Nvidia Stock NVDA Enters a Riskier Phase as Chip Tariff Threats, Margins and Valuation Pull

Nvidia remains the undisputed leader in artificial intelligence hardware, but insider selling, export uncertainty, and shifting market expec

Quick overview

- Nvidia's stock has faced a nearly 4% decline as investors reassess risks, including insider selling and export uncertainties.

- Concerns over Nvidia's relationship with China have intensified due to new regulatory requirements for AI chip exports.

- Insider selling and restrictive sales terms signal a cautious market sentiment, emphasizing the fragility of Nvidia's current position.

- Despite strong fundamentals, Nvidia's elevated expectations and geopolitical tensions have led to increased scrutiny and a shift in investor confidence.

Nvidia remains the undisputed leader in artificial intelligence hardware, but insider selling, export uncertainty, and shifting market expectations are making investors far less forgiving.

A Cautious Start for a Market Darling

Nvidia has entered the new year on the defensive, marking a notable change in how investors are treating one of the most dominant stocks of the AI era. Shares slid nearly 4% in U.S. trading, falling below the $180 level, as markets reassessed a growing cluster of risks surrounding the company.

This move was not simple profit-taking. Instead, it reflected a broader shift in sentiment following Nvidia’s extraordinary multi-year run. The stock’s leadership position in AI remains unquestioned, but markets are now asking harder questions about sustainability, valuation, and exposure to forces outside Nvidia’s control.

For a company that once seemed immune to pullbacks, the tone has clearly changed.

China Exposure Remains the Central Uncertainty

At the heart of investor unease is Nvidia’s relationship with China. Recent regulatory developments offered a measure of relief, but they stopped well short of providing clarity.

The U.S. Commerce Department confirmed that exports of Nvidia’s H200 AI chips to China may proceed, but only under stricter oversight. Each shipment must now be reviewed by an independent testing laboratory to ensure compliance with U.S. restrictions on AI capability.

While this is preferable to an outright ban, it introduces new friction. Approval delays, testing bottlenecks, and uncertainty around shipment volumes all complicate revenue visibility. For investors, this is not a clean reopening of a critical market—it is conditional access with strings attached.

Logistics and Enforcement Still Pose Real Risks

Concerns intensified after reports emerged that Chinese customs authorities had delayed deliveries of Nvidia’s H200 chips. According to industry sources, some suppliers paused production after shipments were held up at regional ports, underscoring a key reality: even when exports are technically permitted, enforcement and logistics can still disrupt sales.

The episode sent shockwaves through chip and technology stocks, highlighting how sensitive the AI hardware trade has become to incremental headlines. Demand may be strong, but revenue only materializes once chips clear inspections, arrive on time, and are installed.

In this environment, investors are increasingly focused not just on demand, but on execution timing.

Restrictive Sales Terms Signal Fragility

Further highlighting the uncertainty, Nvidia has reportedly required Chinese customers to pay fully upfront for H200 orders. These purchases are said to be non-refundable, non-cancelable, and not subject to reconfiguration.

From Nvidia’s perspective, such terms limit financial exposure in the event of sudden policy changes. From the market’s perspective, they serve as a reminder that regulatory stability is far from guaranteed.

If approvals were truly secure, such restrictive conditions might be unnecessary. Their existence reinforces the idea that Nvidia is operating in a narrow corridor of conditional acceptance rather than a stable export framework.

Geopolitical Tension Adds Another Layer of Risk

Adding to the unease are renewed geopolitical concerns, including trade rhetoric from President Trump tied to disputes involving Greenland and broader tariff threats. While Nvidia is not directly targeted, the headlines contribute to an environment where policy risk is once again front and centre.

Markets are increasingly sensitive to any suggestion that trade relations could deteriorate further. For Nvidia, which relies on global supply chains and international customers, even indirect geopolitical escalation can weigh on sentiment.

