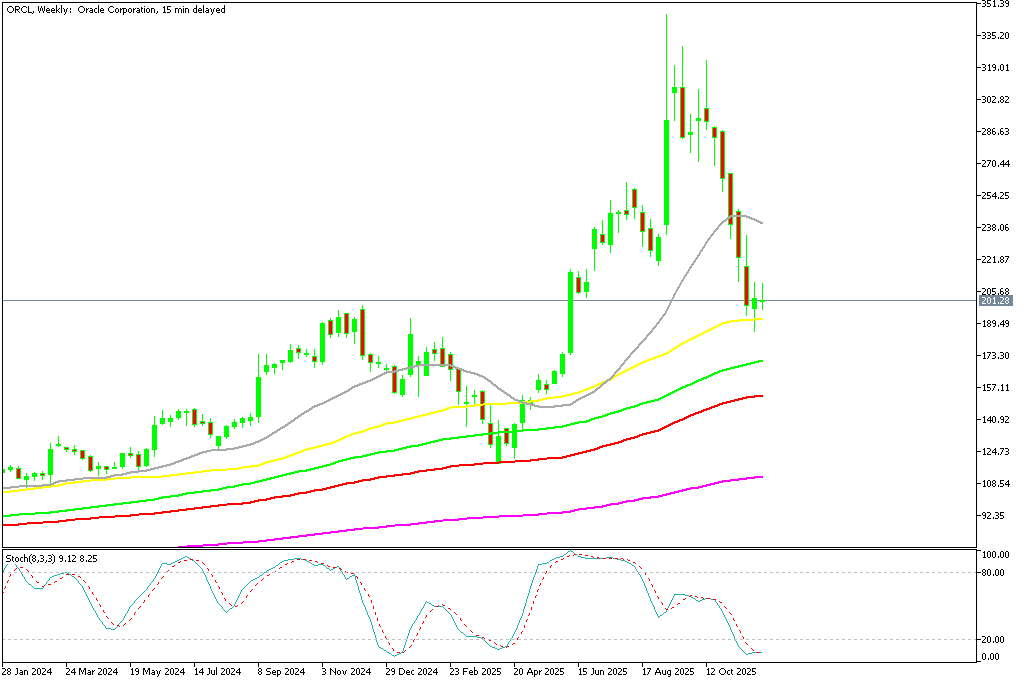

Live ORCL Chart

[[ORCL-graph]]

Concerns regarding Oracle’s expensive shift to AI and cloud infrastructure are rising as a result of its inability to recoup with the bigger market.

Oracle’s Short-Lived Recovery Raises New Concerns

Oracle’s latest attempt at a rebound failed to gain any real traction, deepening worries that the company’s pivot toward artificial intelligence and cloud infrastructure is no longer enough to excite investors. As broader equity markets showed signs of renewed strength, Oracle briefly climbed toward the $210 region—an area buyers had defended in past weeks—but the move quickly fizzled. The stock rolled over once again, sliding back toward the $200 mark, where it now appears vulnerable to a deeper decline.

This lack of follow-through is more than just a technical stumble; it reflects hesitation among investors who are no longer convinced that Oracle’s growth strategy can deliver near-term rewards. With buyers stepping aside and sellers exerting stronger pressure, the path of least resistance remains tilted to the downside.

What began in mid-October as a seemingly normal consolidation has gradually transformed into a steady, grinding downtrend. Even when broader risk appetite improves, Oracle continues to underperform—a pattern that reveals a deeper erosion of sentiment surrounding the stock.

From Market Favorite to Faltering Performer

Earlier this year, Oracle enjoyed a period of strong optimism. The company was viewed as a major beneficiary of the accelerating shift toward cloud computing and AI-driven enterprise workloads. Positive commentary on its AI infrastructure, new application features, and a widely discussed (though highly speculative) $300 billion cloud deal linked to OpenAI fueled a powerful rally. This push culminated in record highs above $340, driven by the belief that Oracle was on the cusp of becoming a more formidable player in the cloud arms race.

