Palantir’s Glow Fades: PLTR Stock Tests Support on Over-Valuation and Govt Dependence

Growing worries over Palantir Technologies' stretched valuation and strong reliance on U.S. government contracts erased recent gains and...

Quick overview

- Palantir Technologies' recent earnings beat failed to boost investor confidence due to concerns over its high valuation and reliance on U.S. government contracts.

- The company's stock dropped nearly 5%, testing key support levels as skepticism about its long-term growth prospects resurfaced.

- Despite strong Q3 earnings, with revenue up 63% year-over-year, fears about overreliance on government contracts and valuation sustainability persist.

- Investor sentiment has worsened, especially after notable figures like Michael Burry disclosed short positions against Palantir, raising doubts about its future.

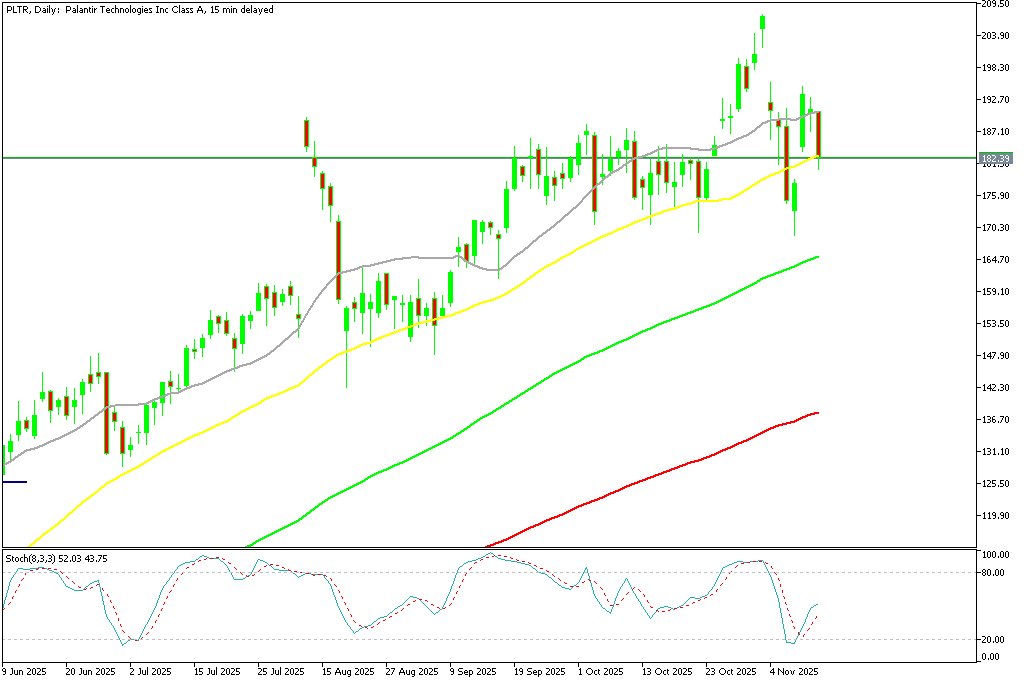

Live PLTR Chart

[[PLTR-graph]]

Growing worries over Palantir Technologies’ stretched valuation and strong reliance on U.S. government contracts erased recent gains and rekindled suspicions about the company’s long-term future, so investors were unimpressed with the company’s most recent earnings beat.

PLTR’s Rally Unravels

Palantir Technologies (NYSE: PLTR) saw its stock tumble nearly 5% midweek, retreating from Monday’s brief rebound as investor enthusiasm gave way to skepticism. Despite reporting record earnings, the focus has shifted from growth to sustainability, with more than half of Palantir’s revenue tied to U.S. government contracts — a risk amplified by ongoing political gridlock and uncertainty over federal budgets.

PLTR Chart Daily – The 50 SMA Is Being Tested Again

The selloff pushed shares below $181, nearing the 50-day simple moving average, a key support that had underpinned the stock’s rally since summer. A decisive close beneath this level could open the door for further declines toward the $150 range, according to technical analysts, signaling waning confidence among retail and institutional investors alike.

Valuation Excess Becomes a Liability

Even with surging demand for its AI-driven data platforms, Palantir’s valuation has become increasingly hard to justify. Trading at an eye-watering 465x forward earnings, it now ranks among the most expensive stocks in the S&P 500, a level many analysts view as unsustainable.

Commentators from The Motley Fool and Forbes both issued cautious notes, warning that the company’s $450 billion market cap leaves “little room for error.” They highlighted that even with exceptional growth, expectations embedded in the share price are detached from financial reality. Investors appear to agree, with profit-taking accelerating as valuations stretch to historic extremes.

Earnings Fail to Calm Fears

Palantir’s Q3 2025 earnings were objectively strong — revenue jumped 63% year-over-year to $1.18 billion, and net income tripled to $475.6 million — but the numbers did little to ease underlying concerns. The company’s overreliance on government contracts, accounting for 52% of revenue, remains a glaring vulnerability. Its commercial business, while improving, still represents a smaller portion of overall sales and relies heavily on a handful of large enterprise deals.

Even upgraded guidance for Q4 and full-year 2025, with revenue projected near $4.4 billion and free cash flow between $1.9–$2.1 billion, wasn’t enough to shift sentiment. Many traders viewed the upbeat outlook as already priced in.

Bearish Bets Deepen Market Doubt

The bearish narrative gained traction when renowned investor Michael Burry — famed for his “Big Short” — disclosed a short position against Palantir. The revelation reinforced skepticism that the company’s AI story is overinflated and vulnerable to a sharp correction.

With macro uncertainty, rising rates, and mounting doubts about profitability, investors are now questioning whether Palantir’s success is more narrative than numbers. The once-celebrated AI pioneer finds itself battling not only competition but also a growing perception that its best days — at least for this cycle — may be behind it.

Conclusion: Reality Catches Up

Despite another quarter of strong results, Palantir’s stock narrative has turned defensive. As market sentiment cools and valuation fears intensify, the company’s heavy government dependence and limited commercial diversification stand out as structural risks. Unless Palantir can demonstrate sustainable, broad-based growth beyond Washington contracts, investors may continue trimming exposure — turning the post-earnings dip into a deeper correction.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account