Valuation Sensitivity Begins to Show

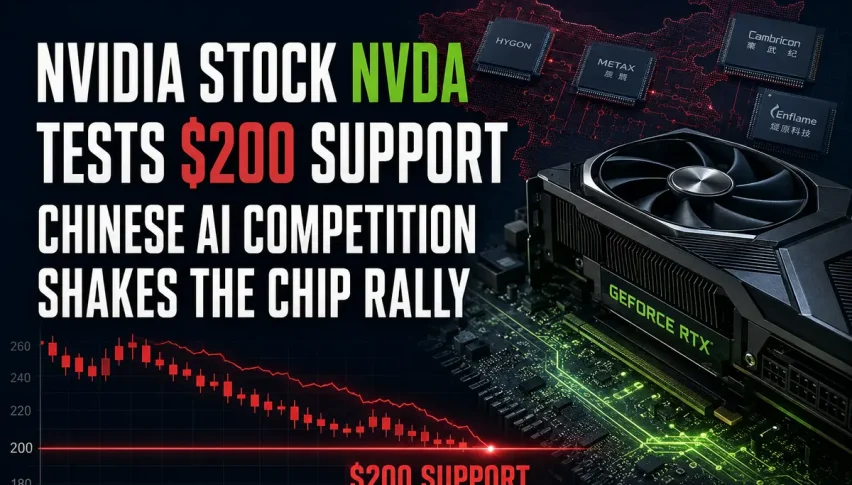

Nvidia’s recent underperformance relative to other mega-cap technology stocks is notable not because fundamentals have weakened, but because expectations were extraordinarily high. The stock’s repeated failure to reclaim the $200 level has taken on psychological importance.

Each rejection reinforces the perception that near-term upside may be capped unless Nvidia delivers fresh upside surprises. Investors are no longer debating Nvidia’s dominance; they are debating how much of that dominance is already reflected in the share price.

In this phase, even good news must clear a higher bar.

CES Commentary Highlights Market Sensitivity

Nvidia’s influence over the broader AI ecosystem was once again evident following CEO Jensen Huang’s comments at CES. Huang noted that next-generation Nvidia chips are now in full production and suggested that future designs could significantly reduce data-center cooling requirements.

Those remarks triggered sharp declines in cooling and thermal-management stocks, illustrating how Nvidia’s messaging can instantly reshape expectations across entire supply chains.

For Nvidia itself, the episode highlighted a growing challenge: every statement is now scrutinized for its implications on margins, industry economics, and future demand—not just for Nvidia, but for everyone around it.

Insider Selling Adds to the Cautious Tone

Investor confidence took another modest hit after a Form 144 filing revealed that Nvidia officer Donald F. Robertson Jr. plans to sell up to 80,000 shares, valued at roughly $15 million.

While insider sales are common and often unrelated to company outlook, timing matters. When a stock trades at premium valuations and momentum is fading, such disclosures can reinforce perceptions that near-term upside may be limited.

The sale did not drive the stock lower on its own, but it added to an already cautious narrative.

Technical Picture Reflects Waning Momentum

Nvidia’s technical setup mirrors the shifting sentiment. The stock has slipped below its 20-week simple moving average (gray), a level that previously provided reliable support. That average has now turned into resistance, rejecting recent rebound attempts.

NVDA Chart Weekly – The 20 SMA Has Turned Into Resistance

Momentum indicators have weakened, and market participants are increasingly discussing the possibility of a deeper pullback toward the 50-week moving average (yellow). While the long-term uptrend remains intact, short-term control has shifted toward sellers.

Fundamentals Remain Exceptional—but Expectations Are Higher

From a business standpoint, Nvidia remains a powerhouse. The company recently reported quarterly revenue of $39.3 billion, far exceeding expectations, reaffirming its central role in the AI boom.

However, the market reaction was muted after management guided toward shrinking gross margins. Investors interpreted this as a sign that the AI “gold rush” phase—characterized by effortless margin expansion—may be giving way to a more capital-intensive reality.

In today’s environment, strong results are assumed. The question is whether Nvidia can continue to exceed already-elevated expectations.

Strategic Expansion Brings Opportunity and Risk

Nvidia’s ambition continues to expand. Its partnership with Brookfield Asset Management to develop up to $100 billion in AI infrastructure signals a push deeper into the value chain.

Strategically, the move makes sense. Financially, it introduces execution risk, capital intensity, and longer payback periods—factors that complicate the investment case just as markets grow less tolerant of uncertainty.

For a company historically prized for its asset-light model, this evolution represents a meaningful shift.

Conclusion: Leadership Remains, but the Margin for Error Shrinks

Nvidia remains the linchpin of the global AI ecosystem, but its early-2026 performance reflects a market that is no longer willing to overlook risk. Regulatory ambiguity, geopolitical tension, insider activity, and premium valuation have combined to create a more demanding environment.

Conditional export relief offers some support, but confidence will only stabilize when policy clarity improves and execution risks diminish. Nvidia’s crown is still firmly in place—but the tolerance for missteps has narrowed significantly.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts