SMCI Stock Breaks Support After 41% Monthly Decline – Breakdown or Rebound?

Super Micro Computer's precipitous decline raises concerns about the AI hardware boom's long-term sustainability as well as the company's ab

Quick overview

- Super Micro Computer's stock has plummeted over 70% since its peak in 2024, reflecting growing skepticism about its future in the AI hardware market.

- The company's recent earnings report revealed declining revenue and net income, highlighting structural weaknesses and rising operational costs.

- Intensifying competition from major tech firms and resurfacing governance concerns have further complicated SMCI's challenges.

- As enthusiasm for AI technologies wanes, Super Micro faces a precarious future without significant improvements in profitability and governance.

Super Micro Computer’s precipitous decline raises concerns about the AI hardware boom’s long-term sustainability as well as the company’s ability to endure in a more cutthroat market.

A Brief Stabilization Gives Way to Renewed Selling

Super Micro Computer (NASDAQ: SMCI) attempted to find balance earlier this month, but any sign of stabilization has evaporated. The stock dropped another 4% on Wednesday, extending a punishing multi-week decline that began after disappointing Q3 2025 results. With shares down roughly 12% over the last five sessions, the bearish pressure continues to intensify.

The reversal has been swift and unforgiving. SMCI, once lauded as one of the biggest winners of the AI infrastructure cycle, has now surrendered more than 70% of its value since peaking near $123 in 2024. Trading below $35 — the weakest level since March — the stock reflects not only deteriorating sentiment but also mounting skepticism about the company’s long-term resilience in a sector that now looks overcrowded and overhyped.

Earnings Miss Shine Light on Structural Weakness

The company’s latest earnings report failed to offer any comfort. SMCI posted Q3 revenue of $5.02 billion and net income of $168.3 million, both declining year-over-year. Even management’s attempt to reassure investors by lifting full-year sales guidance to $36 billion fell flat.

The numbers revealed deeper issues: stagnant top-line growth, margin compression, and rising operational costs. In a hardware-heavy business where scale and efficiency determine survival, these pressures are particularly damaging. With major AI-linked players — including CoreWeave — also reporting weaker results, appetite for AI hardware names has contracted sharply. The speculative frenzy that once powered SMCI’s ascent has now flipped into something much harsher: avoidance.

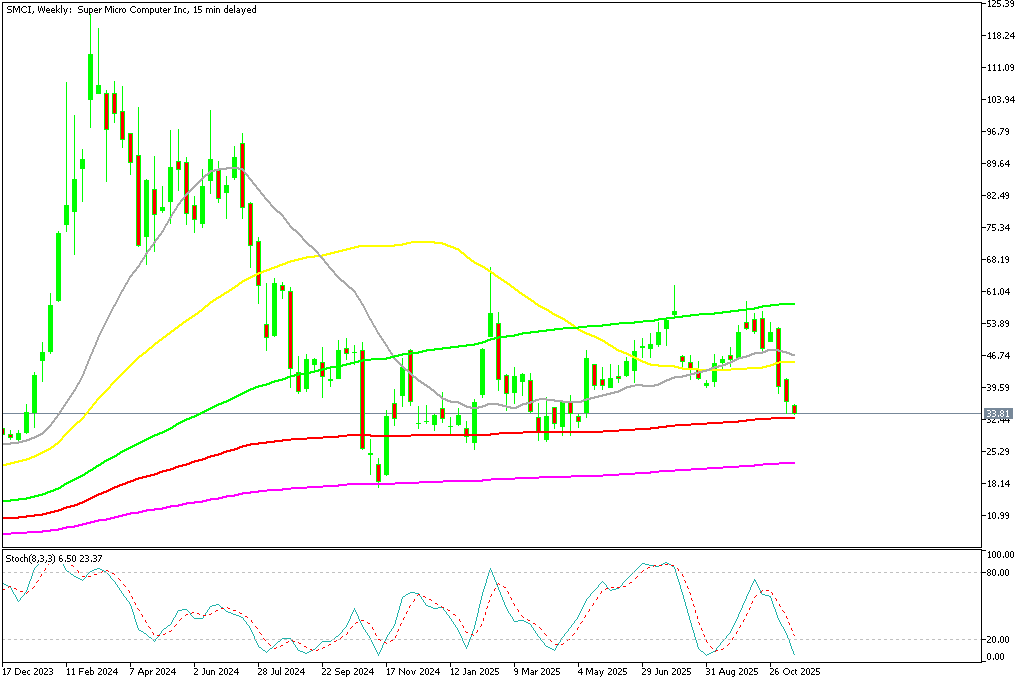

Charts Confirm a Full Technical Breakdown

Technically, the stock’s landscape has deteriorated beyond repair — at least for now. The failed September rebound from $42 to $58.77 confirmed the 100-week SMA (green) as firm resistance. Once SMCI slipped back below $40, sellers swarmed in. The drop toward $33.50 brings the price uncomfortably close to the 200-week SMA (red), a level that, if broken, could trigger an even deeper slide.

SMIC Chart Weekly – The 100 SMA Rejected the Price Again

The chart setup reflects a broader market shift: investors are abandoning speculative AI hardware trades in favor of companies with sustainable profitability, leaving names like SMCI exposed.

Competition Intensifies as Governance Doubts Re-Emerges

SMCI’s challenges are compounded by fierce competitive encroachment. Major technology firms are accelerating efforts to design and manufacture their own chips and servers, reducing reliance on third-party vendors. Reports that Alibaba is building its own AI inference chips have heightened concerns that SMCI’s role in the supply chain may be shrinking.

Compounding the problem, governance concerns have resurfaced. Analysts have raised fresh doubts about SMCI’s accounting consistency and internal controls, pointing to irregularities and limited disclosure transparency. Though no formal actions have been taken, such scrutiny is particularly damaging for a company already fighting an uphill battle.

AI Fatigue Undermines the Bull Case

What was once seen as unstoppable AI expansion is now being reevaluated as overstretched optimism. Profitability across the AI infrastructure space remains uncertain, and Super Micro’s heavy dependence on high-spec server demand leaves it doubly exposed. As excitement around quantum and AI technologies cools, the market is no longer willing to give SMCI the benefit of the doubt.

Conclusion: A Former High-Flyer Now Facing Harsh Reality

Super Micro Computer has become a reminder of how quickly market narratives can flip. Without clearer visibility into margin recovery, stronger governance, and renewed competitive positioning, the stock remains vulnerable to further downside. Unless the company delivers a meaningful turnaround, SMCI risks sinking deeper into both technical weakness and investor distrust — making it one of the starkest casualties of the fading AI hardware boom.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts