SMCI Stock Tests Support Again – Will the Super Micro Fall Below $30 As AI Boom Fades?

Following yesterday's shortfall in Oracle's earnings, Super Micro Computer is once again under intense market pressure due to waning...

Quick overview

- Super Micro Computer is experiencing significant market pressure due to declining AI enthusiasm and investor skepticism following Oracle's earnings miss.

- The company's stock has plummeted over 70% from its 2024 peak, reflecting broader doubts about its long-term viability in a changing market.

- Recent earnings revealed revenue and net income declines, raising concerns about growth stagnation, margin compression, and operational inefficiencies.

- Increased competition and governance challenges are compounding SMCI's struggles, as the market reassesses the sustainability of AI infrastructure growth.

Following yesterday’s shortfall in Oracle’s earnings, Super Micro Computer is once again under intense market pressure due to waning enthusiasm for AI and structural flaws.

A Short-Lived Stabilization Followed by Sharper Selling

Super Micro Computer’s recent behavior in the market reflects a dramatic shift in sentiment toward the broader AI hardware space. Earlier this month, the stock attempted a mild rebound after touching November lows near $31, hinting at a potential pause in the relentless drawdown. But that stability proved fleeting. On Thursday, shares sank another 5%, extending a three-day decline that revived concerns about a deeper structural downturn.

The scale of the reversal is striking. Once hailed as a core beneficiary of the AI infrastructure wave, SMCI has now lost more than 70% of its value from its 2024 peak near $123. Trading slightly above $33, the stock increasingly reflects not just temporary investor caution but broader doubt about the company’s long-term durability in a rapidly shifting environment. Oracle’s earnings miss this week intensified pressure on quantum and AI hardware names, feeding the bearish tone across the sector.

Revenue Pressures and Margin Erosion Deepen Concerns

SMCI’s latest earnings report offered little to counter the growing pessimism. Third-quarter revenue came in at $5.02 billion, while net income fell to $168.3 million — both down from a year earlier. Even the company’s decision to raise its full-year revenue guidance to $36 billion failed to inspire optimism, drawing comparisons to Oracle’s muted response to its own forecast revisions.

What troubled investors most was the quality behind the numbers: growth stagnation, margin compression, and rising operational expenses. SMCI’s earnings have been squeezed sharply, with first-quarter revenue falling 15.5% and earnings tumbling 56%. In an industry where scale is essential for profitability, deteriorating margins signal deeper inefficiencies. At the same time, customer concentration has strained the business; major clients have negotiated tighter pricing, further pressuring margins.

The company also reported negative free cash flow of $950 million in early fiscal 2026, reflecting the financial weight of its rapid expansion efforts. Rising receivables underscore a related issue: SMCI is extending more credit to retain high-volume customers, raising questions about cash management and balance sheet resilience.

Technical Signals Warn of Further Weakness

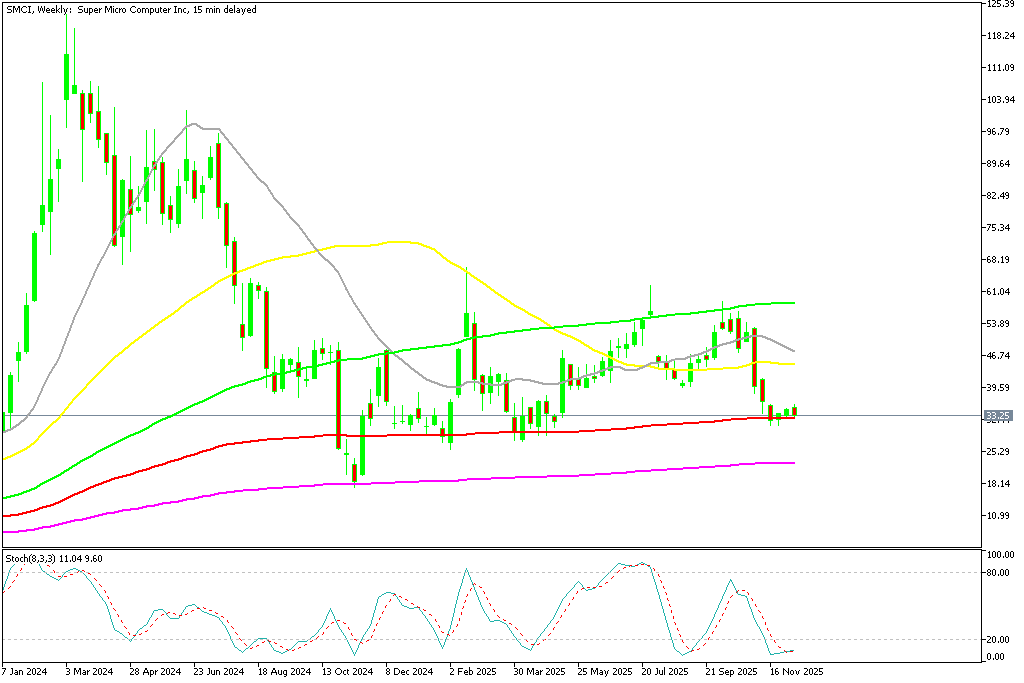

From a chart perspective, SMCI’s situation appears increasingly fragile. The failed recovery in September — from $42 to just under $59 — reinforced the 100-week moving average (green) as a major ceiling. The stock’s subsequent decline back below $40 brought a surge in selling, pushing it toward November’s $33 zone, where it briefly held support near the 100-week smoothed SMA (red).

SMIC Chart Weekly – The 100 SMA Rejected the Price Again

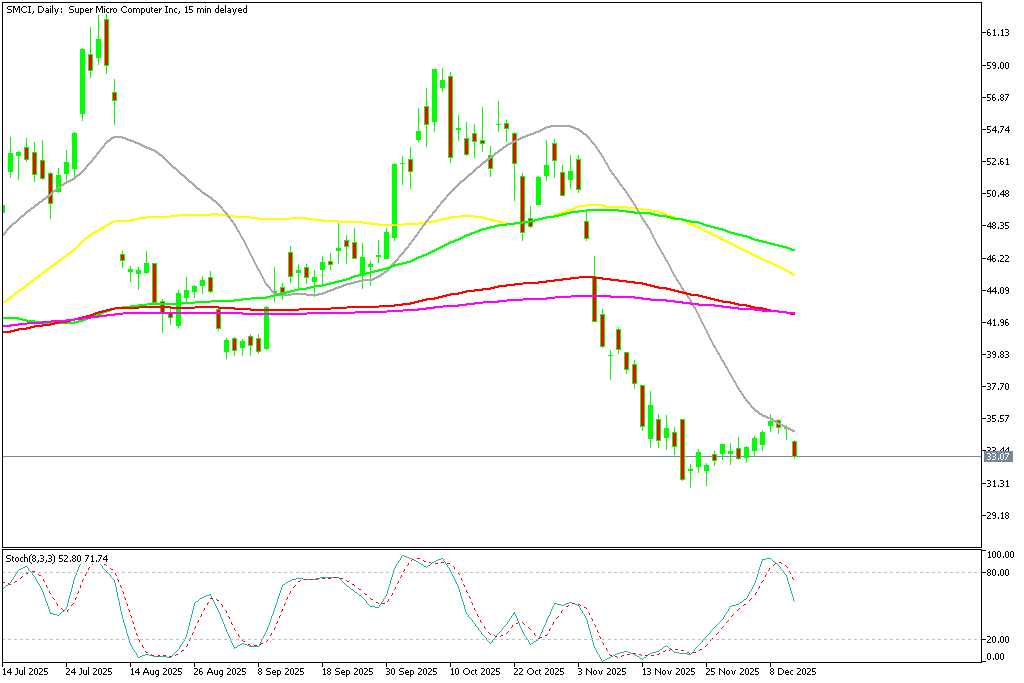

That stability has once again evaporated. The stock is now retesting the same long-term level, and a decisive breakdown could invite a move below $30, with potential downside toward the 200-week moving average (purple) near $23. On the daily chart, the 20-day SMA (gray) rejected price attempts to reclaim the mid-$30 range. Momentum indicators such as stochastic oscillators have already reversed lower, reinforcing bearish momentum.

SMIC Chart Weekly – The 20 SMA Rejected the Price

These technical patterns suggest not only a breakdown of trend but a psychological retreat from speculative trades tied to the AI server boom. As investors gravitate toward companies with steady earnings visibility, names like SMCI — which thrived on hype rather than proven, durable profitability — are finding less support.

Competitive and Governance Challenges Resurface

The company is confronting headwinds from increasingly aggressive competitors. Several large technology firms are developing their own AI chips and server systems, potentially reducing the need for SMCI’s high-performance platforms. Recent reports that Alibaba is designing its own inference chips have added fresh pressure, signaling a shift away from third-party suppliers.

At the same time, governance concerns — previously dormant — have begun to resurface. Analysts have raised questions about SMCI’s accounting consistency, disclosure practices, and internal controls. While no regulatory actions have been taken, such scrutiny can weigh heavily on sentiment, particularly when combined with operational challenges and a rapid expansion strategy.

SMCI’s huge scale-up plans, including production goals of 6,000 racks per month and facility expansions across Taiwan, Malaysia, the Middle East, and the Netherlands, have strained both inventory levels and working capital. The rapid build-out, once seen as a bullish signal of overwhelming demand, is increasingly viewed as a potential overextension.

A Market Confronting AI Fatigue

The broader backdrop to SMCI’s struggles is an emerging fatigue in the AI infrastructure trade. The once-unshakeable narrative of explosive and perpetual AI growth is being reassessed. Investors now recognize that the sector faces real risks: uncertain long-term profitability, rising competition, enormous capital requirements, and cyclical hardware demand.

Super Micro, heavily dependent on the high-end server cycle, sits at the intersection of all these vulnerabilities. With enthusiasm for quantum and AI-linked hardware cooling, the market is no longer willing to overlook SMCI’s operational challenges or speculative valuation.

Conclusion: Super Micro Computer’s steep decline reflects more than a disappointing earnings season — it signals a deeper shift in market psychology. With technical breakdowns, rising competitive threats, governance questions, and weakening AI momentum, SMCI finds itself navigating a much harsher landscape than the one that propelled its meteoric rise. Unless the company can demonstrate sustainable profitability and stronger operational control, the path ahead will likely remain turbulent, with investors continuing to favor stability over speculation.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account