But much of that optimism has faded. Since late September, Oracle’s share price has given up roughly 40% of its value. Each recovery attempt has been brief and shallow, immediately met with renewed selling pressure. The message being sent by the market is unmistakable: enthusiasm has cooled, and investors are no longer willing to overlook the company’s rising costs, leverage, and slower-than-expected margin improvements.

OpenAI Deal

Oracle’s balance sheet has become another point of concern. With debt levels already elevated, the company raised an additional $18 billion earlier this year to support the buildout of its massive AI-focused data center expansion. Reports now suggest Oracle is exploring another $38 billion in financing in collaboration with Vantage Data Centers to support its commitments tied to OpenAI.

While these investments may hold long-term merit, the near-term burden is heavy—and investors are increasingly sensitive to companies stretching their balance sheets for future growth narratives.

Insider Activity Adds Another Layer of Uncertainty

Adding to the challenges is a rise in insider selling. Although insider transactions do not always indicate trouble, their timing matters. Seeing increased insider selling at a moment when the stock is struggling has raised doubts about internal confidence in the company’s short-term trajectory. In a market already cautious about valuation and capital spending excesses, these signals can amplify negative sentiment.

For investors seeking stability, insider behavior acts as a subtle sentiment gauge—and right now, the reading is not especially reassuring.

Technical Signals Point Toward Continued Weakness

From a technical perspective, Oracle’s chart has deteriorated meaningfully. The stock has fallen below key weekly moving averages, including the 20-week SMA, while the 50-week SMA is acting as the next layer of support. Unlike many other large-cap tech names that bounced sharply during recent market strength, Oracle has shown no such resilience.

ORCL Chart Weekly – Sellers Test the 50 SMA

Market attention is now centered on the $190 zone, a level that aligns with longer-term support. Should this break, it may expose the stock to a more pronounced decline toward historical consolidation regions between $120 and $140. While this is not a guaranteed path, the growing weakness in price structure makes such a scenario more plausible than it appeared a few months ago.

AI and Cloud Announcements No Longer Spark Buying Interest

Despite Oracle’s continued rollout of AI-related initiatives—including sovereign cloud offerings, government partnerships, and new infrastructure support for high-security workloads—the market response remains muted.

Announcements that once triggered excitement now barely move the stock. Investors appear fatigued with forward-looking promises and are increasingly prioritizing:

- measurable revenue leverage

- sustainable profit margins

- operational efficiency

- and clear competitive advantages

Without these, even dramatic AI headlines are falling flat.

Rising Costs Threaten Long-Term Margins

A major question looming over Oracle is whether its aggressive expansion strategy is financially sustainable. AI and cloud infrastructure require billions in upfront investment: data centers, high-performance GPUs, advanced networking, and massive energy consumption.

While Oracle’s cloud revenue is growing, the associated costs are climbing as well, keeping pressure on margins. Compared with cloud leaders who already benefit from scale—such as Amazon, Microsoft, and Google—Oracle’s profitability profile appears increasingly strained.

This structural disadvantage continues to feed skepticism about whether Oracle can compete effectively while simultaneously managing its debt load.

Competitive Pressures Are Intensifying

The broader AI ecosystem is becoming more competitive, not less. Major players continue to roll out new products, lock in contracts, and scale faster than ever. Nvidia dominates AI hardware. Microsoft and Amazon command the largest cloud platforms. Even enterprise software rivals are pushing deeper into AI-enabled workflows.

Against this backdrop, Oracle’s slowdown becomes harder to ignore—and investors are beginning to reassess whether the company can maintain relevance in the face of such fierce competition.

Outlook: Downside Risk Still Dominant

The ingredients for continued pressure are still present: weakening technical structure, heavy capital demands, rising debt, fading enthusiasm for AI-themed speculation, and increasingly aggressive competitors.

Unless Oracle delivers clearer proof of sustainable growth and improved operational execution, investor skepticism is likely to remain elevated.

For the moment, the bias remains tilted to the downside—making Oracle a stock that the market is still unwilling to reward, even as other tech names regain their footing.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts