btc-usd

Forex Signals Oct 24: P&G, NatWest, and Sanofi Earnings, But US CPI Inflation Headlines

Today we have the US CPI inflation despite the shut down, while investors will watch P&G, Sanofi and NatWest Q3 earnings reports.

•

Last updated: Friday, October 24, 2025

Quick overview

- The U.S. dollar weakened as risk appetite increased, leading to gains in global markets and equities.

- U.S. Treasury yields rose, indicating renewed caution over inflation and rate expectations.

- Gold and crude oil prices surged, supported by a weaker dollar and geopolitical tensions.

- Investors are focused on upcoming economic reports, including U.S. CPI and earnings from Procter & Gamble, Sanofi, and NatWest.

Live BTC/USD Chart

BTC/USD

0.0000

MARKETS TREND

Today we have the US CPI inflation despite the shut down, while investors will watch P&G, Sanofi and NatWest Q3 earnings reports.

Dollar Slips as Risk Appetite Lifts Global Markets

The U.S. dollar traded mostly lower on Thursday, with the sharpest losses seen against the Australian dollar. Risk-on sentiment dominated the session, reversing the greenback’s earlier strength as investors rotated toward higher-yielding and growth-oriented assets.

Equities Climb on Optimism and Quantum Stock Surge

U.S. stocks extended their gains as optimism spread across markets. The Dow Jones Industrial Average advanced 0.31%, the S&P 500 gained 0.58%, and the Nasdaq Composite rose 0.89%, while the Russell 2000 outperformed with a 1.27% jump.

The rally was partly driven by renewed enthusiasm for quantum computing stocks, which soared following rumors of potential government investment in the sector. Despite a later White House denial, sentiment remained upbeat, and the sector held onto most of its gains.

Bond Yields Edge Higher

U.S. Treasury yields ticked higher across the curve, with the 10-year yield climbing back above 4.00%, signaling renewed caution over inflation and rate expectations.

- The 2-year yield rose 4.7 basis points to 3.490%.

- The 5-year yield gained 5.4 basis points to 3.609%.

- The 10-year yield increased 5.0 basis points to 4.002%.

Commodities and Crypto Push Higher

Gold climbed $27 (0.66%) to $4,125, supported by a weaker dollar and persistent geopolitical tensions. Meanwhile, crude oil jumped $3.27 to $61.71, after reports surfaced of new measures targeting Russian energy firms.

Bitcoin also joined the risk-on rally, advancing roughly $2,000 on the day to trade near $109,553, as traders embraced broader market optimism.

Key Market Events to Watch Today:

Investors turn their focus to a busy Friday calendar featuring major economic updates from the UK, Eurozone, and US.

UK Retail Sales: Flat Growth Expected

UK retail sales are anticipated to remain unchanged in September after a 0.5% rise in August, signaling consumer restraint amid rising living costs and pre-Budget caution.

The latest BRC retail report showed annual growth slowing to 2.0% from 2.9%, with mild weather curbing seasonal clothing demand and most food sales driven by inflation rather than real volume growth.

Eurozone Flash PMI: Modest Improvement Seen

The Eurozone’s October flash PMIs are expected to show little change, with manufacturing forecast at 49.9, services at 51.1, and the composite at 51.0.

While sentiment has improved slightly—supported by better-than-expected ZEW and Sentix readings—overall growth remains fragile. Economists will watch closely for any signs of stronger new orders or a sustained rebound in business activity after months of sluggish expansion.

UK Flash PMI: Signs of Stabilization

Analysts expect the UK services PMI to hold steady at 50.8, following a sharp drop in the prior month. Earlier surveys showed businesses delaying spending decisions until after the Autumn Budget, while consumers stayed cautious about large purchases.

Investec forecasts a modest recovery in manufacturing output, driven by restocking after recent inventory drawdowns.

US CPI: All Eyes on Inflation Data

The September CPI report—delayed by the government shutdown—will be released today at 8:30 a.m. ET after the BLS recalled staff to finalize it. Economists expect headline inflation to rise 0.3% month-on-month (prev. 0.4%) and core CPI to climb 0.3% (unchanged).

The data will be key for the Federal Reserve’s October 29 meeting, as policymakers weigh whether disinflation progress is holding amid firm wage and housing costs.

US Flash Manufacturing PMI: Gauging Factory Momentum

The US flash manufacturing PMI will offer a real-time look at industrial activity during the government shutdown.

Regional data has been mixed, with the New York Fed index rebounding strongly to 10.7 from -8.7, while other regions show patchy improvement. Markets will look for signs of demand resilience and pricing pressure ahead of the next ISM report on November 3.

Procter & Gamble (PG) – Q1 FY2026 Earnings (Before Market Open)

- EPS Estimate: $1.90

- Focus: Analysts expect steady performance supported by resilient demand in home and personal care categories.

Key Watchpoints:

- Volume growth amid moderating inflation pressures.

- Margin trends as input costs stabilize.

- Guidance for FY2026, especially around consumer spending patterns in emerging markets.

💊 Sanofi (SNY) – Q3 FY2025 Earnings (Before Market Open)

- EPS Estimate: $1.58

- Focus: Investors will look for clarity on the company’s pharmaceutical pipeline and vaccine segment performance.

Key Watchpoints:

- Growth in the Dupixent franchise and other specialty care drugs.

- Progress on restructuring initiatives aimed at improving profitability.

- Updates on R&D spending and regulatory milestones.

NatWest Group (NWG) – Q3 FY2025 Earnings (Before Market Open)

- EPS Estimate: $0.43

- Focus: UK banking results are expected to highlight the effects of moderating interest margins and rising credit provisions.

Key Watchpoints:

- Net interest income trends amid potential Bank of England rate cuts in early 2026.

- Loan growth and deposit trends as consumer borrowing slows.

- Progress on capital returns or share buybacks.

The 20 SMA Holds the Gold Dip

Although demand for safe haven assets is still high, gold fell precipitously from record highs following the Fed’s most recent rate decrease as profit-taking was prompted by Powell’s cautious tone. Earlier this week, gold jumped beyond $3,700 and reached $3,707.42 following the Federal Reserve’s announcement of a 25 basis point rate decrease to 4.25%. But the impetus soon waned, and prices dropped back to $3,627, a $80 decline from the new all-time high. As traders locked in profits after the rally driven by dovish predictions, there was a sudden fall but buyers returned on Friday pushing the price $60 higher. Yesterday buyers continued to push and XAU reached another record high at $4,381 but we saw a $375 crash to $4,004 yesterday, so the volatility is increasing. But the 20 daily SMA held as support.

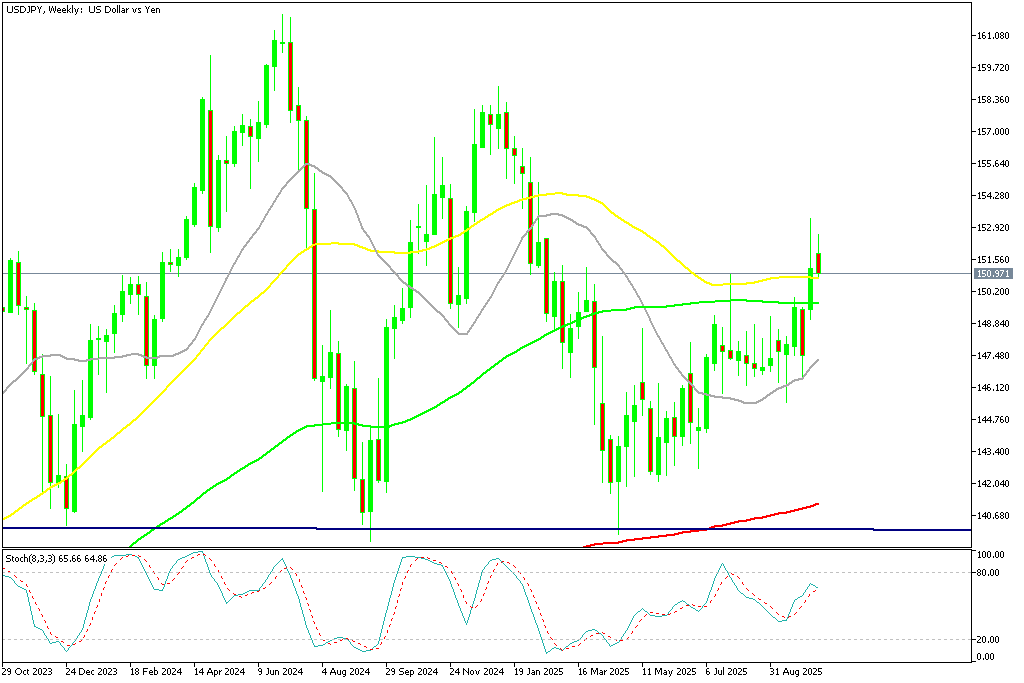

USD/JPY Returns to 150

Foreign exchange markets saw sharp swings. Early in the week, U.S. yield differentials and Japanese capital outflows pushed the dollar above ¥150, but disappointing U.S. jobs data triggered profit-taking, causing the USD/JPY to slide by four yen from its peak. However, the new BOJ governor the JPY has weakened and USD/JPY soared to 153 but returned below 152 yesterday.

USD/JPY – Weekly Chart

Cryptocurrency Update

Bitcoin Retests the Support Indicator

Cryptocurrencies remained highly active over the summer. Bitcoin (BTC) climbed to fresh highs of $123,000 and $124,000 in July and August, supported by institutional inflows and technical strength. However, remarks from Treasury Secretary Scott Bessent ruling out U.S. increases to BTC reserves triggered a steep pullback, sending the coin down below $105,000 before finding support at the 200 daily SMA (purple) and recovering above $115,000 but then fell toward $100K again. However this week BTC has turned higher again, climbing above $111K.

BTC/USD – Daily chart

Ethereum Falls Below $4,000

Ethereum (ETH) has been similarly strong, surging toward $4,800, its highest since 2021 and near its all-time peak of $4,860. Despite a dip last week, ETH found support at the 20-day SMA, with retail enthusiasm and renewed institutional participation driving fresh upside momentum. ON Friday we saw a dive below $3.500 however buying resumed on Sunday and ETH/USD climbed above $4,500 but returned back down below $4,000 again this week.

ETH/USD – Weekly Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

ABOUT THE AUTHOR

See More

Skerdian Meta

Lead Analyst

Skerdian Meta Lead Analyst.

Skerdian is a professional Forex trader and a market analyst. He has been actively engaged in market analysis for the past 11 years. Before becoming our head analyst, Skerdian served as a trader and market analyst in Saxo Bank's local branch, Aksioner. Skerdian specialized in experimenting with developing models and hands-on trading. Skerdian has a masters degree in finance and investment.

Related Articles

Sidebar rates

Related Posts