Google Stock GOOGL Faces Third Weekly Declines After Record Highs – Can $240 Hold?

Alphabet's stock is exhibiting its first symptoms of exhaustion following a six-month rise that sent the tech giant to all-time highs as...

Quick overview

- Alphabet's stock is experiencing its first signs of fatigue after a six-month rally, marking three consecutive weekly declines.

- The company is launching Gemini Enterprise, a subscription-based AI service aimed at expanding its enterprise market presence, although initial investor reactions have been cautious.

- A favorable court ruling in an antitrust case has eased regulatory pressures on Alphabet, boosting investor confidence and contributing to its previous stock highs.

- Despite recent stock pullbacks, Alphabet's strong earnings and strategic positioning in AI and cloud services suggest a solid long-term growth outlook.

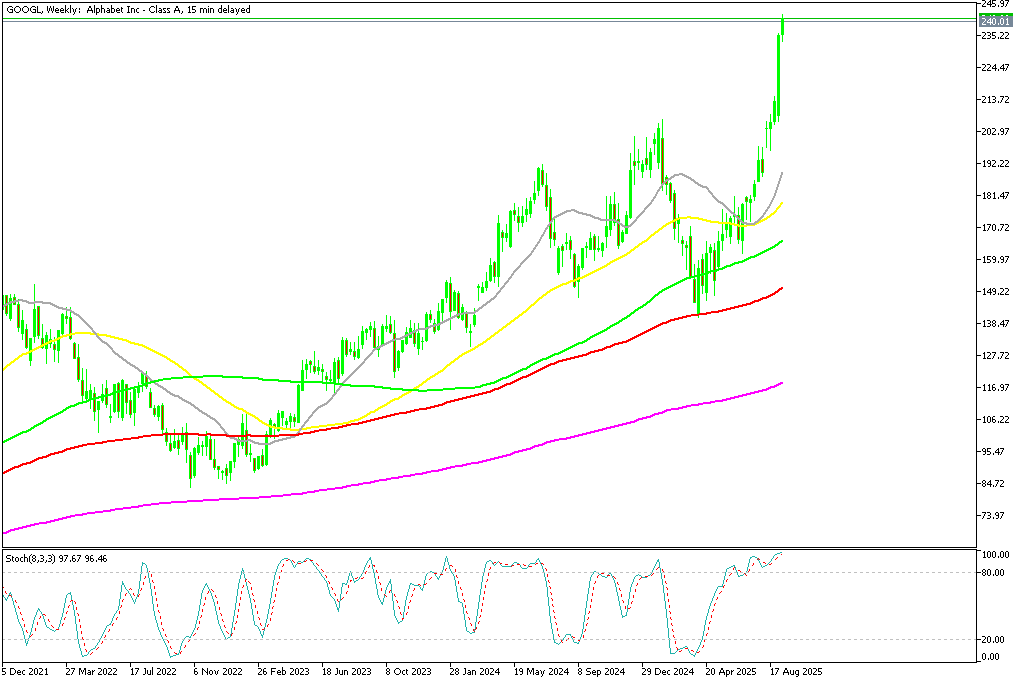

Live GOOGL Chart

[[GOOGL-graph]]

Alphabet’s stock is exhibiting its first symptoms of exhaustion following a six-month rise that sent the tech giant to all-time highs as investors reevaluate momentum and valuation.

Alphabet’s Rally Loses Steam

Alphabet (NASDAQ: GOOGL) appears set to close the week lower, marking its third straight weekly decline after hitting all-time highs by mid-September. The stock’s exceptional rise had been fueled by Apple’s struggles in the smartphone market, a favorable antitrust ruling, and strong quarterly earnings that reinforced investor optimism.

GOOGL Chart Daily – The Uptrend Is Picking Up Pace

Over the past six months, Alphabet shares surged from $140 in April to $256 in September, delivering one of the most powerful rallies among mega-cap tech stocks this year. However, the pace has since slowed. By Thursday evening, shares traded near $240, as investors began to lock in profits and evaluate whether the stock’s next move is consolidation—or correction.

New Subscription Model Aims at Enterprise Expansion

Alphabet is doubling down on artificial intelligence with the launch of Gemini Enterprise, a subscription-based service that allows businesses to build and deploy custom AI agents.

Priced at $30 per user per month—plus an additional $21 monthly fee for small businesses—the offering signals Google’s ambition to strengthen its foothold in the AI productivity market. However, the stock slipped in early trading following the announcement, suggesting that investors may want to see clearer monetization potential before rewarding the move.

The enterprise-focused expansion reflects Alphabet’s strategy to turn its AI breakthroughs into consistent, scalable revenue streams while fending off competition from Microsoft’s Copilot and OpenAI-powered integrations.

Legal Victory Eases Regulatory Pressure

Alphabet also found relief in a favorable court ruling stemming from the U.S. government’s high-profile antitrust case. Judge Amit Mehta delivered a balanced decision that requires Google to share some search data and curb exclusive search deals, but crucially, stopped short of imposing major structural penalties.

The verdict was interpreted as a net positive for the company, reducing uncertainty around future regulatory constraints while preserving Google’s dominant position in search and advertising. This outcome lifted investor confidence earlier in September and was a major catalyst behind Alphabet’s previous run to record highs.

Apple’s Weakness Becomes Google’s Advantage

Apple’s underwhelming iPhone 17 launch provided Alphabet with an unexpected boost. The missteps in Apple’s smartphone division opened the door for Pixel’s rapid expansion, with global Pixel sales doubling between early 2024 and mid-2025.

Alphabet’s Pixel 9 series has been a standout performer, helping the company capture incremental market share, particularly in the U.S. and select European regions. Analysts point out that Apple’s stumbles have also benefited Samsung and Chinese rivals such as Xiaomi and Huawei, but Google’s integration of AI-driven features within its hardware has kept it ahead in innovation appeal.

Earnings Strength Reinforces Long-Term Confidence

Alphabet’s second-quarter 2025 results reinforced investor faith in the company’s resilience. Adjusted EPS came in at $2.31, comfortably beating expectations, while revenue excluding traffic acquisition costs rose to $81.2 billion.

Google Cloud remained a standout performer with $13.6 billion in sales, signaling sustained enterprise adoption of cloud-based infrastructure. Meanwhile, YouTube’s ad revenue surged 13% year-over-year to $9.8 billion, underscoring Alphabet’s continued dominance in digital advertising even as competition intensifies from TikTok and streaming rivals.

The results painted a picture of a tech powerhouse firing on multiple cylinders—cloud, advertising, and AI—while managing to expand margins despite a softer digital ad environment.

Outlook: Can Alphabet Break Above $250 Again?

Despite short-term weakness, Alphabet’s outlook remains fundamentally strong. The company has navigated regulatory challenges, broadened its AI monetization strategy, and leveraged competitors’ missteps—all of which create a foundation for continued growth.

However, the stock’s recent pullback underscores a market rotation from momentum to valuation discipline, as investors assess whether the multi-month rally has outpaced earnings potential.

If Alphabet can hold support near $235–$240 and sustain revenue growth through year-end, a renewed breakout above $250 could set the stage for a fresh leg higher in 2026.

Conclusion: Alphabet’s short-term retreat may simply be a healthy pause after an extraordinary rally. With legal clarity, strong fundamentals, and a growing AI footprint, the company’s long-term trajectory remains firmly upward—even as markets catch their breath.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM