Oracle Breaks Below $200 as Big Contracts Can’t Stop ORCL Stock From Diving

Oracle's recent slide reflects growing concerns that the company's goals for cloud computing and artificial intelligence will fall short...

Quick overview

- Oracle's share price has dropped nearly seven percent, indicating deteriorating investor confidence in its AI and cloud ambitions.

- Notable insider selling has raised concerns about the company's near-term outlook, contributing to negative market sentiment.

- Despite announcing a strategic AI partnership, Oracle's stock response was tepid, reflecting investor focus on financial performance over headlines.

- With competitors advancing rapidly, Oracle faces challenges in profitability and market perception, leading to skepticism about its future growth.

Live ORCL Chart

[[ORCL-graph]]

Oracle’s recent slide reflects growing concerns that the company’s goals for cloud computing and artificial intelligence will fall short of the high standards set by the industry.

Oracle Gives Back Gains as Selling Accelerates

Oracle’s share price is struggling to regain its footing after a brief rebound earlier this week. A surge to around $234, sparked by optimism following Nvidia’s latest earnings release, proved short-lived. Sellers quickly regained control, driving the stock sharply lower and erasing all recent gains. By the end of the session, Oracle was down nearly seven percent, reinforcing the view that confidence in the stock is deteriorating.

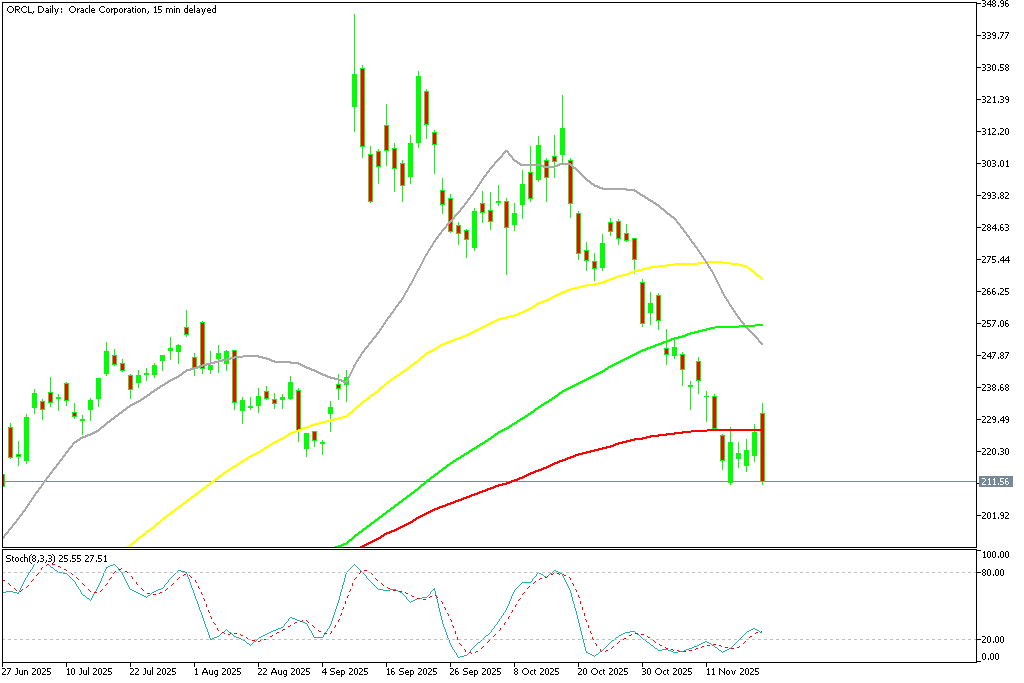

ORCL Chart Daily – MAs Have Turned Into Resistance

What had once been viewed as a resilient uptrend is now beginning to resemble a broader unwinding of optimism surrounding the company’s cloud and AI ambitions.

Insider Transactions Add to Investor Unease

The downward pressure has been magnified by a wave of notable insider selling. While such activity does not always signal trouble, its timing, amidst growing weakness in the stock, has unsettled investors. The sales have contributed to a narrative that those closest to the business are less confident in the near-term outlook — a perception that has weighed heavily on sentiment.

At a time when the market is already on edge over higher costs and slowing growth, any hint of internal caution can quickly tip the balance toward more aggressive selling.

Critical Support Levels Start to Give Way

From a technical perspective, the situation has worsened significantly. After reaching record levels above $345 earlier in the year, Oracle’s shares have dropped by roughly forty percent and now hover around the $210 area. The stock has fallen below its 20-week simple moving average — a key long-term support that had held throughout much of 2024.

Both the 50-day and 100-day moving averages have begun to flatten and roll over, a classic warning sign that the prior uptrend has reversed. Technicians are now pointing to the $200 region as a crucial level. If that area fails to hold, it could open the door to deeper declines and further damage to confidence.

AI Partnerships Fail to Calm the Market

Oracle recently announced a strategic collaboration with Defense Technologies, aiming to deliver advanced AI and sovereign cloud capabilities to national security and defense clients. While the deal is significant on paper, the market response has been almost nonexistent. Instead of sparking renewed enthusiasm, the announcement was met with indifference, suggesting that investors are now more focused on financial outcomes than on headlines.

Despite expanding its presence in AI infrastructure, Oracle continues to face rising operating costs. Energy prices, maintenance of data centers, and long-term infrastructure investments are weighing on profitability. These pressures have led many to question how sustainable — or scalable — Oracle’s current AI strategy actually is.

Weak Margins Undermine the Growth Narrative

Oracle’s AI-linked cloud revenue, supported by Nvidia’s powerful chips, has grown in absolute terms. However, profitability has disappointed. Gross margins in this segment reportedly trail far behind those of larger rivals such as Microsoft and Amazon, whose cloud divisions enjoy greater efficiency and scale.

This disparity is becoming harder for investors to ignore. In an environment where profitability and efficiency matter more than promises, Oracle’s thin returns are raising doubts about whether its transformation into a major AI infrastructure player is realistic.

Falling Behind as Competitors Push Ahead

While Oracle wrestles with margin pressure and uncertainty, competitors continue to surge. Nvidia remains the dominant force in AI hardware, Microsoft is expanding its cloud reach at a steady pace, and Palantir is capturing high-profile government and enterprise contracts. The contrast has highlighted Oracle’s slower progress and added to the perception that it is losing ground in a rapidly evolving market.

Outlook: Optimism Gives Way to Skepticism

Investor patience appears to be wearing thin. Without clear evidence of improved margins or a sharp acceleration in cloud performance, confidence is likely to remain fragile. The shift in sentiment is stark: what was once promoted as a powerful AI comeback story is now being reassessed as a company under growing financial strain.

For now, Oracle’s trajectory reflects a market that is no longer driven by hype, but by hard numbers — and those numbers will need to improve before belief in its long-term vision can be restored.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts