Forex Signals Oct 30: The BoJ and ECB Steady, Trump Meets Xi; Apple, Amazon, Eli Lilly Q3

Along with the ECB, BOJ, and Trump-Xi summits, today's earnings are dominated by major market players Apple, Amazon, and Eli Lilly.

•

Last updated: Thursday, October 30, 2025

Quick overview

- Major earnings reports from Apple, Amazon, and Eli Lilly are anticipated to influence market sentiment this week.

- Federal Reserve Chair Jerome Powell indicated that rate cuts will not be continuous, with future decisions dependent on economic data.

- The Bank of Canada also cut rates, citing challenges from rising U.S. tariffs and weak global demand.

- U.S. pending home sales were flat in September, reflecting ongoing concerns about job stability and high inventory levels.

Along with the ECB, BOJ, and Trump-Xi summits, today’s earnings are dominated by major market players Apple, Amazon, and Eli Lilly.

Powell Warns Cuts Won’t Be Continuous

The Fed trimmed rates by 0.25%, with Chair Jerome Powell describing it as a “risk management move”, not the start of a steady easing cycle.

He stressed that a December cut isn’t assured, saying the decision will depend on upcoming data. Inflation remains above target, though disinflation in services is ongoing.

Powell noted tariffs are adding mild price pressure, but their impact should fade. The labor market is softening gradually, and AI-driven investment continues to support modest growth near 1.6%.

Bank of Canada Turns Cautious Too

The BoC also cut rates by 25 bps to 3.75%–4.00%, marking a tentative shift toward support. Governor Tiff Macklem said policy is now at the low end of neutral, but warned that further cuts aren’t planned soon.

Rising U.S. tariffs and weak global demand pose new challenges for Canada’s exporters, prompting a wait-and-see approach before any additional easing.

Markets, Housing, and Yields React

U.S. pending home sales were flat in September, missing forecasts despite lower mortgage rates. Confidence remains weak amid job worries and high inventory.

Stocks were mixed:

- Dow -0.16%

- S&P 500 flat

- NASDAQ +0.55%

Post-close: Alphabet +5.5%, Meta -9%, Microsoft -2.3%. Yields jumped, with the 10-year up to 4.08%, reflecting doubts about another near-term cut. Oil rose 0.3% to $60.38 after a major inventory draw, while gold reversed lower to $3,944 after failing to hold above $4,000.

Key Market Events to Watch Today: Central Banks and Big Tech in Focus

Today’s results will set the tone for late-week market sentiment. Strong reports from Apple and Amazon could reinforce the tech sector’s resilience, while Eli Lilly’s update will be key for gauging momentum in the healthcare space.

Trump–Xi Meeting: A Cautious Reset

U.S. President Donald Trump and China’s Xi Jinping will meet on October 30 at the APEC Summit in South Korea, aiming to ease trade tensions and revive talks on rare earths, soybeans, technology, and Taiwan.

Analysts expect limited progress, as both sides seek stability without major concessions. The meeting comes ahead of a November 10 trade truce expiry, with the U.S. preparing a Section 301 probe that could trigger new tariffs in early November.

BoJ: No Rush to Hike

The Bank of Japan is set to hold rates at 0.50%, despite hints it’s nearing a tightening move. Officials see no urgency, especially amid political changes after PM Takaichi’s rise following coalition shifts.

The BoJ continues ETF and J-REIT sales, signaling gradual normalization while avoiding disruption.

ECB: Staying on Pause

The European Central Bank will likely keep policy unchanged in October, holding the Deposit Rate at 2.00%.

Inflation forecasts for 2026 were nudged to 1.7%, prompting a cautious tone from Christine Lagarde, who sees balanced risks and expects a reassessment in December.

Earnings Watch: Big Tech and Pharma in Focus

Apple Inc. (AAPL)

- Quarter: Q4 2025

- Report Time: After Market Close (AMC)

- EPS Estimate: $1.77

- Focus: Investors will be watching iPhone 16 and Mac sales trends, along with updates on the Vision Pro rollout.

- Context: Apple shares have outperformed peers this quarter, but analysts warn that slowing services growth or weaker China demand could weigh on sentiment.

Amazon.com, Inc. (AMZN)

- Quarter: Q3 2025

- Report Time: After Market Close (AMC)

- EPS Estimate: $1.56

- Focus: AWS cloud margins, Prime membership growth, and holiday season outlook.

- Context: Recent retail strength and logistics efficiency could support results, but higher fulfillment costs may pressure operating income.

Eli Lilly & Co. (LLY)

- Quarter: Q3 2025

- Report Time: Before Market Open (BMO)

- EPS Estimate: $5.89

- Focus: Sales of weight-loss drug Mounjaro and diabetes treatment pipeline progress.

- Context: The pharma giant’s valuation remains stretched, and investors are keen to see whether strong demand can offset rising R&D expenses.

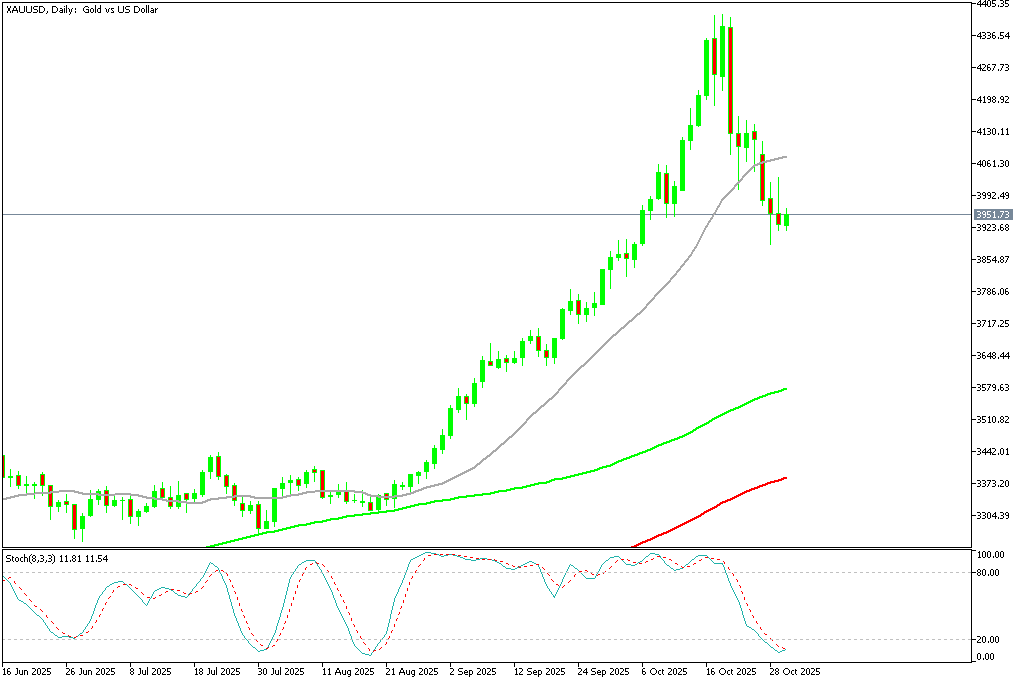

Gold Buyers Start to Fight Back

Although demand for safe haven assets is still high, gold fell precipitously from record highs following the Fed’s most recent rate cut comments, as profit-taking was prompted by Powell’s cautious tone. Earlier this month, gold jumped above $4.3800 following the Federal Reserve’s announcement of a 25 basis point rate decrease. But the impetus soon waned, and prices dropped back to $4,004. The 20 daily SMA (gray) held as support last week, but it gave way yesterday as sellers pushed Gold below $3,900.

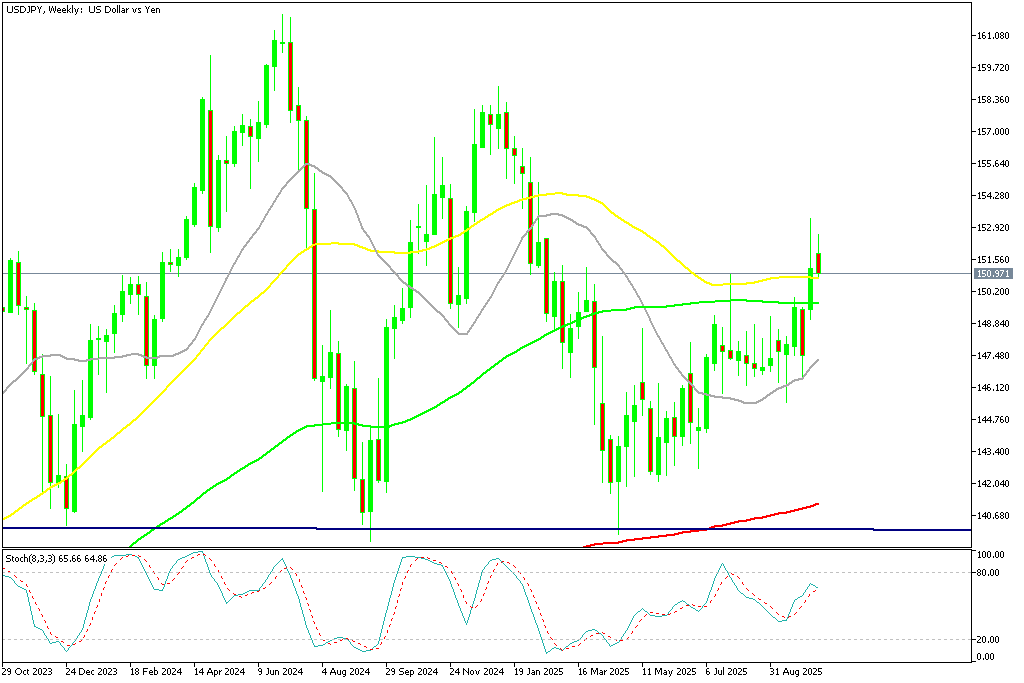

USD/JPY Returns to 150

Foreign exchange markets saw sharp swings. Early in the week, U.S. yield differentials and Japanese capital outflows pushed the dollar above ¥150, but disappointing U.S. jobs data triggered profit-taking, causing the USD/JPY to slide by four yen from its peak. However, the new BOJ governor the JPY has weakened and USD/JPY soared to 153 but returned below 152 yesterday.

USD/JPY – Weekly Chart

Cryptocurrency Update

Bitcoin Fails at Resistance

Cryptocurrencies remained highly active over the summer. Bitcoin (BTC) climbed to fresh highs of $123,000 and $124,000 in July and August, supported by institutional inflows and technical strength. However, remarks from Treasury Secretary Scott Bessent ruling out U.S. increases to BTC reserves triggered a steep pullback, sending the coin down below $105,000 before finding support at the 200 daily SMA (purple) and recovering above $115,000 but then fell toward $100K again. However last week BTC has turned higher again, climbing above $114K over the weekend.

BTC/USD – Daily chart

Ethereum Stays close to $4,000

Ethereum (ETH) has been similarly strong, surging toward $4,800, its highest since 2021 and near its all-time peak of $4,860. Despite a dip last week, ETH found support at the 20-day SMA, with retail enthusiasm and renewed institutional participation driving fresh upside momentum. ON Friday we saw a dive below $3.500 however buying resumed on Sunday and ETH/USD climbed above $4,500 but returned back down below $4,000 again this week.

ETH/USD – Daily Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

ABOUT THE AUTHOR

See More

Skerdian Meta

Lead Analyst

Skerdian Meta Lead Analyst.

Skerdian is a professional Forex trader and a market analyst. He has been actively engaged in market analysis for the past 11 years. Before becoming our head analyst, Skerdian served as a trader and market analyst in Saxo Bank's local branch, Aksioner. Skerdian specialized in experimenting with developing models and hands-on trading. Skerdian has a masters degree in finance and investment.

Related Articles

9 hours ago

Save

9 hours ago

Save

Sidebar rates

Related Posts